System trading is a data-driven, disciplined approach that uses a set of rules and a pre-defined process to make trading decisions, issue buy and sell orders, or execute a trading system.

The simplest example would be to think of an “If, then” statement. That is, if X happens then do Y. For instance,

if price crosses above a simple moving average

then buy 100 shares of stock

System traders do not deviate from their system and have no or very little manual intervention. The trading rules and long-term process should drive the trades and positions as well as account for various market conditions.

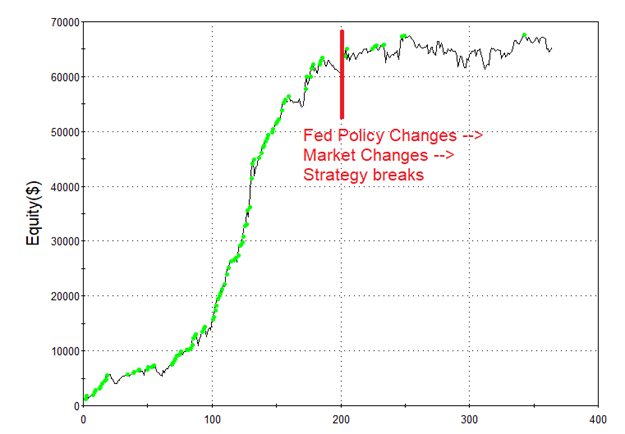

The best traders of all time including the best hedge fund of all time, Rennaissance Technologies, are famously known as system traders.

What is a Trading System?

A trading system is a set of rules that determine the buy and sell signals based on the market data. A proper trading system should also account for position sizing, risk management, and other key factors.

A trading system can incorporate price action, volume, volatility, technical analysis, fundamentals, market breadth, economic data, news events, intermarket analysis, multiple timeframe analysis, system performance, seasonal factors, and more to determine trading decisions. It is entirely up to the trader to backtest how the trading system would perform in various financial conditions.

Automated or Not?

A trading system does not need to be fully automated and can still be executed manually. This is more commonly referred to as ‘hybrid trading’ where the trader utilizes data and statistics to find trading edges but does not fully automate the trading system but rather manually executes the trades whenever an alert is received.

There are many advantages to full automation which I cover in-depth in my Algorithmic Trading Guide but here are a few quick ones

More time to research new ideas

No emotions in automated trading

Monitor and trade more markets

Trade more time zones

No trader fatigue or manual errors (fat fingers)

Most system traders code their strategy logic or trading systems so that execution happens automatically. If you cannot code or program, keep reading to find out how you can still create automated trading strategies with no coding. Jump Ahead

System Trading vs. Discretionary Trading

Discretionary trading relies on intuition, gut-feel, in-the-moment decision making, and unreliable execution. System trading relies on tested data and statistics paired with reliable execution. After spending a decade-plus in the professional trading world, I am a bit biased. However, listen to Jim Simons – founder of Renaissance Technologies – talk about the importance of treating trading like a business and the necessity of having a trading system. Watch from 36:48 to 38:02.

“That religious sticking to the model is the only way you can run such a business. Because you cannot simulate that guy that walked in and said ‘Hey, Google is too high. Let’s sell it’. How can you simulate that? You don’t know what might have happened.”

Discretionary Trading Pitfalls

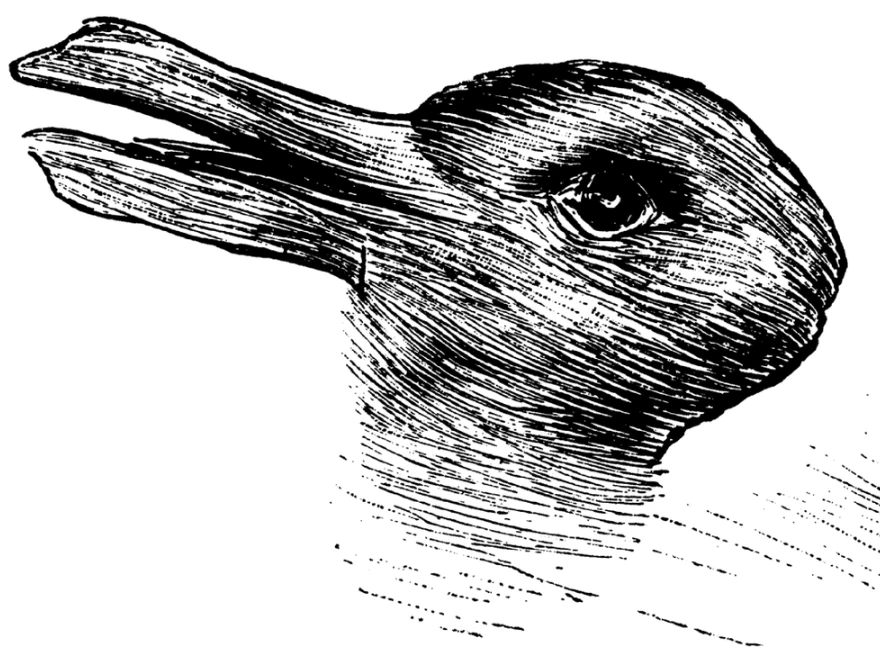

What you see is not the same

Humans are prone to seeing delusions and recognizing patterns where there are not any. It is part of our survival mechanism and the market preys on this. For instance, do you see a duck or a rabbit?

Half the traders see one thing and half the traders see the other. This is no way to build a reliable business or risk your hard-earned capital.

Two or more patterns on the same chart

Driving the previous point home in another way. Notice this chart below covers the same date range but can easily show multiple different technical analysis chart patterns depending on who you give the crayon to. Double bottom, channel breakout, bear flag, go-broke special.

Linear vs Log Charts

Do you use linear scale or log scale charts? How we even set up our trading charts will determine what patterns and peaks and valleys line up. This presents a whole new can of worms that make it problematic to build a business off of discretionary methods lacking testable insights.

Trading “Truths”

The big players need liquidity to exit their positions and in order to do so they need a lot of retail traders to take the other side of their trade. This has created astute institutional and professional traders to abuse old trading axioms and sayings (that may have used to work) to their advantage.

The market marketing machine teaches new traders simple sayings and patterns with obvious names like bearish engulfing candle or bullish flag pattern to initiate a new flock of fish to take the opposite side of their trades.

I wrote about three of these common trading “truths” in this blog debunking them and showing the data of what actually happens. All the more reason to test everything and build trading systems rooted in data.

What is Mechanical Trading?

Mechanical trading is the process of having pre-determined rules generate trade entry and exit signals. Mechanical trading is simply another way of describing system trading or automated trading. System trading or Mechanical Trading can be used for day trading, trend following, mean reversion, arbitrage or any other type of trading idea.

Mechanical Trading Strategies

Turtle Trading

The original story covers 23 novice traders hired to execute a trading system as part of an experiment set up by two professional traders. The goal was to see if regular people could achieve success following a trading system.

The story is fascinating and the strategy itself is disclosed in the famous books The Complete Turtle Trader and Way of the Turtle. The strategy’s performance has since waned but can be thought of a simple breakout strategy executed across commodities with some volatility-based sizing.

Ichimoku Trading Strategy

The Ichimoku Cloud technical indicator uses a series of moving averages with different lookbacks and offsets to create a “price cloud” (pictured below). I placed a purple box to show most of the price collapse happened during the “bullish cloud phase”.

This indicator is often popularized because the creators claim that it can predict future price movements. However, this may be another trading “truth”, as most testing does not show a positive edge or e-ratio.

Forex Robot Trading

This is an alternative word for automated trading systems or algorithmic trading in the forex industry. I am not sure why the forex industry has taken to the terminology robot but one can consider these all the same.

Trading systems can be applied to any timeframe, bar type, or asset class including forex and cryptocurrencies. I have given away a handful of successful “forex trading robots” including this one below. Although, you will hopefully never hear me use this phrase again.

An alternative trading system (ATS) is an electronic trading system that matches orders for buyers and sellers of securities and are often SEC-regulated but not national securities exchanges. Alternative trading systems are more considered trading venues that are more loosely regulated than exchanges, not to be confused with a rules-based trading system for executing buy and sell orders as we have been discussing in this post. A few examples of alternative trading systems would be

Crossing networks

Dark Pools

Electronic Communication Networks (ECNs)

Can you have an automated trading system with no code?

Build Alpha Trading System Software

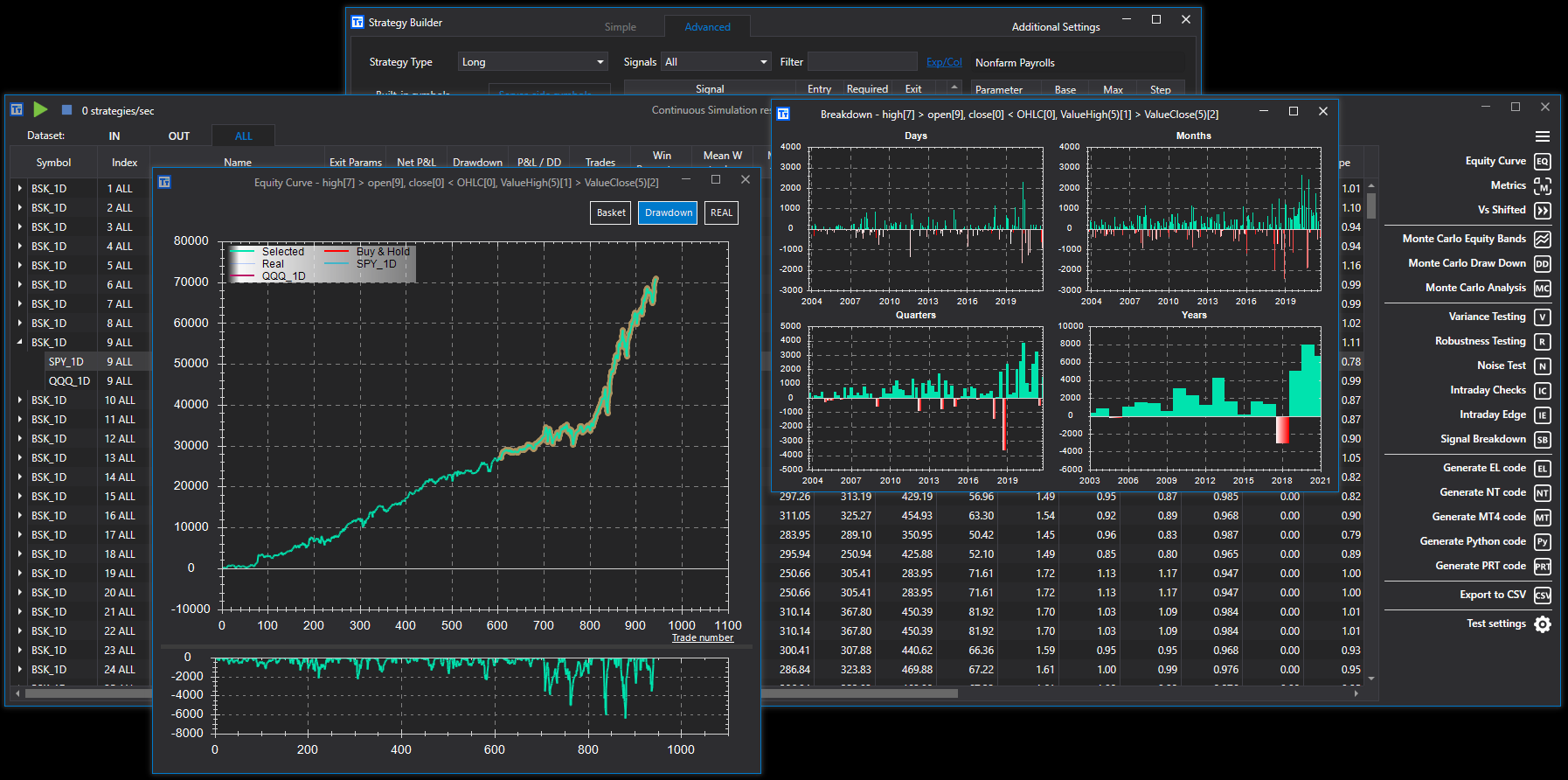

Yes, Build Alpha is a no code strategy generator that I have been building for the past half-decade or so. This software allows traders to select entries, exits, risk management, and more from a point-and-click interface and the genetic algorithm (strategy engine) will find the best strategies for you.

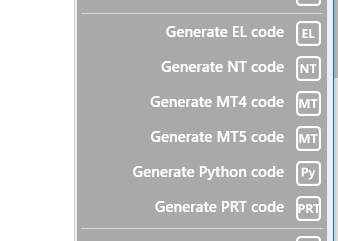

After finding strategies that meet your desired risk controls and robustness tests you can monitor the strategy live to receive real-time alerts and position changes or hit a button to generate fully automated code for a variety of popular brokerage platforms such as TradeStation, NinjaTrader8, MetaTrader4, MetaTrader5, Python, and more.

Watch this demo video to see how fast I can build

A MACD strategy

A RSI-2 strategy

Thousands of strategies better than the two above

Please note this video is a few years old. Check out the Build Alpha Demo page to see new versions of the software.

Summary

System trading is a data-driven approach that requires a set of rules that determine entry, exit and sizing of a trading strategy. A trading system can be executed manually or automatically but should involve very little or no human intervention. Traders struggling with emotions, discipline, or finding quantifiable edges should investigate system trading. Build Alpha enables traders with no coding experience to build, test, and automate their trading systems. Shoot me an email anytime to learn more.

Author

David Bergstrom – the guy behind Build Alpha. I have spent a decade-plus in the professional trading world working as a market maker and quantitative strategy developer at a high frequency trading firm with a Chicago Mercantile Exchange (CME) seat, consulting for Hedge Funds, Commodity Trading Advisors (CTAs), Family Offices and Registered Investment Advisors (RIAs). I am a self-taught programmer utilizing C++, C# and python with a statistics background specializing in data science, machine learning and trading strategy development. I have been featured on Chatwithtraders.com, Bettersystemtrader.com, Desiretotrade.com, Quantocracy, Traderlife.com, Seeitmarket.com, Benzinga, TradeStation, NinjaTrader and more. Most of my experience has led me to a series of repeatable processes to find, create, test and implement algorithmic trading ideas in a robust manner. Build Alpha is the culmination of this process from start to finish. Please reach out to me directly at any time.

The Best Way to Properly Backtest on Tradestation

How to Download TradeStation

If you have not already downloaded TradeStation, then please do so before continuing with this backtesting on TradeStation guide. First, head to the TradeStation’s home page to login to your Client Center. Next, select the Download Software tab in the top menu. At the time of writing, TradeStation offers both version 9.5 and version 10. Build Alpha and this guide are compatible with both. Additionally, TradeStation has a great installation video and user guide here:

Create a Strategy for Backtesting and Live Trading

In order to backtest, we need a strategy. There are two ways to create a strategy for backtesting and live trading in TradeStation. One requires coding and one does not.

Easy Language Development Environment

TradeStation’s proprietary coding language, called Easy Language, was designed to make programming easy for traders. TradeStation handles all of the “no fun” tasks like data connectivity, order routing, and account monitoring while traders get to focus on the logic of the strategy.

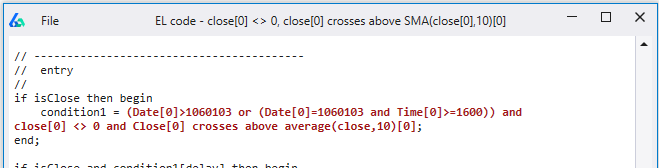

Easy Language allows traders to express their trading ideas in almost human readable syntax. Below is an example of a moving average crossover system that buys 100 shares on a cross above and sells 100 shares on a cross below

If Close[0] crosses above Average(Close,10)[0] then buy 100 shares next bar open;

If Close[0] crosses below Average(Close,10)[0] then sell 100 shares next bar open;

Learning the ins and outs of easylanguage are not as gruesome as learning a traditional programming language. In addition, TradeStation has great documentation and tons of pre-built-in functions for all popular indicators.

Build Alpha and Generated Code

Build Alpha is a no code strategy builder that enables traders to build, test, and generate code for tons of automated trading strategies. This presents an option for those that do not want to learn how to program but still want to do algorithmic trading.

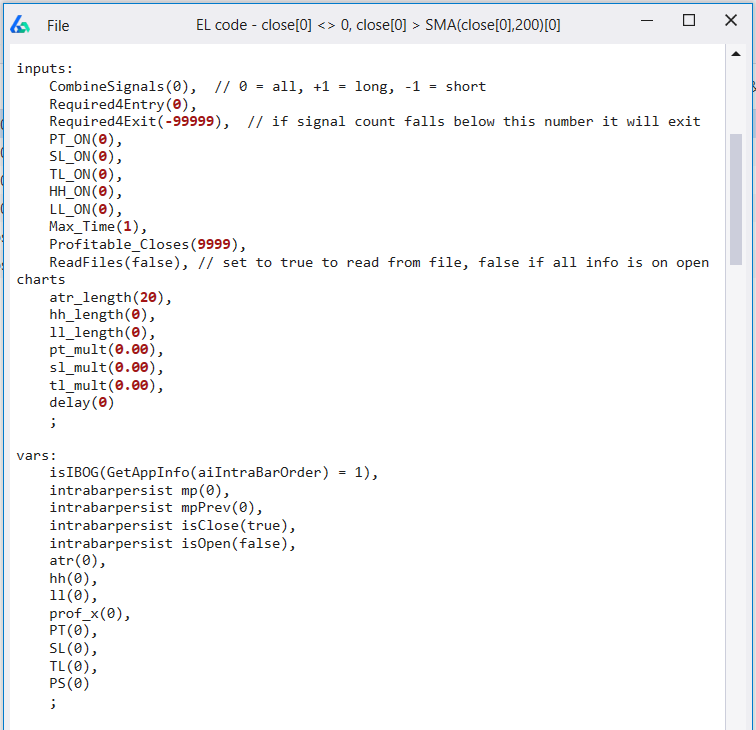

After generating a strategy, simply hit the ‘Generate EL Code’ button to get full code. This code can be copy and pasted into TradeStation’s Development Environment as if you coded it yourself.

Compile or Verify the Strategy

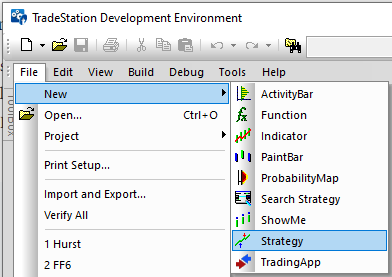

Whether coded yourself or built with Build Alpha, we must save the strategy in TradeStation’s development environment. To do so follow these steps

View >> Development Environment

File >> New Strategy

Name the strategy

Code your strategy or copy and paste from Build Alpha

Hit F3 or Verify to save the strategy

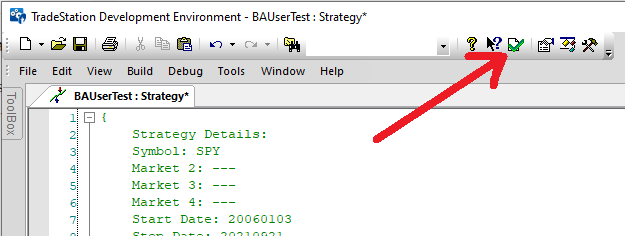

How to Add a Strategy to a Chart

Ok, now that we have a trading system how do we view it on a chart? The next step to properly backtest on the TradeStation trading platform is to open a chart.

Step 1 Open a New Chart

In the File menu, head over to View >> TradingApp Launcher >> Chart Analysis. Alternatively, one can do File >> New >> TradingApp Window >> Chart Analysis.

Double-click on the prices to access the settings. You can adjust the date range, candlestick type, timeframe, and symbol. Alternatively, you can right-click on the chart and select Format Symbol to do the same.

Step 2 Insert Strategy

Now that our chart is set, we need to insert the strategy onto the chart. From the File menu you can Insert >> Strategy or you can right-click on the chart and select Insert Strategy.

Next, select your desired strategy. You should see the trades appear on the chart.

Step 3 Turn on and configure settings

Let’s make sure our strategy settings are correct. Right-click on the chart and select Format Strategies or double-click on one of the entry or exit arrows to open the settings menu.

To automate the strategy, one must

check the box “Generate Strategy Orders for Display in TradeManager’s Strategy Orders tab”

check the box “Automate execution using”

select an account

select a confirmation setting

Please note these steps are the same for simulated trading and live accounts. Always confirm which account you are signed into prior to automating anything!

Max Bars Back and sufficient market data

The trading software needs sufficient data to calculate whatever it is your trading systems do. TradeStation has a setting called “Maximum number of bars study will reference” but it is more colloquially known as “Max Bars Back”.

This setting instructs TradeStation how many bars to wait before the trading strategy should begin trading. If your strategy uses a 200-period simple moving average, then it would be wise to set the Max Bars Back to 201.

To find this setting, right-click on the chart and select Format Strategies. In the next window, choose the “Properties for All” tab and look in the lower left. After setting an appropriate value hit OK and then continue to hit Close on the Format Analysis Techniques & Strategies window.

This setting is meaningful regardless of timeframe, tick data, daily, weekly, etc. as TradeStation considers bars.

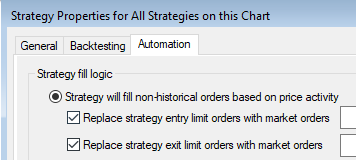

Advanced Automation Settings in TradeStation

We have now set up a simple strategy with simple settings. TradeStation has many more noteworthy settings. In the Properties for All window, there are three tabs across the top. Select the ‘Automation’ tab to see a new set of configurations.

Fill historical orders

The first option is to instruct TradeStation on what to do when your strategy logic generates an order, but the market does not give you a fill. The default setting is to change your limit order to a market order 15 seconds after the strategy logic generates an order (assuming no fill).

Multiple Strategies on the Same Symbol

The next option to enable is if you will have multiple strategies for the same symbol. TradeStation will make sure one strategy’s exit does not close out a position from another strategy if you select the “Allow multiple automated strategies on multiple charts using the same symbol” option.

Stop Orders

Finally, enable TradeStation to send stop orders to their own server. This is an underrated feature and worth explaining. If your TradeStation account is down, internet goes out, lose power, etc. while you have an open position then this may save you. TradeStation will notice stop orders from your strategy logic and house them on their server. If you lose power, no problem, your order is still live on a TradeStation Technologies Inc server.

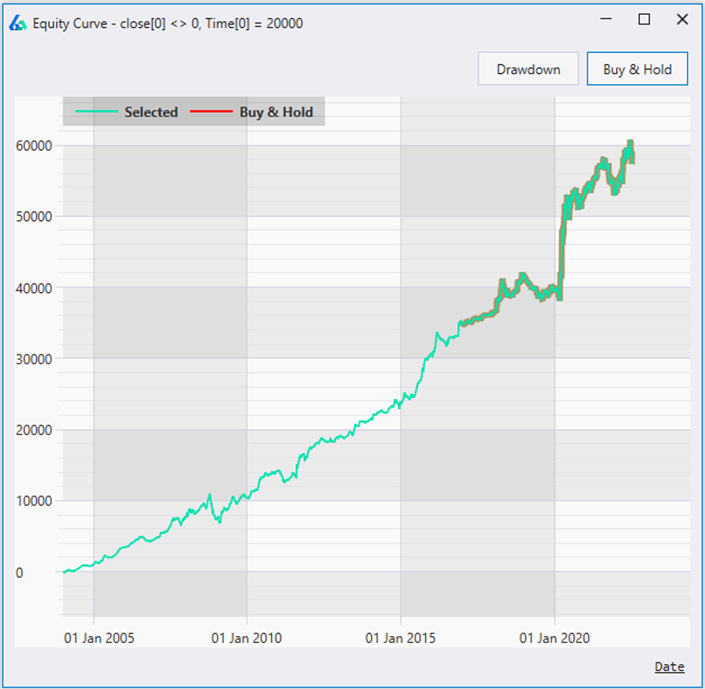

How do we view our back test results? After loading the strategy on the chart we can view the Strategy Performance Report. To open the report you can either

Hit “ALT” + “SHIFT” + “P”

View >> Strategy Performance Report

The report is extensive and has many options. I will briefly describe them all below

Performance Summary – shows all relevant performance metrics

Trade Analysis – provides insights into streaks, run ups and drawdowns

Trades List – list of all entries, exits, and P&L

Periodical Returns – strategy returns broken down by day, week, month and year

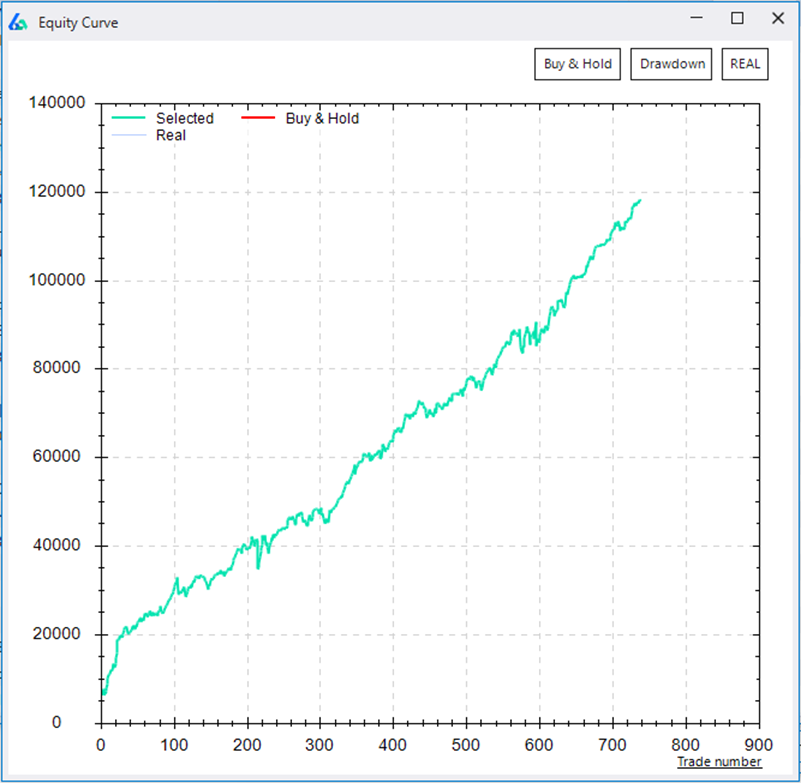

Performance Graphs – equity curves and various other visual displays

Trade Graphs – more visuals to view trade results

Settings – an overview of symbol, strategy, and system settings

You can also save or print this report in the upper left near the File menu. Reminder, backtest results are not indicative of future results.

Luckily, the Strategy Performance Report can be saved to a csv or excel file and imported into Build Alpha. Build Alpha has a converter that can take these Strategy Performance Reports and import any strategy.

Build Alpha offers more advanced robustness testing and portfolio testing than TradeStation does. This is also a way to combine your TradeStation strategies with your Build Alpha strategies to do more thorough research.

TradeStation Backtesting Summary

TradeStation securities offers a trading platform, brokerage account, and programming language called easylanguage for systematic traders. Traders can load strategies onto real time charts and view past performance, the trades on a chart, and various performance results. TradeStation has data for all assets such as Futures, Stocks, ETFs, forex, cryptocurrencies and various indexes. Build Alpha provides a no code strategy builder to produce fully automate-able Easy Language code for TradeStation.

For those interested in getting started with Build Alpha and TradeStation, please reach out to me to find out how TradeStation will cover your Build Alpha license cost. Read more here TradeStation and Build Alpha promo

Author

David Bergstrom – the guy behind Build Alpha. I have spent a decade-plus in the professional trading world working as a market maker and quantitative strategy developer at a high frequency trading firm with a Chicago Mercantile Exchange (CME) seat, consulting for Hedge Funds, Commodity Trading Advisors (CTAs), Family Offices and Registered Investment Advisors (RIAs). I am a self-taught programmer utilizing C++, C# and python with a statistics background specializing in data science, machine learning and trading strategy development. I have been featured on Chatwithtraders.com, Bettersystemtrader.com, Desiretotrade.com, Quantocracy, Traderlife.com, Seeitmarket.com, Benzinga, TradeStation, NinjaTrader and more. Most of my experience has led me to a series of repeatable processes to find, create, test and implement algorithmic trading ideas in a robust manner. Build Alpha is the culmination of this process from start to finish. Please reach out to me directly at any time.

Jim Simons – The Man Who Solved the Markets

Who is Jim Simons?

Jim Simons, born in 1938, is often referred to as “the most successful hedge fund manager of all time” and the “greatest investor on Wall Street”. The Financial Times named him “the world’s smartest billionaire” in 2006. Simons is the founder of Renaissance Technologies, a quantitative trading hedge fund based out of New York, that boasts an incredible 66.1% average annual return since 1988. Simons’ approach to the markets is fully systematic and there is so much to glean from his work as Jim Simons launched the quant revolution. This article will examine Simons’ many accomplishments and a few takeaways that can help us become better system traders.

If you are not interested in his origins and rather skip ahead to the systematic trading parts choose below

Simons began as a mathematician and arguably had a full career before leaving to start Renaissance Technologies. He studied mathematics at Massachusetts Institute of Technology (MIT) and later got his Ph.D. from the University of California, Berkeley.

Simons put his mathematics skills to the test working with the National Security Agency (NSA) to break codes during the Cold War while simultaneously teaching at MIT and later Harvard University. After his public opposition to the Vietnam War, Simons was forced out but later appointed chairman of the math department at Stony Brook University.

Simons is known for his studies in pattern recognition and developed the Chern-Simons form with Shing-Shen Chern and is credited with contributions toward the development of String Theory. His theoretical framework combined geometry, topology, and quantum field theory.

Simons has formally received recognition in mathematics, geometry, and topology before shifting his focus to finance in the late 1970s

AMS Oswald Veblen Prize in Geometry 1976

Elected to National Academy of Sciences 2014

The Greatest Trader on Wall Street

Jim Simons founded Renaissance Technologies in 1982 as a 40-year old retired mathematics professor. However, he left his job/academia to start his first hedge fund Monemetrics in 1978. This fund was moderately successful and employed both fundamental and technical approaches to the market, but Simons felt “gut wrenched” by the emotional swings.

Simons decided to use a purely systematic approach to avoid emotional rollercoasters and avoid common trading biases that trip up most traders. Simons staffed the new fund, Renaissance Technologies, with mathematicians, computer scientists, and physicists to pioneer a new approach to algorithmic trading.

Since 1988, Jim Simons’ Renaissance Technologies flagship fund, the Medallion Fund, has returned an average of 66.1% per year which shatters any other publicly available returns over the same horizon. Later I will dissect what little information is available about Simons’ (and RenTec) strategies, approach and success. Skip ahead

Simons is quoted as saying his best algorithm has always been

“you get smart people together. You give them a lot of freedom. Create an atmosphere where everyone talks to everyone else. They’re not hiding in a corner with their own little thing. They talk to everybody else. And you provide the best infrastructure, the best computers and so on that people can work with. And make everyone partners. So that was the model that we used in Renaissance. So we would bring in smart folks and they didn’t know anything about finance, but they learned.”

Philanthropist

Jim Simons has given over $2.7 billion to philanthropic causes ranging from education and health to scientific research. In 1994, Simons and his wife Marilyn Hawrys Simons co-founded the Simons Foundation which later established the Simons Foundation Autism Research Initiative in 2003.

This foundation founded Math for America in 2004 and Simons later doubled the initial $25 million pledge in 2006.

Simons’ alma maters and former academic employers have been benefactors from Simons’ trading successes with large contributions to University of California Berkley, MIT and Stony Brook. His most recent contributions have been aimed to advance computational science and mathematics.

Jim Simons Renaissance Technologies Medallion Fund

Medallion Fund Beginnings

Simons started in the late 1970s and was met with some initial success. However, Simons questions whether the early success was more luck than skill. Primarily focused on commodity futures using fundamental and technical analysis, Simons never achieved the emotional clarity or systematic approach to have full trust.

In 1988, Simons set up the Medallion Fund with a focus on huge amounts of data diversifying across timeframe, asset class, and pattern. Adding the stock market how Jim Simons and team gained additional success. However, the big success did not come until the early 1990s when he brought Bob Mercer and Peter Brown on board from IBM.

Mercer was a large donor in the 2016 US Presidential election (Trump) and eventually left the firm in 2017 after political differences.

Medallion Fund Fees

Most hedge funds charge “2 and 20” which is shorthand for an annual 2% management fee and a 20% rake on performance. Simons knew he had something special and offered investors “5 and 20” in the early days of Medallion but has since moved toward a “5 and 44” structure. This %5 management fee and 44% profit take may be the most aggressive fees in the industry, but Simons and the Medallion Fund have earned them. Due to the large fees, the net returns are more in line with a 39.1% average annual return instead of the earlier stated 66.1%. However, 39.1% is still remarkable with such a large capital base.

Now most of the investors and owners in the fund are employees as Medallion takes no outside capital.

Assuming the net returns column over the most recent 20-year span then an investor would have experienced the growth of a $1,000 investment into a whopping $906,933.26.

Medallion Fund vs. S&P500

Assuming the past 20 years S&P 500 returns then the same $1,000 invested in the S&P500 would return an impressive $2,039.12. This is a far cry (about 500x smaller) than the return generated by the Medallion fund. There is beating the market, capturing alpha, and then the universe that Medallion and Simons are from. Here are the side-by-side returns:

Medallion Fund Takeaways

Fully systematic

Data-driven

Diversify across timeframe, asset class

Hire smart, collaborative people

Win rate is not as important as trading edge

Compounding creates wealth

Jim Simons Net Worth and Personal Life

Billionaire Status and Forbes List

Jim Simons is the current richest trader in the world with a $28.1 billion dollar net worth ranking him on the Forbes list. He has the highest net worth of any trader or money manager on the Forbes wealthiest list. For example, Simons has a wealth more than three times that of George Soros.

Archimedes Yacht

Jim Simons owns a $100 million yacht with an annual running cost of $8 to $10 million. The 68-meter (222 ft) yacht is appropriately named Archimedes after the famous mathematician. Archimedes the superyacht sleeps 12 in 6 cabins and has room for 18 crew members on board with a dining hall for 20 guests. The yacht was built at the Dutch yacht builder Royal Van Lent and delivered to Simons in 2008. Let’s face it, these big boy toys are half the allure of trading.

Private Jet

Simons also owns a $70 million Gulfstream G650 private jet. You can charter one of these bad boys for about $10,500 per hour, if interested.

Tragedy

Unfortunately, Simons’ 84-plus years have not been without tragedy. In 1996, his son Paul was struck and killed by a car while riding his bicycle on Long Island. Paul was 34 at the time. In 2003, Simons’ son Nicholas, 24 at the time, drowned while on a trip to Bali, Indonesia.

Bonus Fact

Simons does not like, nor does he wear socks. Not sure if there is any correlation to his trading success but perhaps if you are struggling remove the feet prisons. I don’t know.

Jim Simons Quant Trading Insights

As all traders, I am always reading, learning, and trying to find a new piece that can help improve performance, limit drawdown or push me forward. The aforementioned book about Simons came out in 2019 and I devoured it in a weekend. I originally posted some thoughts on a See It Market blog here: 5 Lessons From One of the Greatest Traders of All Time (Jim Simons) – See It Market but want to elaborate on the insights and their application to system trading, Build Alpha and my own musings.

Edge is Important – Not Why It Exists

Simons does not care to explain the hypothesis or explanation of why a predictor or model works. If a predictor has edge and is statistically significant then why bother with some explanation for why it must work.

If the edge can be explained, then others are probably aware of the edge and others will soon trade it away.

In other words, data mining is ok. I’ve long defended this approach since the launch of Build Alpha and is nice to hear Simons echo similar ideas.

In my opinion, it is possible we cannot comprehend why a pattern or edge exists because it exists in a dimension too complex for our current understanding. Discarding an edge because we cannot explain it is a mistake.

Remove human bias and let the data show you where, when, and how to trade. Let others overlook these “unexplainable” patterns.

Excerpts to drive the point home

“Simons and his researchers didn’t believe in spending much time proposing and testing their own intuitive trade ideas. They let the data point them to the anomalies signaling opportunity. They also didn’t think it made sense to worry about why these phenomena existed. All that mattered was that they happened frequently enough to include in their updated trading system, and that they could be tested to ensure they weren’t statistical flukes”. (pg 109)

“Simons and his colleagues hadn’t spent too much time wondering why their growing collection of algorithms predicted prices so presciently. They were scientists and mathematicians, not analysts or economists. If certain signals produced results that were statistically significant, that was enough to include them in the trading model” (pg 150)

“I don’t know why the planets orbit the sun. That doesn’t mean I can’t predict them” – Simons (pg 151)

“More than half of the trading signals Simons’s team was discovering were non-intuitive, or those they couldn’t fully understand. Most quant firms ignore signals if they can’t develop a reasonable hypothesis to explain them, but Simons and his colleagues never liked spending too much time searching for the causes of market phenomena. If their signals met various measures of statistical strength, they were comfortable wagering on them.” (pg 204)

“Volume divided by price change three days earlier, yes, we’d include that” – Simons (pg 204)

To read on how to quantify trading edge check this out

You cannot run a trading business that relies on your emotional state or gut-instincts. There are too many days where you may be sick, tired, hungover, dealing with personal issues and what happens when these days line up with the most opportunistic market days?

Simons is 100% systematic and preaches the importance of treating trading like a business that can be backtested, modelled and followed. Here’s a quick minute long video where he explains why:

You Need a Great Team

Simons is no doubt successful on his own right, but Medallion’s performance really skyrocketed when Simons started building his team. Jim doubled salaries to hire people away from prestigious positions in tech, science, and academia.

Being around other smart, successful, and innovative people will only push you farther. The old saying “if you want to go fast go alone but if you want to go far go together” applies here.

Seek out other like-minded individuals and be open to sharing ideas. This is one of the greatest reasons I keep Build Alpha open to other traders. The ideas, inputs, and feedback help me create better software which allows all of us to create better portfolios. So, thank you for all the contributions, ideas, sound boards, etc.

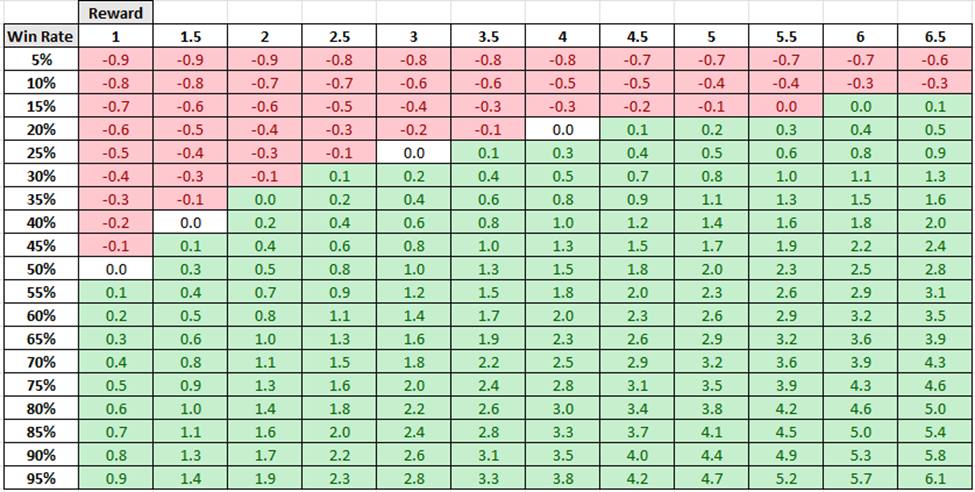

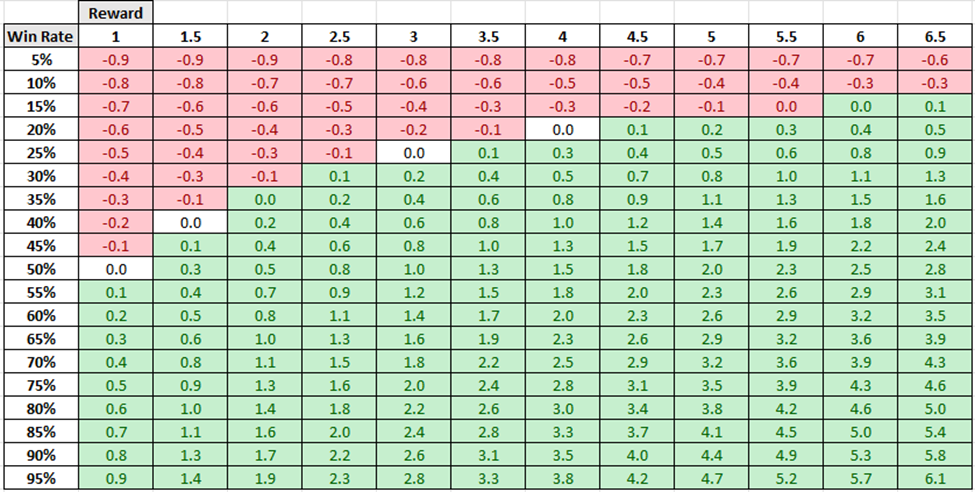

Edge Does Not Have to be Big

Renaissance searched for “overlooked” edges and joked about a 50.75%-win rate while utilizing the law of large numbers to win in the long-run. Seeking the perfect entry or exit or the one strategy is often a failed approach. Ren Tech generated astronomical returns with a nearly 50%-win rate. Much more can be gained combining unique smaller edges together than wasting time hunting for the holy grail.

Some of the trading signals they identified weren’t especially novel or sophisticated. But many traders had ignored them. (Page 112)

“We’re right 50.75 percent of the time… but we’re 100 percent right 50.75 percent of the time. You can make billions that way” (pg 272)

The Man Who Solved the Market – Gregory Zuckerman

Most of the quotes in this article are from this tremendous book. The book released in November 2019 and does such a great job covering Simons. Simons and Renaissance are very secretive about their strategies but there are a few insights (if you read between the lines) in the book.

Jim Simons Interviews and Videos

James Simons Full Length Numberphile Interview

The Mathematician who cracked Wall Street

James Simons – Mathematics, Common Sense and Good Luck

Famous Jim Simons Quotes

These quotes come from Zuckerman’s book along with page number. You can read into the lines and see why Simons is such a staunch supporter of the systematic trading approach.

Early on, he traded like others, relying on intuition and instinct, but the ups and downs left Simons sick to his stomach. (Page 2)

Simons and his colleagues used mathematics to determine the set of states best fitting the observed pricing data; their model then made its bets accordingly. The why’s didn’t matter, Simons and his colleagues seemed to suggest, just the strategies to take advantage of the inferred states. (Page 29)

“I don’t want to have to worry about the market every minute. I want models that will make money while I sleep”, Simons said. “A pure system without humans interfering.” (Page 56)

If a currency went down three days in a row, what were the odds of it going down a fourth day? Do gold prices lead silver prices? Might wheat prices predict gold and other commodity prices? Simons even explored whether natural phenomena affected prices. (Page 57)

Their goal remained the same: scrutinize historic price information to discover sequences that might repeat, under the assumption that investors will exhibit similar behavior in the future. Simon’s team viewed the approach as sharing some similarities with technical trading. The Wall Street establishment generally viewed this type of trading as something of a dark art, but Berlekamp and his colleagues were convinced it could work, if done in a sophisticated and scientific manner – but only if their trading focused on short-term shifts rather than longer-term trends. (Page 108)

Berlekamp also argued that buying and selling infrequently magnifies the consequences of each move. Mess up a couple of times, and your portfolio could be doomed. Make a lot of trades, however, and each individual move is less important, reducing a portfolio’s overall risk. (Page 108)

Humans are most predictable in times of high stress – they act instinctively and panic. Our entire premise was that human actors will react the way humans did in the past….we learned to take advantage.” (Page 153)

“Any time you hear financial experts talking about how the market went up because of such and such – remember it’s all nonsense”, Brown later would say. (Page 199)

By 1997, though, more than half of the trading signals Simon’s team was discovering were nonintuitive, or those they couldn’t fully understand. (Page 203)

“If there were signals that made a lot of sense that were very strong, they would have long-ago been traded out”, Brown explained. “There are signals that you can’t understand, but they’re there, and they can be relatively strong.” (Page 204)

The gains on each trade were never huge, and the fund only got it right a bit more than half the time, but that was more than enough. (Page 272)

his larger point was that Renaissance enjoyed a slight advantage in it collection of thousands of simultaneous trades, one that was large and consistent enough to make an enormous fortune. (Page 272)

The inefficiencies are so complex they are, in a sense, hidden in the markets in code,” a staffer says. “RenTec decrypts them. we find them across time, across risk factors, across sectors and industries.” (Page 273)

For all the unique data, computer firepower, special talent, and trading and risk-management expertise Renaissance has gathered, the firm only profits on barely more than 50 percent of its trades, a sign of how challenging it is to try to beat the market (Page 317)

To skip down to the best automated trading strategies click here.

What is an automated trading system?

An automated trading system is a set of rules that can be programmed for a computer to automatically execute trades whenever the rules occur in a given financial market. An automated trading system is the same thing as an automated trading strategy, an algo strategy, a trading algorithm, a trading robot or an algorithmic trading strategy.

In short, any pre-determined set of buy and sell rules that can execute trades automatically can be considered an automated trading system. Trading rules can be any set of if then scenarios and do not need to be complicated mathematical models.

Simple Automated Trading System Example

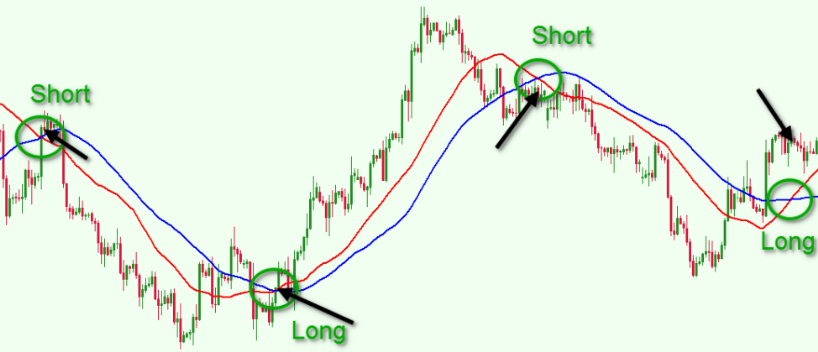

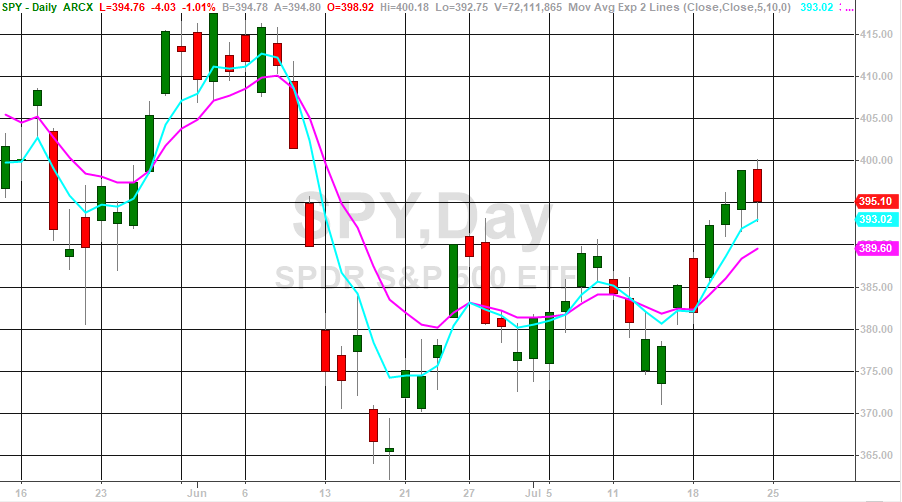

The simplest automated trading strategy is a moving average cross strategy. This system buys when the stock price rises above the moving average and sells when the stock price falls below the moving average.

Algorithmic traders have long known this strategy to lose its luster in financial markets, but this system is a great example of how simple buy or sell decisions can be made using technical indicators or market prices. If you can think it, then it can be coded.

Later we will get into much more complex algorithmic trading strategies and trading algorithms. However, I will not go into black box trading where strategies are known to the computer but not known to the human in charge of the computer.

How Does Algorithmic Trading Work?

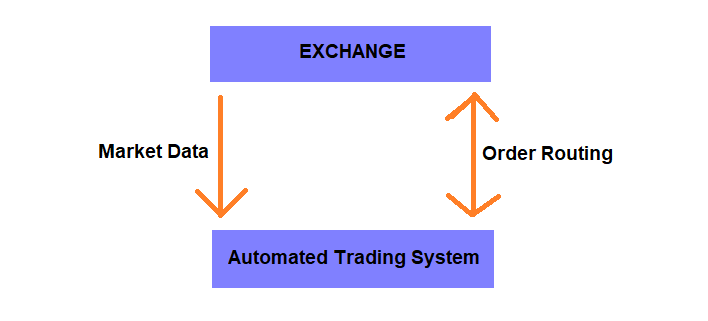

Algorithmic trading works over the internet allowing one computer or server to receive market data and send trading instructions to another computer or server. For instance, a high frequency trading firm may have their servers co-located in the exchange’s data center. This allows for lower latency in receiving new market prices and issuing new orders.

This server can also calculate the trading strategies and send buy and sell orders directly to the exchange. The exchange parses the message and executes the market makers’ desired actions.

Most trading systems communicate with the exchange through Financial Information Exchange protocol or FIX protocol. However, many independent traders have brokers that provide this communication connection built into the platform and most traders never have to worry about how algorithmic trading works.

Most platforms, brokers, and software provide application programming interfaces or APIs that make it easy to connect custom code to the exchange or broker. However, software like Build Alpha or TradeStation make it possible to connect directly with data providers, brokers, and the exchanges so traders only have to worry about entries, exits and risk management.

What are different types of automated trading systems?

There are various different types of trading strategies but let’s cover the five most popular strategies below. These strategies can apply for longer term investors or day traders. For a more extensive look please check out my Algorithmic Trading Guide.

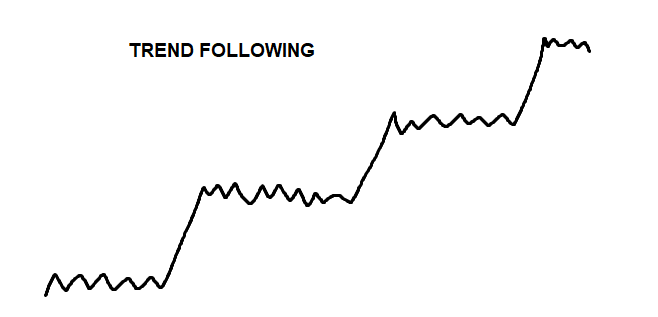

Momentum or Trend Following

Arguably the simplest and most widely used – especially amongst commodity traders. Trend following strategies aim to capture prolonged price movement in a single direction or a “trend”.

Trend strategies tend to have lower win percentages as these strategies have outsized winners in comparison to more frequent but smaller losers. The typical returns from a trend strategy may be a series of small losses and then one large win when the system captures the large trend move.

These strategies are best implemented by traders with strong resolve and the ability to withstand frequent losses. Periods of chop and noise are much more common than big trend moves thus leading to your trading account not making much progress most of the time and then making large leaps “at once”.

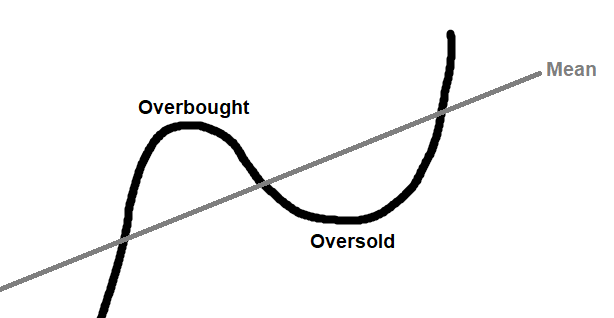

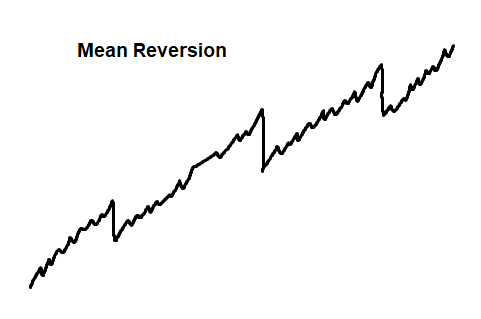

Mean Reversion

Mean reversion trading strategies tend to have higher win percentages as they have many frequent small wins and the infrequent large loss. The typical returns from a mean reversion strategy may be a series of small wins and then one large loss when the trend breaks.

The simplest mean reversion strategy is one that aims to buy and sell large deviations from a moving average or volume weighted average price. As price moves away from the mean, however calculated, the strategy looks to enter a position with the intention of price returning to the average price.

Many traders refer to these extremes as overbought or oversold and attempt to quantify them with technical analysis, technical indicators, mathematical models or statistical concepts.

In theory, traders that employ mean reversion strategies can experience profit and loss of their trading account to inch higher most of the time with periodic large set backs. Many market makers and dealers experience this.

Statistical Arbitrage

Typically, statistical arbitrage is looking for short-lived opportunities between two securities. Many traders will isolate two correlated or related stocks such as Coca-Cola and Pepsi and monitor the spread or difference between the two. Whenever the difference between the two becomes large enough the trader places a trade buying the cheaper and shorting the expensive until the pairing comes back into normal ranges.

An obvious simplification, but many traders cannot execute pair trading or statistical arbitrage with retail brokerage accounts and software. There is also steep competition from professionals, market makers and hedge funds.

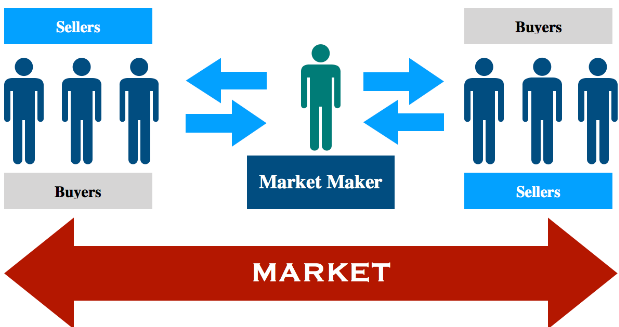

Market Making and High Frequency Trading

A market maker can be thought of as a liquidity provider that quotes both bids and offers regardless of market conditions. The market maker will hold inventory and aims to profit on the bid-ask spread or the difference between the highest price someone is willing to buy and the lowest price someone is willing to sell.

Market making is arguably the most complex form of algorithmic trading and automated trading as it requires tons of price data, quote information, data from multiple stock exchanges, active trading activities and trading decisions and is often completely automated with zero room for discretion.

High frequency trading (HFT) is market making or trading in fractions of a second based on powerful computer programs executing large numbers of orders almost simultaneously. The depths, pros and cons, and nuances of HFT and market making far exceed the scope of this post.

Pattern Trading

In the previously mentioned Algorithmic Trading Guide, I mention pattern trading as being one of the most common strategy types for algorithmic traders. This style was popularized by Jaffray Woodriff of Quantitative Investment Management in Jack Schwager’s Hedge Fund Market Wizards book (still one of my favorites).

This style looks for repeatable patterns that shift the odds one way or the other. For example, based on historical data, whenever this candlestick formation or these two events have occurred there has been a X% chance price is higher over the next N days. Again, a gross simplification, but a trading style most traders are familiar.

Is Automated Trading Profitable?

Yes. The leading 12 investment banks earned about $2 billion from portfolio and algorithmic trading in 2020 according to Coalition Greenwich. Additionally, the greatest hedge fund of all time – Renaissance Technologies – is strictly algorithmic. Listen to James Simons, the founder, speak from 36:48 to 38:00.

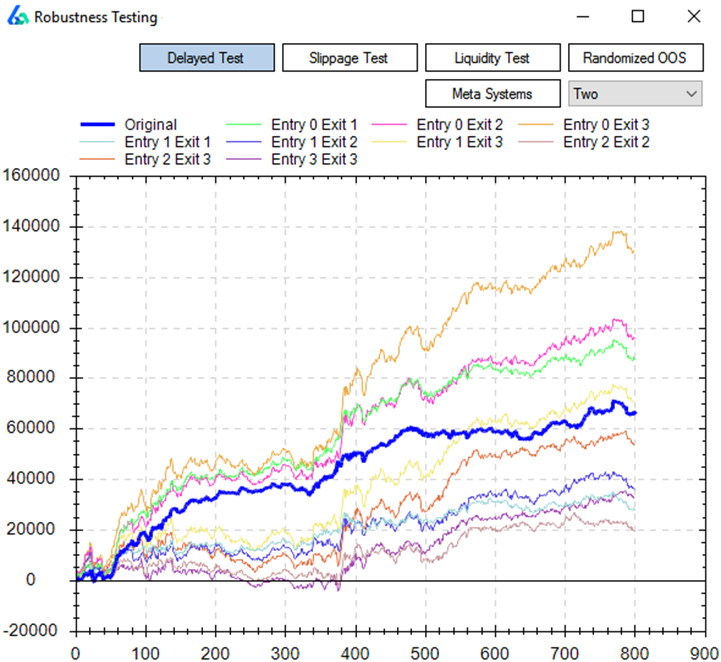

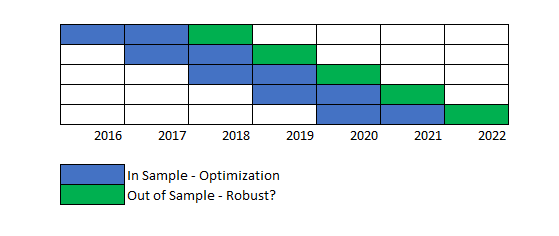

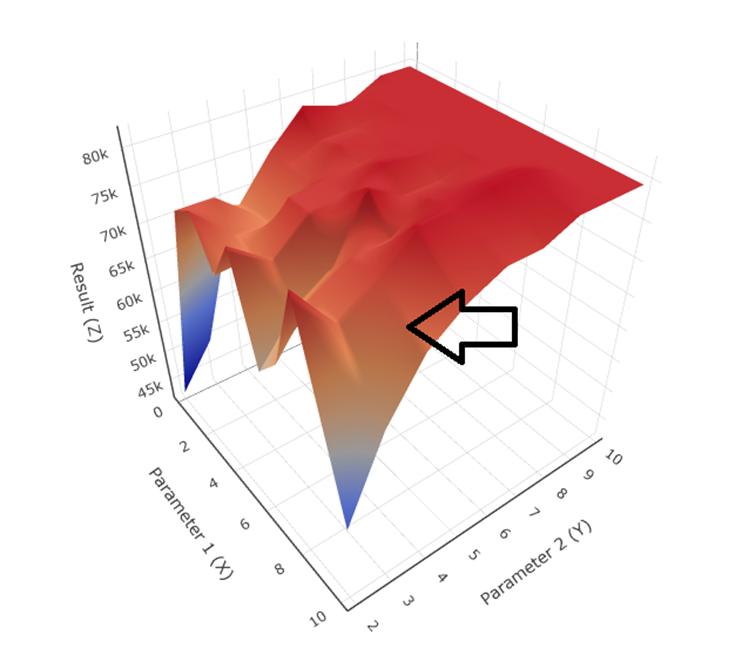

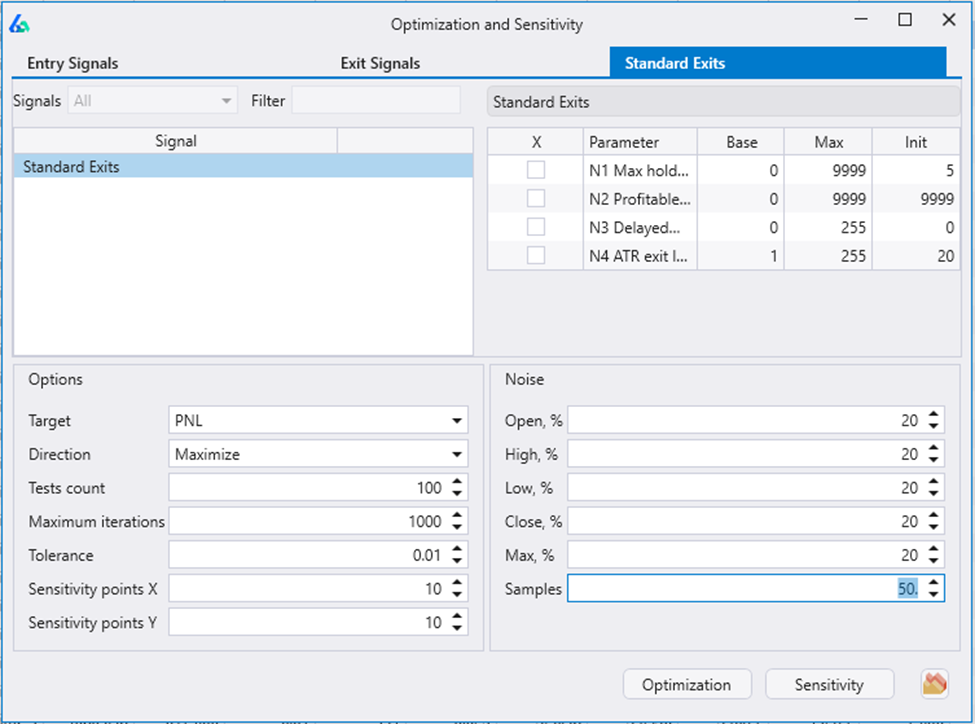

Furthermore, I have posted tons of algo trading success stories on the Build Alpha blog. Successful automated trading requires rigorous testing, robustness tests, stress testing, considering multiple market conditions, contextual data and more. Nothing manual trading does not require. I wrote a bit about strategy reliability here: Robustness Testing for Trading Strategies.

Can I automate my trading strategy?

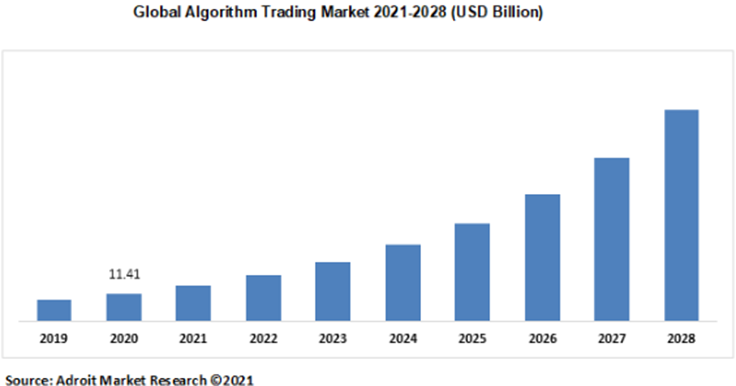

Yes. We live in the golden age of algo trading as nearly 75% of US equity volume now comes from algorithms while algorithmic trading is expected to grow at 11.23% CAGR over the next five years. Brokers and data platforms have made trade automation incredibly simple.

My goal with Build Alpha has been to connect those with a desire to automate trading strategies with the tools to do so without having to learn or write any code. Now anyone can test, build and automate their trading strategies without any code.

What’s the best automated trading software?

Build Alpha is the best automated trading software. I am biased because as I set out to find the best automated trading software, I could not find one that gave me the end-to-end tools necessary. That is what prompted Build Alpha’s development oh so many years ago. That being said, I will review the three most popular software for automated trading strategies.

Build Alpha

Build Alpha enables traders to create, test, and automate trading strategies with no code. There are 5,000+ built-in entry and exit signals as well as the ability for users to add their own signals with a drag and drop builder. The signal library includes everything from seasonality, price action, candlesticks, chart patterns, technical indicators, market breadth, options flows, economic data, time of day and more.

Build Alpha works in two ways. First, the trader can select specific entry and exit signals from the point-and-click interface to test a specific strategy. On the other hand, Build Alpha’s genetic algorithm can take thousands of inputs such as potential entries, exits, filters, risk management, position sizing, account size and will build the best possible strategies.

The trader can also specify certain thresholds that each strategy must pass such as the Monte Carlo simulation must be profitable or the profit factor must be above 1.7, etc. These automated workflows allow for the fast creation of strategies that fit any trader’s desired risk tolerance and performance thresholds.

Build Alpha then connects to live market prices for real-time strategy monitoring or can produce fully automatable code for every strategy. This code can be copy and pasted into various broker platforms for live trading.

Take a look at these to see step-by-step walkthroughs

TradeStation makes automating trading strategies very simple as TradeStation is a broker and has a really reliable platform which is a favorite among independent algorithmic traders. TradeStation also created Easy Language, a proprietary programming language aimed to make trading strategy development much simpler for traders.

Traders can write their strategy logic using Easy Language inside TradeStation’s Development Environment. Once the strategy’s code is complete, the trader can easily add the strategy to a chart to enable simulated or live trading.

A simple moving average crossover strategy may only require two lines of code using Easy Language. Here is an example below:

If Close crosses above average(close,10) then buy 100 shares next bar open;

If Close crosses below average(close,10) then sell 100 shares next bar open;

For those of you interested in a TradeStation account, email me to find out how TradeStation will pay for your Build Alpha license.

Python

Python is undoubtedly the fastest growing programming language due to its easy-to-read syntax and clean scripting style. Many traders have flocked to python as the vast number of public libraries that have already built trading functionality such as technical indicators and other position sizing logic coded continues to grow.

If you are interested in learning about using python to build automated trading strategies, then I highly recommend checking out a few other resources I have created.

How to create a trading algorithm in 3 Steps with Build Alpha

Build Alpha is the simplest way to create algorithmic trading strategies as it does not require any coding. Let’s take the moving average cross strategy above and build it in 3 clicks.

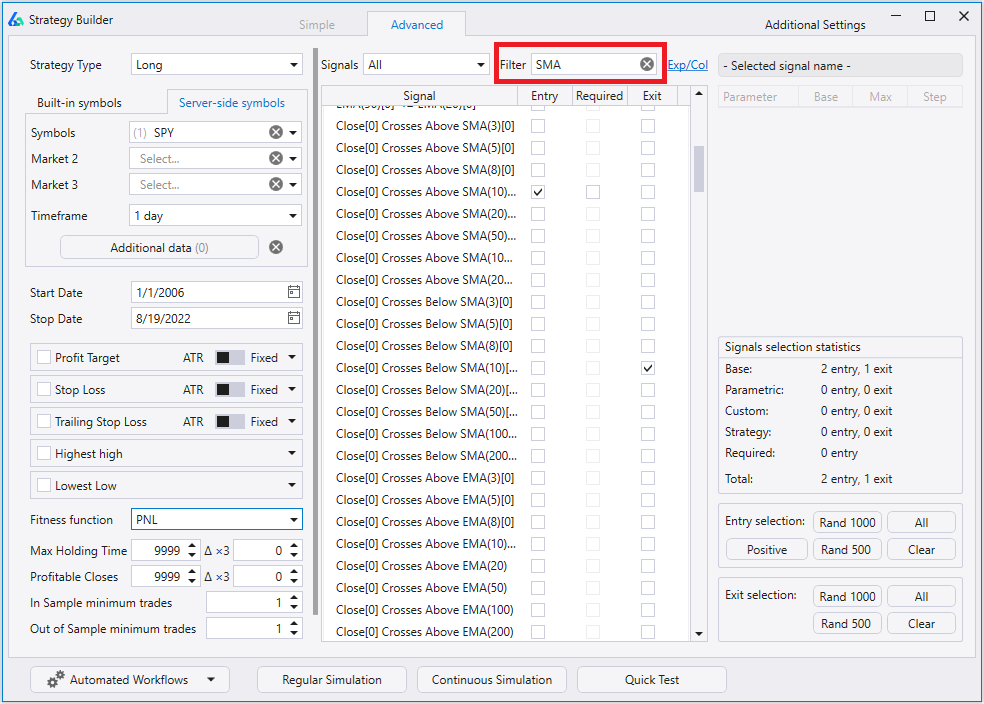

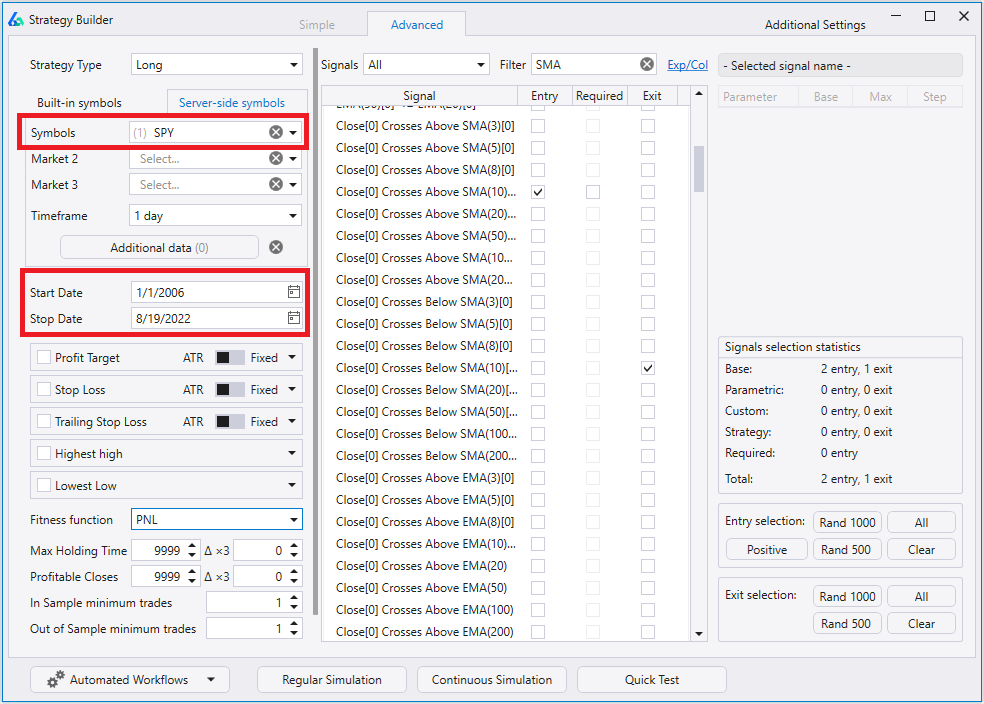

Step 1 – Select Signals

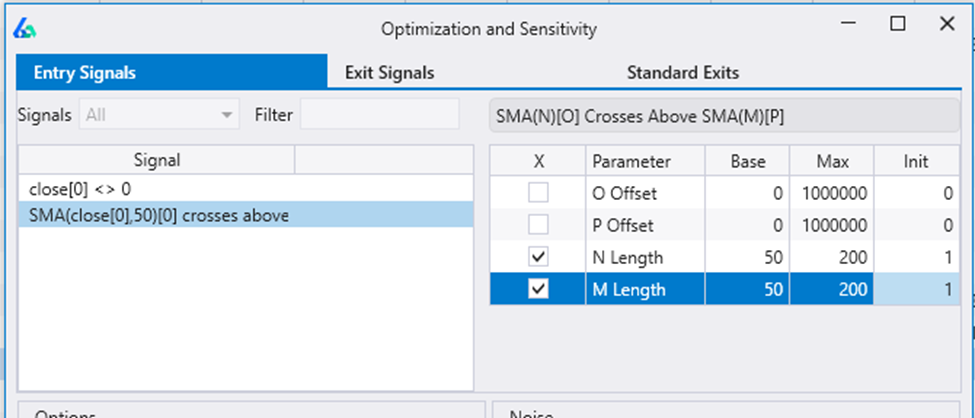

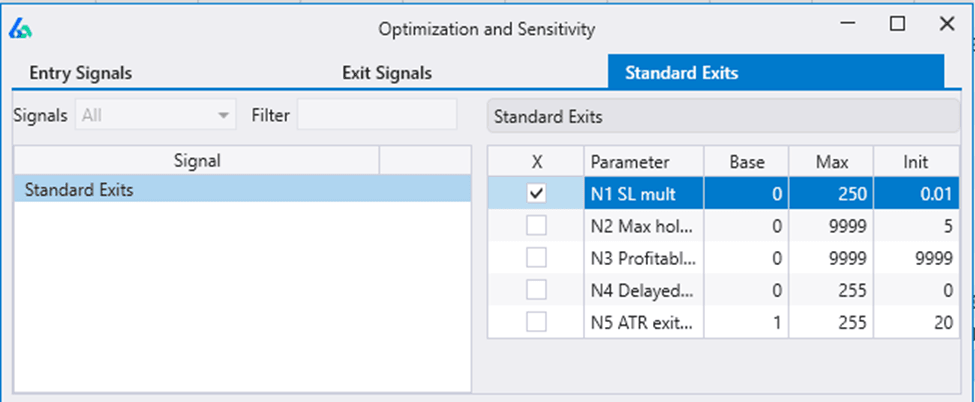

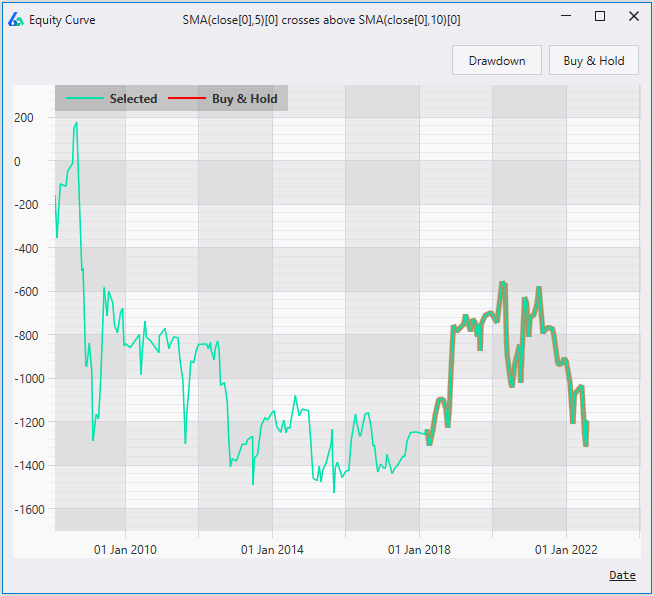

Search for SMA signals and select an entry and exit. Let’s enter when the close crosses above the 10-period SMA and exit when the close crosses above the 10-period SMA.

Yes, you can optimize parameters. I am showing the lazy hardcoded settings. Traders can create any range of parameters to test and optimize.

Step 2 – Select Dates and Symbol(s)

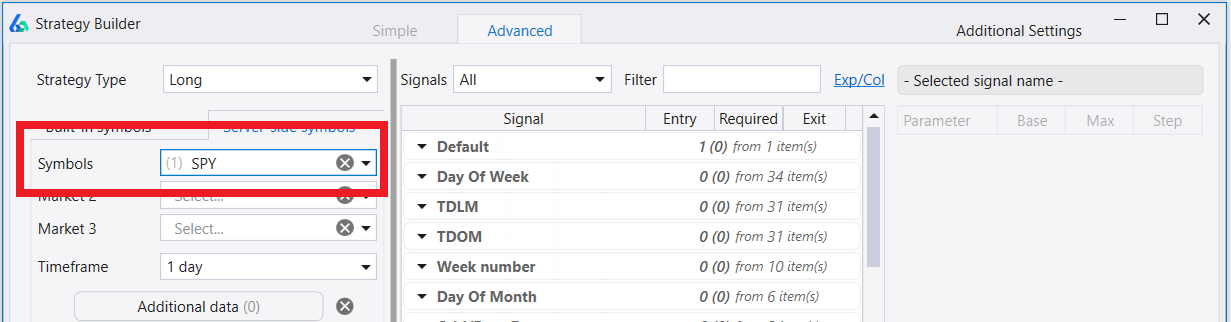

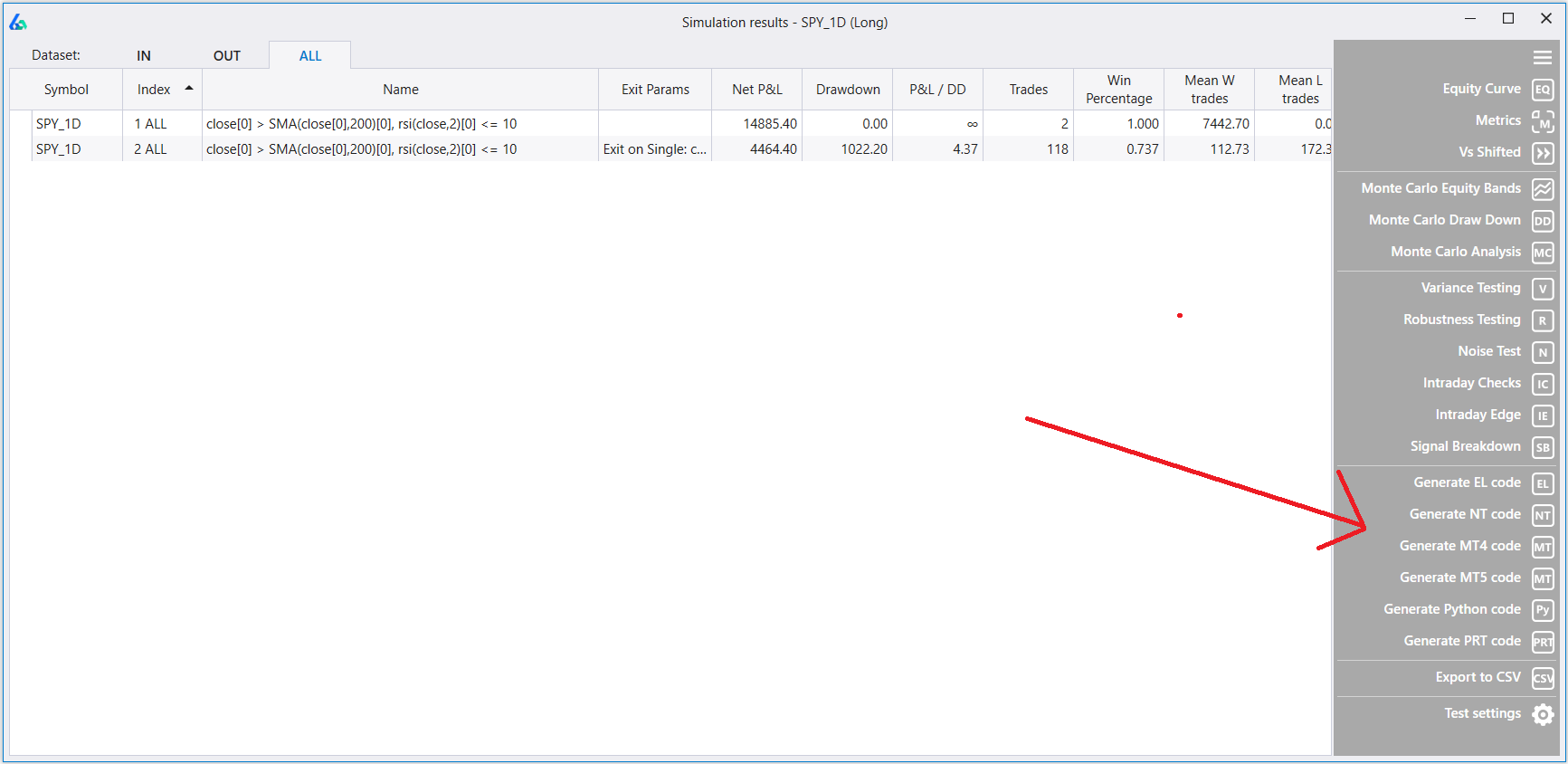

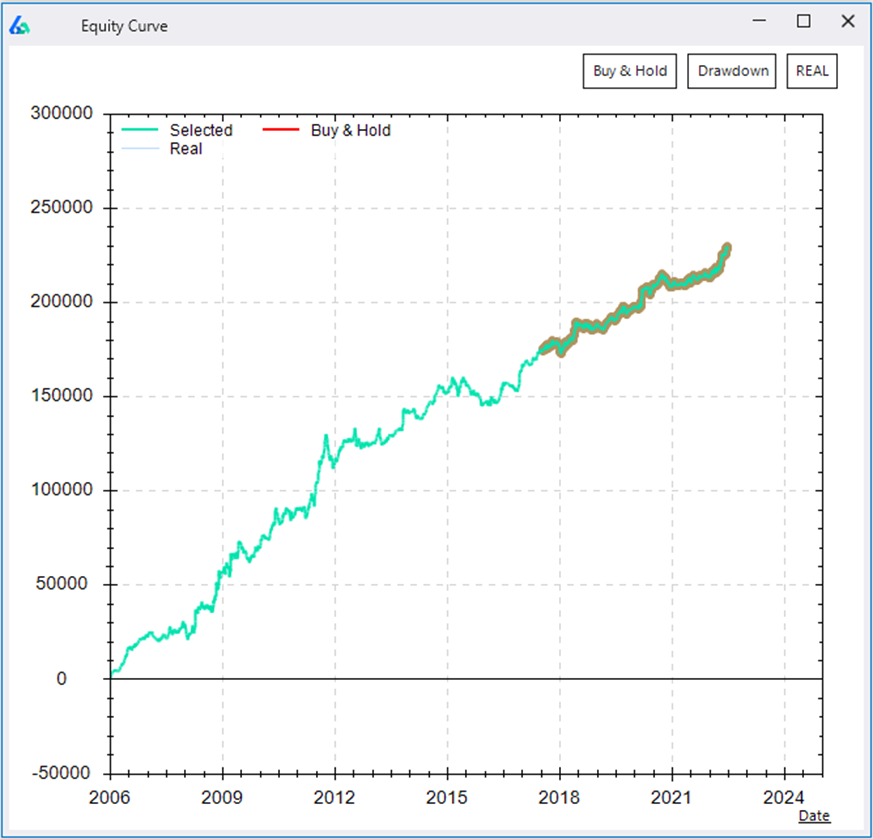

Select your test dates, symbol(s), and any risk management. I will select SPY and test from 2006 to 2022.

Step 3 – Simulate

Hit Simulate and view your results. If the results are suitable (they should not be) then hit one of the “Generate Code” buttons to get fully automatable code for this (or any) strategy.

It is important to note that Build Alpha permits automated trading strategy monitoring in two ways. First, you can export generated code. Second, you can connect your broker’s data feed with existing connections to TradeStation, Interactive Brokers, QuoteMedia, Binance, and more.

Example Automated Trading Strategy

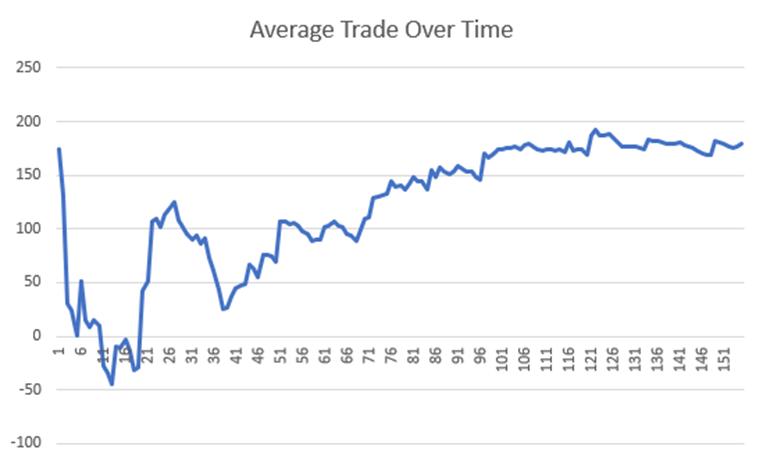

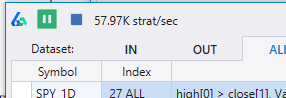

Later in this post I will share a table that automatically updates with the best technical analysis strategies for all financial markets. Each strategy uses one rule for entry and one rule for exit. These are meant to give insights to what is working now, building blocks for your own strategies, and general free information.

This strategy below has two rules: one for entry and one for exit. The trading strategy is applied to CSCO or Cisco Systems Inc which is a large multinational technology conglomerate.

This strategy enters when the closing price crosses below the 5-period exponential moving average (EMA) and exits when the closing price crosses above the 5-period exponential moving average.

At the time of publishing, you can see a sample of this strategy’s performance on the far right over the past 1,809 trades earning $18,138.17 per 100 shares traded over the last 12 months. This strategy also would have made $1,883.81 over the last 30 days.

What are the best automated trading strategies right now?

First, how do we define best? The simplest way is total P&L. Second, what is a trading strategy? In this case, let’s look at all possible combinations of technical indicators and only use one rule for entry and one rule for exit.

Can we build more advanced systems? Yes. However, this results table serves to show us what parameter settings, lookback ranges and indicators have been performing well lately. Perhaps this info can serve as building blocks for new automated trading strategies or just free information for my fellow system traders.

In the table below, you can sort by asset class, timeframe, ticker, and minimum trade count. All strategies are sorted by their total profit and loss over the last 30 days and last 12 months. All strategies use the same position sizing.

Key Points

Automated trading systems automatically execute buy and sell orders based on pre-defined rules.

There are at least 5 different types of algorithmic trading strategies

Trend Following

Mean Reversion

Statistical Arbitrage

Market Making / High Frequency Trading

Pattern Trading

It has never been easier to automate trading strategies – even with no programming

Build Alpha, TradeStation and Python are easier routes to algo trading

The best trading strategies are changing all the time, but the table above is free to all

Summary

Automated trading strategies continue to grow in popularity as traders with no programming background can now turn their strategies into trading algorithms. Automated trading strategies are just pre-defined rules that instruct a computer when and how much to buy and sell in financial markets. I have spent the past decade involved in professional trading and can honestly answer there is no best automated trading strategy. However, a combination of robustness testing and portfolio construction can help any trader gain an edge in algorithmic trading over the trader that fails to grasp these algorithmic trading concepts.

Author

David Bergstrom – the guy behind Build Alpha. I have spent a decade-plus in the professional trading world working as a market maker and quantitative strategy developer at a high frequency trading firm with a Chicago Mercantile Exchange (CME) seat, consulting for Hedge Funds, Commodity Trading Advisors (CTAs), Family Offices and Registered Investment Advisors (RIAs). I am a self-taught programmer utilizing C++, C# and python with a statistics background specializing in data science, machine learning and trading strategy development. I have been featured on Chatwithtraders.com, Bettersystemtrader.com, Desiretotrade.com, Quantocracy, Traderlife.com, Seeitmarket.com, Benzinga, TradeStation, NinjaTrader and more. Most of my experience has led me to a series of repeatable processes to find, create, test and implement algorithmic trading ideas in a robust manner. Build Alpha is the culmination of this process from start to finish. Please reach out to me directly at any time.

Automate Trading with No Coding | Complete Guide

Can you automate your trading?

Yes, you can automate your trading! In fact, according to BusinessWire, algorithmic trading is responsible for 60-73% of all U.S. equity trading. Most brokers support automated trading and even provide easy to learn programming languages to build your first automated trading system.

Three Ways to Automate Your Trading

Most broker platforms support automated trading with two options for automation. Build Alpha provides a third.

A development environment to add your own code and will execute your trades when your trading rules are true.

An application programming interface or API which allows your code to speak directly with the broker’s platform.

Build Alpha – a no code algo trading platform.

Both of the first two solutions require tedious hours learning to code, intricacies of the platform’s development environment or API, and introduces fragile breakpoints that can harm your trading results if you are not an experienced programmer.

Later in this article, I will introduce how you can still automate your trading with no coding using Build Alpha and a variety of popular brokers. The benefits of automated trading are still possible without the ability to program!

Is Automated Trading Profitable?

Absolutely. Automated trading is simply having a computer execute trades instead of you manually clicking the mouse buttons. The largest banks, hedge funds, and the best trader of all time are staunch supporters and users of automated trading.

I also highlighted several Build Alpha success stories (with statements) in my Algorithmic Trading Guide.

Many fear automated trading is not profitable because they fall for snake oil salesmen selling overfit trading strategies that were not developed to last but developed to sell. Automated trading requires robustness testing or stress testing to break the strategy before the market does. I wrote more about Robustness Testing here.

What is an automated trading system?

An automated trading system is a set of pre-defined entry and exit rules executed by a computer program. Many proper trading systems contain risk management and position sizing as well.

Simple Moving Average Example

The simplest example of an automated trading system, and probably the most popular technical analysis system, is the moving average crossover. In the moving average crossover system, a trading system would enter a long position when the faster moving average (shorter length) crosses above the slower moving average (longer length). The system would exit a long position when the faster moving average crosses below the slower moving average.

How do I automate my trading with no coding?

Build Alpha is no code algo trading software that allows traders to create hundreds of algorithmic trading strategies on historical data at the click of a button. No algo trading experience needed.

There are thousands of built-in entry and exit signals to choose from and the ability to create your own with a drag and drop builder or using python. The built-in library covers everything from

seasonality

price action

candlestick patterns

chart patterns

technical analysis indicators

volume

volatility

pre- and post-market

market breadth

options flows

economic data

dark pools

and more

Simply search and select your desired entry signals, exit signals, risk management and position sizing then hit simulate and Build Alpha will generate the best results.

From the results window, select your desired trading system then click on one of the code generators in the lower right. The code generator will produce fully automatable code that can be copy and pasted into any of the supported broker platforms.

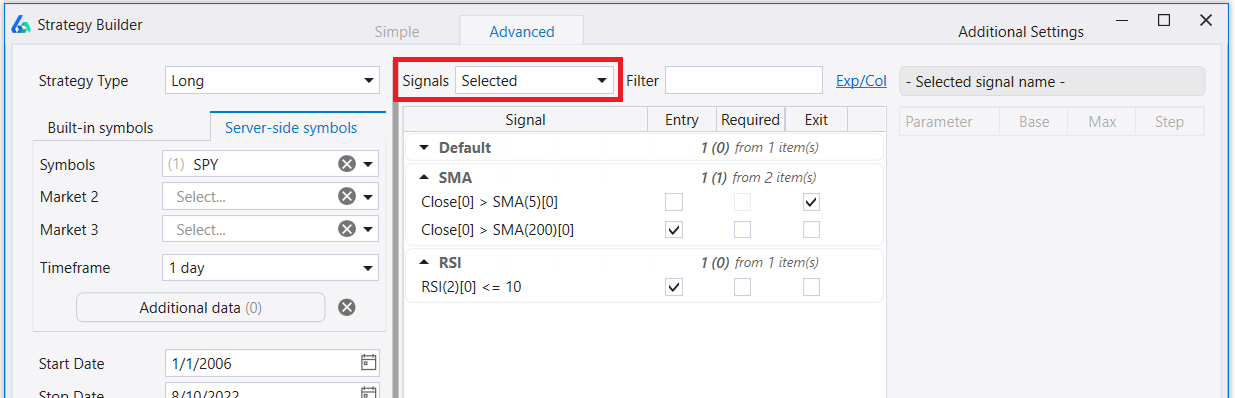

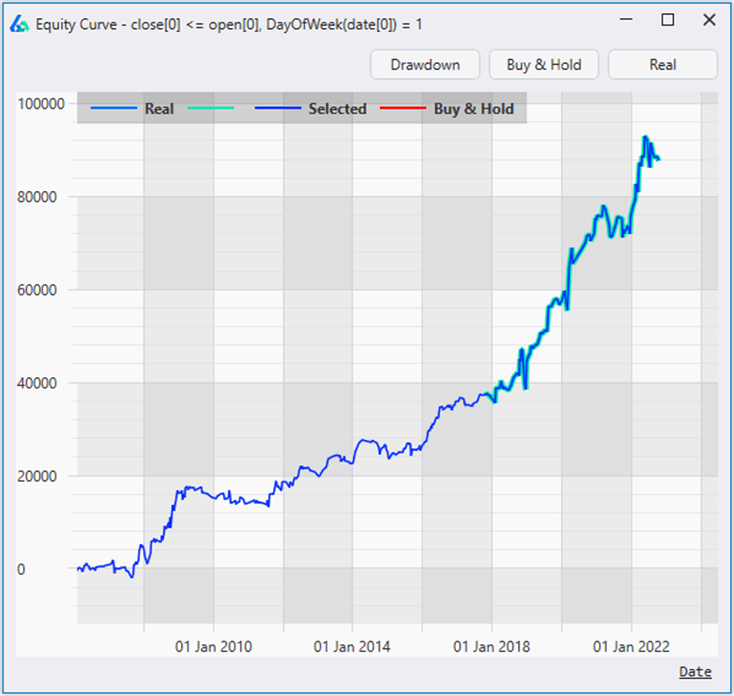

This strategy enters when the 2-period RSI is below 10 and price is above the 200-period simple moving average. On the other hand, this strategy sells when price is above the 5-period simple moving average.

Step 2 – Set account size and position sizing

We will use a fixed size of $10,000 per position. We achieve this by setting the account size to $10,000 and the position sizing to Fixed. Both are found in the settings menu.

Step 3 – Select Symbol(s)

Next, we need to select our symbol as SPY.

Step 4 – Select Entry and Exit rules

Finally, let’s select our trading decisions or entry and exit rules. The entry requires the following two conditions to be true

2-Period RSI is below 10

Price is above the 200-period simple moving average

Alternatively, the exit signal closes the trade when price is above the 5-day moving average.

Here is a quick gif searching and selecting the following entry and exit signals in Build Alpha.

Click on the gif to view/watch

Now that we see our results, we can highlight the strategy, review its performance metrics and equity curve, and ultimately generate code for it.

Step 5 – Generate Code

In the results window, highlight your strategy and navigate over to the lower right where you will find the Generate Code buttons. Find your preferred broker platform and hit Generate.

The Generate Code button will create complete code for the highlighted strategy that can be copy and pasted into your broker’s platform. Voila! Automated trading with no coding necessary. Steps for each broker below.

How do I set up my automated trading with Generated Code? Best Automated Trading Platforms

Great! How do we take the generated code and start auto trading buy and sell orders? Let’s walk through how you can take the generated code and set it up in the three most popular automated trading platforms.

TradeStation – Automated Trading Platform

TradeStation is arguably the consensus favorite among automated trading platforms. It is very easy to use, reliable and has competitive fees. Now you can partake in TradeStation algorithmic trading without being a tradestation coder.

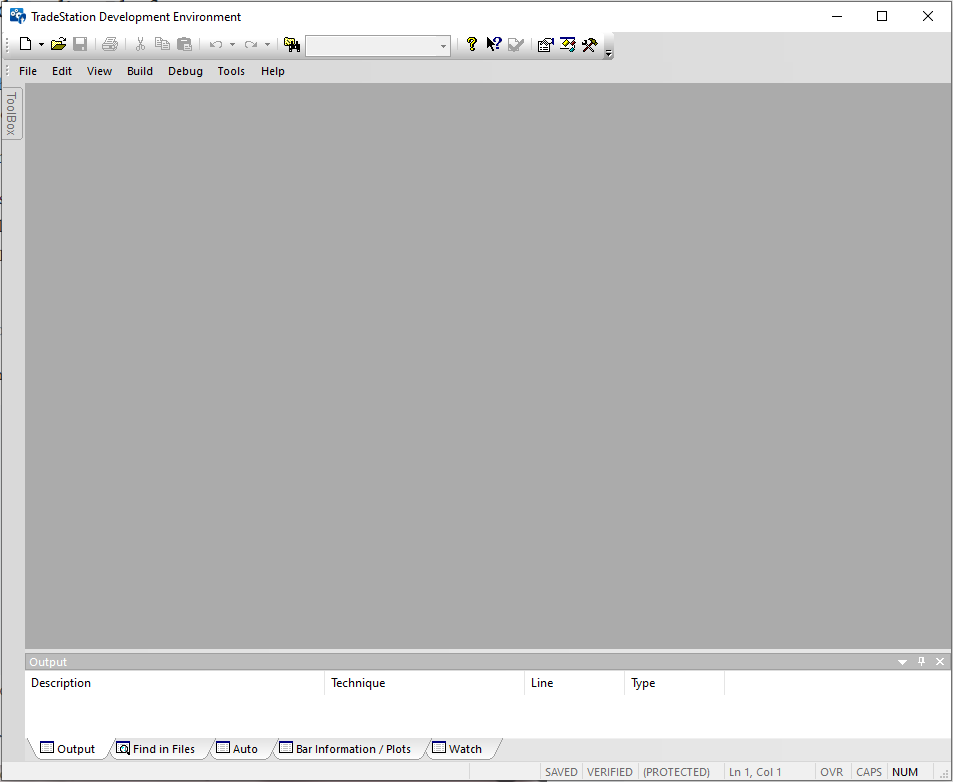

Step 1 – Open Development Environment

The first step to automating with TradeStation is to open the Development Environment found under View >> Development Environment.

Step 2 – Create new strategy File

Next, create a new strategy File >> New >> Strategy

Step 3 – Copy and Paste

Then copy and paste the Build Alpha generated code into the new Strategy and hit F3 to verify. You can hit CTRL+A to highlight all the Build Alpha generated code then CTRL+C to copy it all. Then inside the new Strategy in TradeStation’s Development Environment you can hit CTRL+V to paste it all.

Step 4 – Add to Chart

Finally, open a new chart and set it with the symbol you wish to trade. Then right-click and select Insert Strategy!

Please note this is an older version of Build Alpha’s results window. There are many more features now!

As part of TradeStation’s confidence in the software, we have partnered to help traders have the best of both worlds. If you open a new TradeStation account and license Build Alpha then TradeStation offers a commission rebate plan to repay you until they have paid for your license. For more information, please check out TradeStation Build Alpha promo.

NinjaTrader – Automated Trading Platform

NinjaTrader8 is a close second and highly favored automated trading platform among futures traders. Below are four simple steps to take Build Alpha generated code and enable inside NinjaTrader8. That’s right, you can generate and trade NT8 scripts without being a ninjatrader coder.

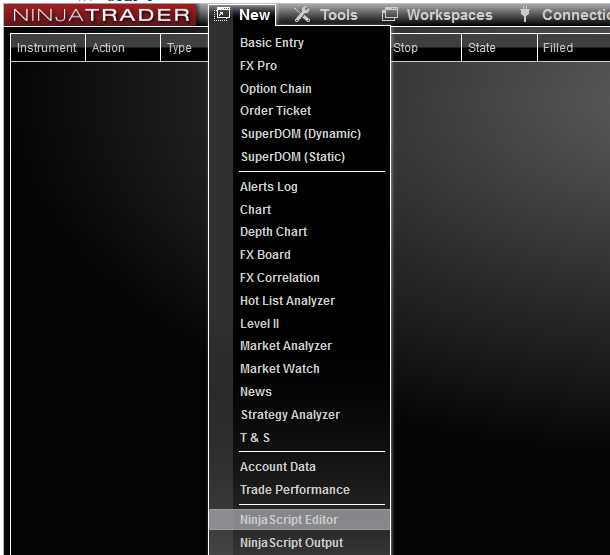

Step 1 – Open Script Editor

Open up the NinjaScript Editor

Step 2 – Create new strategy file

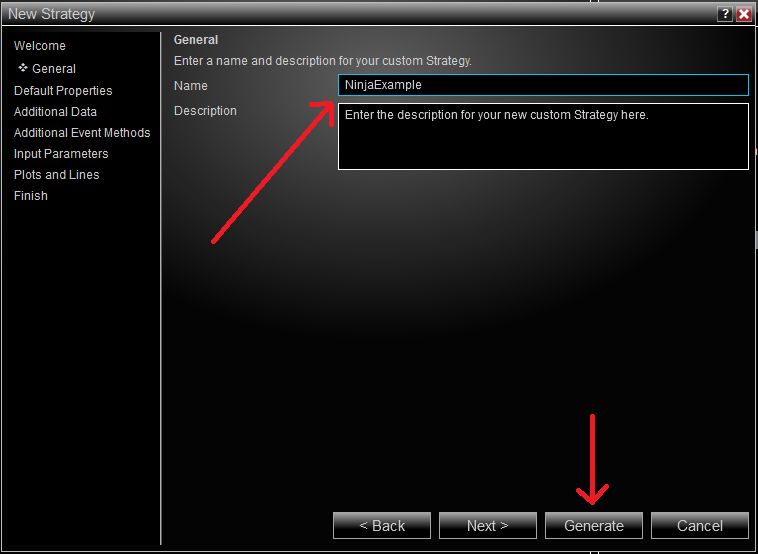

In the NinjaScript Editor, right-click on Strategies to create a new one.

Step 3 – Name your strategy

Name your strategy and hit Generate.

Step 4 – Copy and Paste

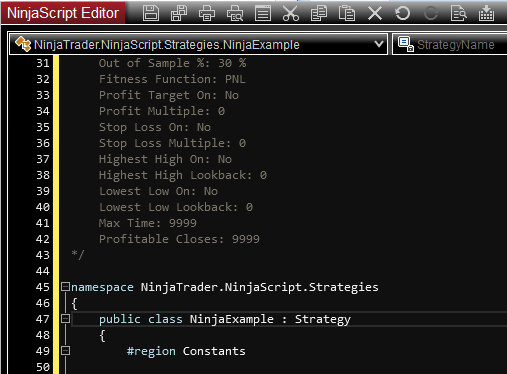

In the new NinjaTrader Strategy that appears, please hit CTRL+A to highlight all text and then hit ‘BACKSPACE’ to delete it all. Then inside Build Alpha, hit Generate NT Code. Please highlight and copy all the generated code using CTRL+A, CTRL+C. Then come back to the blank NinjaTrader Strategy and hit CTRL+V to paste it all.

Step 5 – Quick Edit

Go to line 47 and edit the class name to be the same as the designated strategy name. You can go to line 47 by hitting CTRL+G then entering 47. I named the strategy NinjaExample.

After making this change you can verify or compile the strategy by hitting the above button.

Step 6 – Add to Chart

Open up your desired chart, right-click and select Strategies. Alternatively, you can hit CTRL+S.

Step 7 – Enable

Select your strategy and be sure to enable the strategy in the Properties pane.

That’s a wrap. Ninjatrader automated trading systems without writing a single line of code in your ninjatrader scripts.

MetaTrader4 and MetaTrader5 – Automated Trading Platforms

MetaTrader4 and MetaTrader5 are both supported by Build Alpha’s code generators. However, most traders should migrate to MetaTrader5. In a recent Build Alpha survey, MetaTrader was the lowest ranked automated trading platform among the three listed in this article. I highly encourage you to check out the other two if you are currently struggling with MetaTrader.

Step 1 – Open MetaEditor

Open MetaEditor. This can often be done from your search menu or from within MetaTrader.

Step 2 – Create new EA

Create a New Expert Advisor. Expert Advisors are what MetaTrader calls strategies. Give your expert advisor any name you desire. I will use MetaExample.

Step 3 – Copy and Paste

In the new strategy that appears, please highlight and delete all text. You can hit CTRL+A and ‘BACKSPACE’ as we have done before.

In Build Alpha, hit the Generate MT4 Code or Generate MT5 Code button. Then highlight and copy all the text. This can be done using CTRL+A, CTRL+C. Back in the MetaEditor, paste all the generated code using CTRL+V. Then hit the Compile button in the top menu.

Step 4 – Add to Chart

You can now add expert advisors to the tester or a live chart.

Can I automate my day trading?

Absolutely. Build Alpha has time frame selection, time of day filters, and a Force End of Day Exit option that forces any strategy to close open positions at the specified time.

The pre- and post-market signals allow traders to specify signals around volume weighted average price (VWAP), pre- and post-market volume or pre- and post-market highs and lows.

The Quick Test feature even allows you to test a strategy across thousands of symbols and view the optimal times to take profits, stop out, or when highs and lows of the day are made. The test even shows you most profitable and least profitable symbols as well as a summary across all tickers.

Please note it is best that day traders do not use excessive leverage or size as there is a high risk of losing money rapidly due to leverage.

Automated Trading Pros

What are the benefits of automated trading?

More Markets

Market data moves so quickly, and manual trading can rarely keep up. There are often missed trades during fast moving market conditions. Automated strategies can be one of many trading solutions to help.

Trading more markets, more systems can often mean getting to the law of large numbers faster. If your systems have edge, then this means a rising account.

Quantified Risk

Experienced traders know that having a set of rules with a risk you can afford to take is the key to financial longevity. New traders seeking massive upside often take the high risk and lose money because they do not have a system or have properly quantified their trading edge.

Computer Never Sleeps

Certain financial markets like futures, forex and cryptocurrencies trade 24 hours per day. There are tons of trading account opportunities in off market hours and auto trading and automated trading strategies can help.

Fewer Mistakes

Trading is hard. Losing your money sucks. Losing your money from human errors like fat fingering an order or entering the wrong symbol suck even more.

Automated systems help avoid these blunders. Consider whether you understand how big of an impact this can have on your emotional state. No more calling customer support to see if they will cancel a trade.

Less Emotions

Backtesting trading strategies and understanding how a system can make money or lose money over the next N trades is crucial to reducing emotions. If you have a plan, you can stick to it.

If you do not have a plan, then losing your money heightens stress, which heightens emotions, which raises your probabilities to harm your trading account.

Known Systems

Automated trading is much more than automatic order entry. Advanced trading work is understanding edge, setting proper expectations, and quantifying your risk. Many investors do not know their systems and cannot properly answer these above questions. How do you think these traders wind up?

Automated Trading Cons

Where to Start with Automated Trading?

There are so many markets, symbol, timeframes and potential signal combinations. New traders often do not know how to start. The simplest solution is to start quantifying what you do know. For example, does price need to be above a moving average? What moving average? Does yesterday need to be a bullish or bearish day? What about volume?

I wrote here about quantifying simple ideas:

Solution: Build Alpha does not require you to have a trading idea. You can of course test your own ideas, but if you do not have an idea you can select thousands of input signals at once and Build Alpha will find the best strategies for you. The genetic algorithm learns from your inputs and creates the best combinations quickly.

Computer needs to be on 24 hours?

Yes, if your computer is not connected to the internet or turned off then the automated trading systems will not send orders to the broker’s trading platform.

Solution: Rent a virtual private server (VPS) which is a computer that is on 24-7 which you can remotely log into. Amazon, Microsoft and other smaller companies have been reliably offering this service for years and often you can rent a VPS for only a few bucks per month. All PCs have remote monitoring software built-in.

What if my trading signal is not included in the built-in signals?

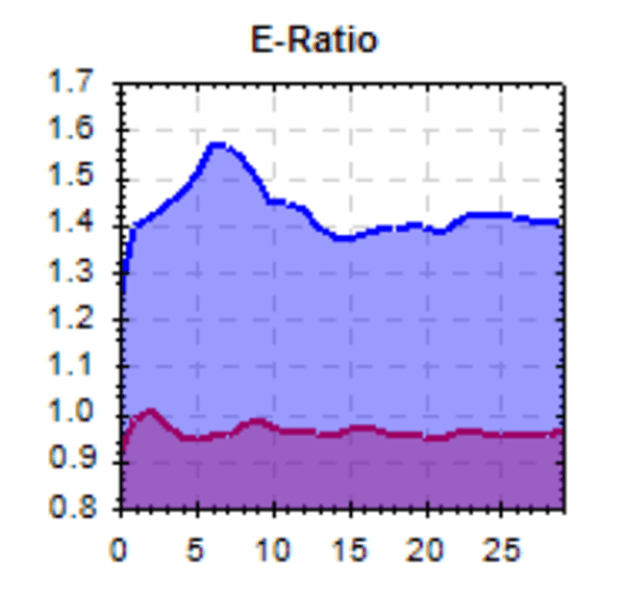

There are nearly 5,000-plus signals built-in, and I have done my very best to include those with above average e-ratios, but it is possible that your trading idea requires something unique.

Solution: Build Alpha has two ways to add custom signals that can be passed to the strategy builder engine. First, there is a drag and drop signal builder. It allows the trader to combine any technical indicator, math operator, and custom parameter setting.

Anyone can automate their trading even without programming

Automated trading pros outweigh the cons

Most brokerage platforms support automated trading now

Summary

Automated trading is growing every year with now nearly three quarters of U.S. stock market volume being attributed to automated trading. In the past, creating automated trading systems required access to historical market data, live market data, broker connections, and the ability to program it all. However, now, Build Alpha provides professional automated trading software to all traders. This enables all traders to create, test, and automate any trading strategy on a variety of automated trading platforms.

Automated trading platforms support both demo account and live account implementations. Cryptocurrencies, Forex, CFDS are complex instruments and come with a steeper learning curve and intricate nuances, but traders can focus on futures, stocks and ETFs as all markets are automatable.

Author

David Bergstrom – the guy behind Build Alpha. I have spent a decade-plus in the professional trading world working as a market maker and quantitative strategy developer at a high frequency trading firm with a Chicago Mercantile Exchange (CME) seat, consulting for Hedge Funds, Commodity Trading Advisors (CTAs), Family Offices and Registered Investment Advisors (RIAs). I am a self-taught programmer utilizing C++, C# and python with a statistics background specializing in data science, machine learning and trading strategy development. I have been featured on Chatwithtraders.com, Bettersystemtrader.com, Desiretotrade.com, Quantocracy, Traderlife.com, Seeitmarket.com, Benzinga, TradeStation, NinjaTrader and more. Most of my experience has led me to a series of repeatable processes to find, create, test and implement algorithmic trading ideas in a robust manner. Build Alpha is the culmination of this process from start to finish. Please reach out to me directly at any time.

Stop Losses | Complete Guide and Test Results Reveal

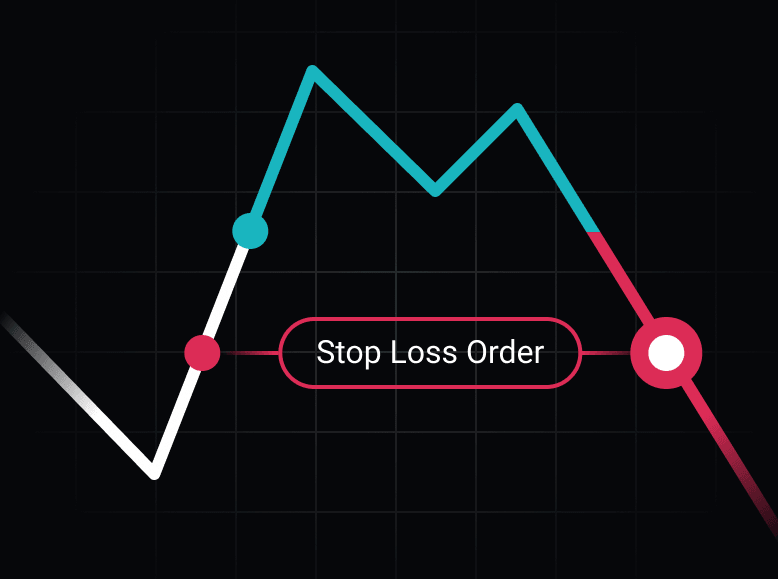

What is a Stop Loss?

A stop loss is an order to close an existing position to limit losses when the market reaches a certain price. A stop loss is a form of risk management and intends to serve as protection from more severe trading or investing losses. The purpose of a stop loss is to automatically exit a trade when the trader cannot stomach more pain in the trade or the set up has been invalidated. Before we get into all the types and variations of stop losses including the trailing stop loss, let’s become masters of understanding stop losses as a money management tool.

How Does a Stop Loss work?

A simple stop loss example is Cody buys 100 shares of Apple stock at a purchase price of $104.00 to open a long position (aiming to profit from a rise in AAPL stock). Cody does not want to risk more than $200 on his trade.

If AAPL’s price falls to $102.00 then Cody’s 100 shares would result in a $200 loss. Cody can set a stop loss order at $102.00 so that if and when AAPL falls to $102.00 his shares will be automatically sold.

When the market price reaches the stop price, the stop-loss order is converted to a market order and is generally executed immediately thereafter assuming during market hours. It is important to note that the market’s liquidity will determine the actual fill price of the stop loss order after conversion to a market order.

If there is a buyer bidding to buy at least 100 shares at $102.00 then Cody’s stop loss order will sell to that buyer at that share price thus closing his position for a $200 loss.

However, if the best bid for 100 shares is at a lower price of $101.98 then Cody’s stop market order to sell will be executed at a stock price $0.02 below his stop level resulting in a loss of $202. This is because the stop loss order converters to a market order and takes the available current market price.

Market Price or Limit Price? What is the difference between a Stop Loss and a Stop Limit Order?

In the example above, the best bid could have been $101.08 instead of $101.98 and when price falls below the stop and the next available market price is significantly below the trader’s desired exit level then significant losses may ensue.

What if in this scenario Cody would prefer to hold the position and wait for the share price rises or current price to recover before selling?

The stop limit order allows the trader to enter a stop price and a limit price which converts the stop order into a limit order (instead of a market order) after the stop price has been hit. Then the trade will be executed at the limit price (or better). This could alleviate some of the concerns around market orders.

Let’s revisit Cody’s position from earlier and assume he placed a stop limit order with a stop price of $102.0 and limit price $101.90. In the first example, Cody’s transaction price would be $101.98. In the second example, Cody’s stop would trigger but the limit order would never execute because price was already below his limit price ($101.08 vs $101.90). In this scenario, Cody would hold the shares and until the security price rebounds (hopefully).

The big difference is that a stop loss converts into a market order and a stop limit order converts into a limit order. The risk with stop limit orders are thinly traded markets or gaps beyond the stop limit. There are no stop limit orders guarantee to get filled at the specified limit price.

How to Calculate Stop Prices? Where to place them?

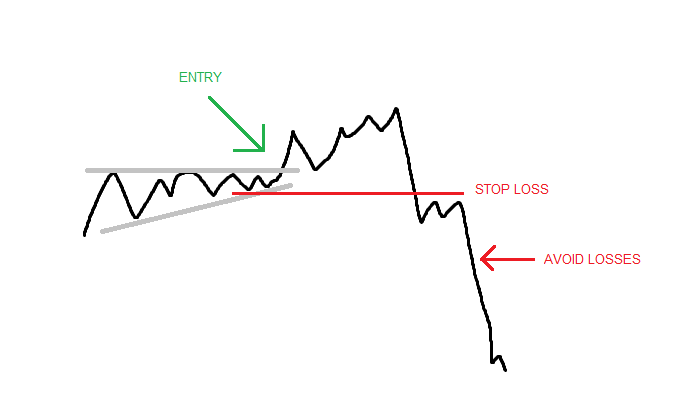

Method 1: beyond a recent high or low-price level

Those using technical analysis and chart patterns to trade will advise you to put a stop below (above) a recent low (high) that would invalidate the chart or pattern that prompted the entry.

However, one should not choose the minimum price below the most recent low but a decent margin below the recent price level so all the stock drops and natural volatile markets can happen without stopping you out of your position prematurely.

However, I have now spent years working with a high frequency trading, market making firm and I can assure you this is not a great strategy for existing positions especially in fast moving markets. We joke and call this the “draw a line stop loss”. This rings true for long and short positions and all trading hours.

Method 2: based on your risk tolerance

Another exit strategy to determining when to sell stocks on adverse price moves is to determine your entry, determine how much you are willing to lose and place your stop sell order at this amount. This may apply to traders that have pre-determined their position sizing based on the entry or their account size.

This strategy lacks forethought and traders must realize the market does not care where your pain threshold is. You may choose a price level that can be hit easily.

Method 3: something testable

Calculating stop loss orders is no different any other part of your trading system; that is, it should be fully testable. Often times using method one above does not result in something that can be backtested. Often times backtesting can result in isolating situations that produce more money or more favorable market conditions. This can also apply to placing sell stop or limit orders. Some easy ideas for something testable are:

fixed dollar amount

fixed Average True Range amount

dynamic dollar amount

a rolling N-day low (or high for a short position)

What is a Trailing Stop Loss?

A trailing stop loss aims to protect profits moving the stop price higher as the market price moves higher. Trailing stops are often an excellent tool to protect gains and combat market volatility that wishes to shake you out of profitable positions. Of course, one can use either a trailing stop market order or a trailing stop limit order.

As the trading day progress and the trade becomes more profitable, the trailing stop can be updated instantaneously or at the end of each bar.

How to Calculate a Trailing Stop Loss?

Trailing stops are typically calculated from the maximum trade price or high watermark while in a long trade. Short positions just have reversed logic calculating from the minimum trade price during the trade.

Cody’s original transaction price was to enter a long trade at $104.00. Let’s assume Cody placed a $1 trailing stop which would initially start at $103.00 or $1.00 below his entry price. After the market opens, AAPL’s price shot up to $104.77 raising Cody’s trailing stop price to $103.77.

If trading fails to make a new high above $104.77 then Cody’s trailing stop would remain unchanged at $103.77. However, if the security price rises to a maximum price of $105.66 then Cody’s trailing stop would move to $104.66 which is above his entry price of $104.00. At this point, Cody has “locked” in some gains even if price drops. However, investing involves risk and anything can happen (look above to thinly traded or overnight gap risk comment).

What is the best Stop Loss strategy? Static or Dynamic?

Stop losses, stop limit orders, trailing stops, oh my. What are the best stop loss strategies to add to your trading systems? First, let’s discuss a few variations of what we have discussed so far.

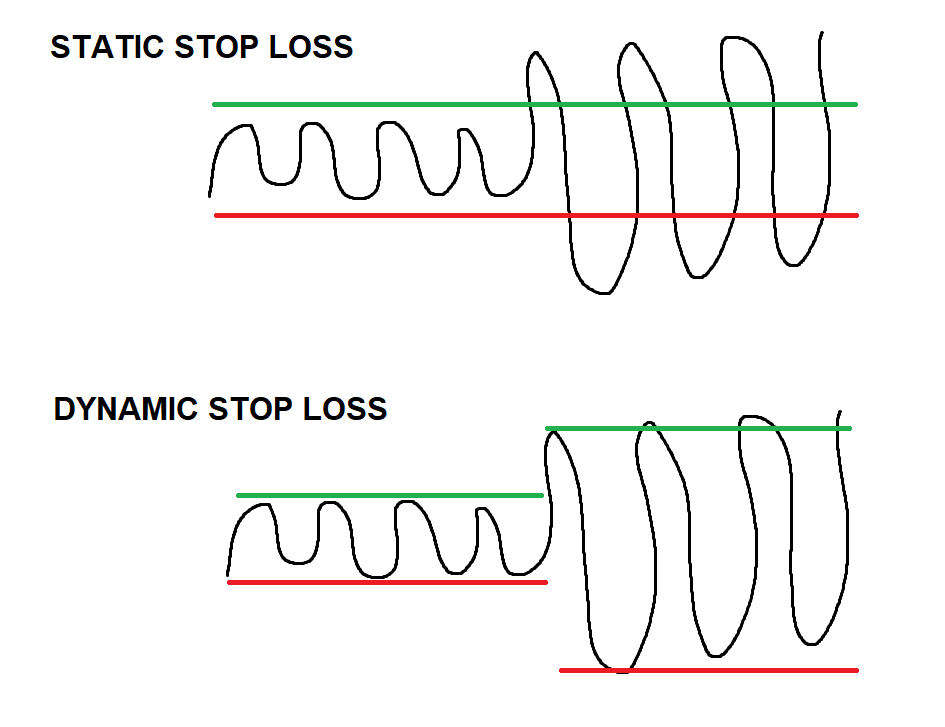

Static vs Dynamic Stop Losses

A static stop loss is a stop that is calculated the same way regardless of the current market price and market volatility. For example, a trader may employ a $200 stop for every trade he places regardless if the stock price significantly moves from the time of his first trade to the time of his most recent trade.

Static Stop Loss Pros

Simplify what to expect

Always understand your risk

Easy to think in fixed (static) terms

Static Stop Loss Cons

Fails to account for changes to underlying

Fails to account for different volatility regimes