The Taguchi Method,

Robust Design, and

What It Means for

Trading Systems

Genichi Taguchi’s framework for designing systems that are less sensitive to noise maps directly to algorithmic trading. This guide explains the method, translates it into trading language, and shows how Build Alpha applies these principles automatically.

Table of Contents

- Who Was Taguchi?

- What Is the Taguchi Method?

- Core Idea: Controllable vs Noise Factors

- Injecting Noise Into the Process

- The Trading Lens: Taguchi in Build Alpha

- Inner Array and Outer Array

- Signal-to-Noise Ratio for Strategies

- Case Study: Noise Test Pass vs Fail

- 3 Practical Robustness Formulas

- Automated Robustness Workflow

- A Necessary Caution

- FAQ

Who Was Genichi Taguchi?

Genichi Taguchi was one of the major names in quality engineering and experimental design. His systematic approach to off-line quality control was first adopted in Japan, then attracted significant attention in the United States, Germany, the UK, and China. His methods were praised for emphasizing not just hitting target values, but reducing variation around those targets.

Taguchi became influential not because every detail of his method was perfect — some were heavily criticized — but because he helped popularize a very powerful idea:

The Taguchi Principle

A good design is not just one that performs well on average. It is one that performs well even when noise and variation show up.

That single idea has aged very well. And for successful algorithmic traders, it should sound extremely familiar.

What Is the Taguchi Method?

The Taguchi Method is a framework for designing products and processes so they are less sensitive to variation. Taguchi defined quality in terms of the loss caused when performance drifts away from a target — not just whether something barely passes a spec sheet.

Expected loss depends on both how far the average result is from the target and how much the result varies around that average. This shifts the focus away from pass/fail thinking.

A design that looks great in one narrow setting but falls apart under small disturbances is not truly high quality. In Taguchi’s view, that design still creates loss.

For traders: a strategy with a beautiful backtest that collapses under slight parameter changes, different date ranges, or noisy data is not a robust strategy. It is an overfit strategy — and Taguchi would call it a poor design.

Core Idea: Controllable Factors vs Noise Factors

Taguchi’s key insight is separating factors into two groups:

Controllable Factors

The things the designer chooses. In trading: entry logic, exit logic, stop and target behavior, holding period, timeframe, filters, portfolio weighting, and position sizing.

Noise Factors

The things that create variation and cannot be fully controlled. In trading: market regime shifts, volatility changes, spread and slippage variation, different sample windows, start-date sensitivity, execution imperfections, small parameter changes, and synthetic or perturbed market paths.

The goal is to choose controllable settings so the output becomes less sensitive to noise factors — not by controlling the noise (you can’t control markets), but by designing the strategy so it doesn’t need the noise to cooperate.

That is robust design in one sentence. And it is the foundation of every robustness test Build Alpha offers.

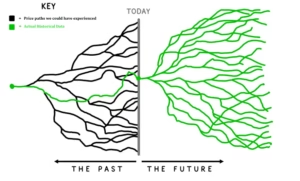

Injecting Noise Into the Process

One of the most useful parts of Taguchi’s framework is that it doesn’t just acknowledge noise conceptually. It brings noise into the experiment.

Taguchi recommends using an inner array for controllable factors and an outer array for noise factors. For each candidate design, the experiment is run across multiple noise settings, and the mean and variance of the response are analyzed together.

In modern trading language, that translates directly to:

The Taguchi Approach to Testing

Do not just test your strategy in a clean environment. Disturb it on purpose and see what survives.

In trading, modern equivalents of “injecting noise” include:

- Slippage and spread changes

- Alternative start dates and date ranges

- Shuffled or perturbed samples (Monte Carlo simulation)

- Regime variation (trend vs chop, high-vol vs low-vol)

- Nearby parameter changes (noise test parameter optimization)

- Synthetic data scenarios that mimic plausible alternative histories

- Noise-adjusted data series that perturb the historical price path

The Trading Lens: Taguchi in Build Alpha Language

Build Alpha is not trying to find one pretty backtest. At its best, it is trying to find strategy structures that still behave acceptably when the environment changes. That is much closer to robust parameter design than most traders realize.

| Taguchi Concept | Trading Equivalent |

|---|---|

| Controllable factors | Entry logic, exit logic, stops, timeframe, filters, sizing |

| Noise factors | Regime shifts, vol changes, slippage, date sensitivity, parameter shifts |

| Inner array | Strategy design space — rule combinations being tested |

| Outer array | Stress environment — noise, Monte Carlo, synthetic data, walk-forward segments |

| Signal-to-noise ratio | Mean performance relative to performance variation across noise tests |

| Robust design | Strategy that survives robustness tests |

| Loss function | Drawdown, variance of returns, performance degradation under stress |

Inner Array and Outer Array: A Direct Match

Taguchi’s inner/outer array concept maps cleanly onto trading research.

Inner Array (Strategy Design)

- Entry type and signals

- Exit type and logic

- Stop and target rules

- Timeframe and bar type

- Filter combinations

- Trade direction

- Parameter values

Outer Array (Stress Environment)

- High-vol vs low-vol regimes

- Trend vs chop environments

- Alternate date ranges

- Alternate symbols

- Worse fills and higher slippage

- Synthetic data variants

- Nearby parameter values

- Walk-forward segments

Instead of asking “Which strategy made the most money in one test?” you ask a stronger question: Which strategy still behaves well after repeated exposure to noise? That is the real robustness question.

Signal-to-Noise Ratio and the Robust Trading Mindset

To compare designs, Taguchi introduced a signal-to-noise index so the response could be judged by both its mean and its variation. Traders often do this informally already — they know a strategy is not attractive if the in-sample result is high but nearby tests collapse, or if the strategy swings wildly depending on small assumptions.

Raw net profit is not enough. A strategy with the highest return can still be the weakest candidate if it is highly sensitive to noise. A lower-return strategy with tighter behavior across realistic perturbations can be the much better live-trading choice.

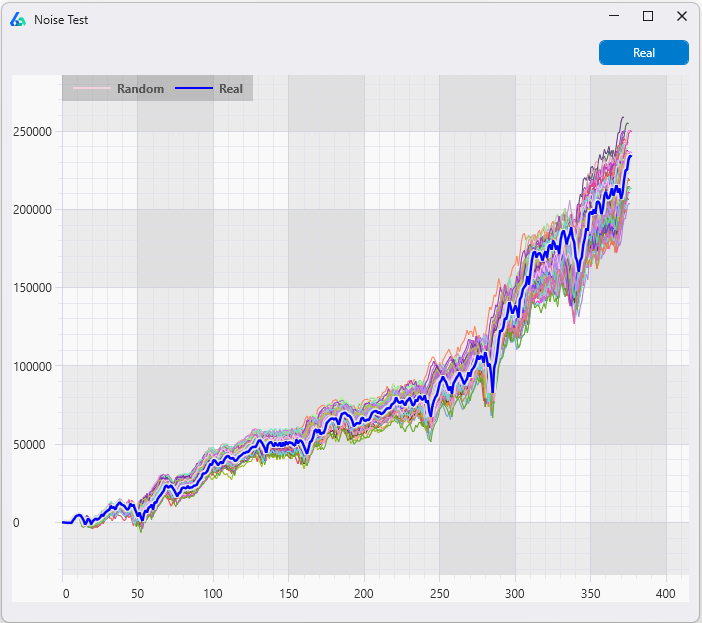

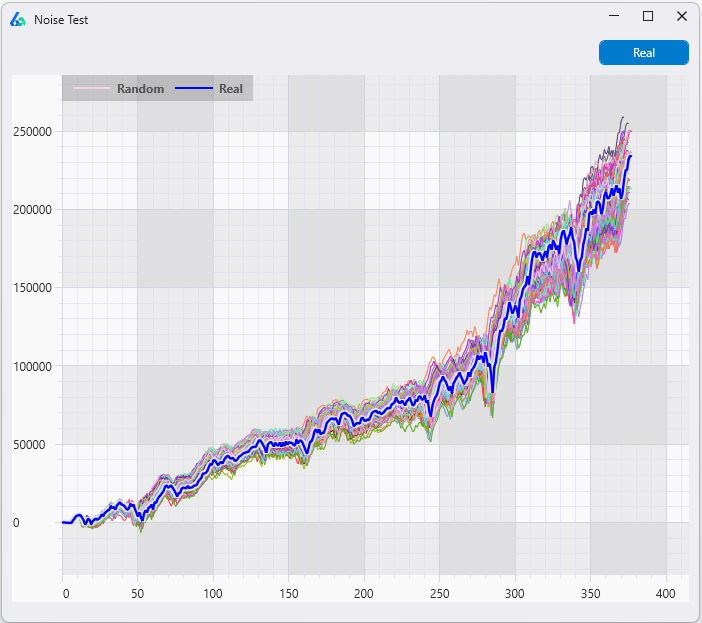

This is why the Noise Test is one of the most valuable tools in Build Alpha. It directly measures signal-to-noise behavior: does the strategy’s equity curve remain tight across 1,000 noise-adjusted data series, or does it scatter widely?

Case Study: Tight vs Wide Noise Test

The Lying Backtests case study demonstrates the Taguchi principle in action. Two strategies with nearly identical backtests are put through the Noise Test — deliberately perturbing the data to see which strategy/design is sensitive to noise.

Both strategies had roughly identical backtests. Only the first survived noise testing. In Taguchi terms: both designs hit the target, but only the first was insensitive to noise. That is the difference between a backtest and a robust design.

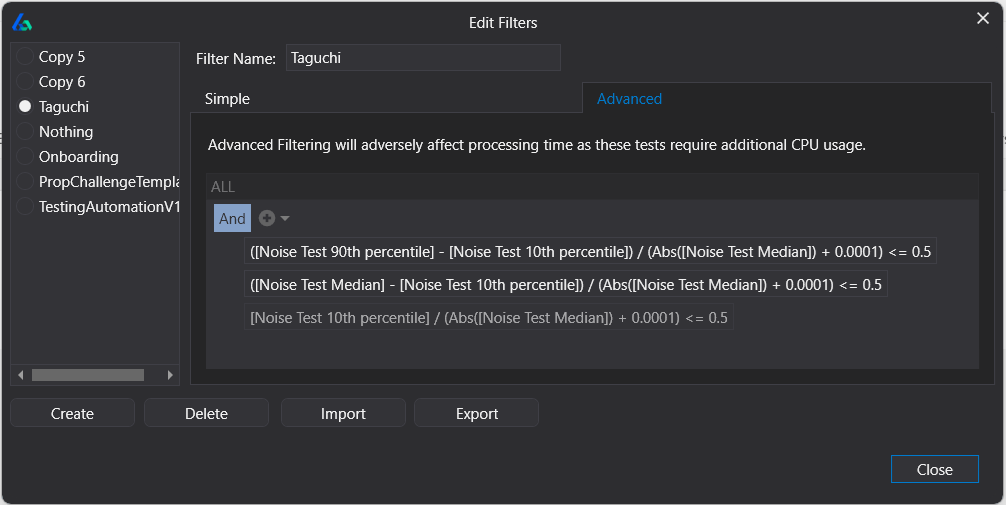

3 Practical Robustness Formulas for Trading

These are modern, trading-friendly formulas inspired by Taguchi’s philosophy: reward decent central performance while penalizing sensitivity to noise. They are not Taguchi’s original formulas — they are adapted for strategy evaluation across noise tests.

1. Normalized Percentile Spread

Measures: How wide the performance distribution is across noise tests relative to the typical result

Interpretation: Lower is better. Higher means more instability.

// A general fragility measure — how scattered are the noise test outcomes? P90 is 90th percentile.

2. Downside Robustness Loss

Measures: How much the weaker scenarios fall below the central case

Interpretation: Lower is better. Focuses on downside — traders care more about how bad things get than how good.

// More useful than full spread because it isolates the left tail

3. Survival Ratio Under Stress

Measures: How much of the median result survives in weak scenarios

Interpretation: Higher is better when median is positive. Spots strategies whose median looks fine but whose lower tail is weak.

// The “what’s left when things go wrong” metric

These thresholds are arbitrary and for demonstration purposes. To find useful thresholds is an exercise left to the trader.

Automated Robustness Workflow

These formulas become most powerful when they are part of an automated pipeline — not a one-off statistic. Build Alpha can generate strategies and only return those that pass robustness thresholds:

The system is no longer optimizing for “best backtest.” It is optimizing for good central performance + acceptable downside + lower sensitivity to noise. That is the Taguchi philosophy made operational.

This workflow connects naturally to Build Alpha’s existing robustness pipeline: noise testing for deliberate disturbance, synthetic data for realistic variation, vs random testing for edge verification, noise test parameter optimization for parameter sensitivity, and walk-forward optimization for temporal robustness. See out-of-sample testing and the full robustness testing guide for the complete methodology.

A Necessary Caution: Taguchi Is Influential, Not Infallible

Taguchi’s methods received some criticism in statistics. All progress does. His use of orthogonal arrays can miss important interaction effects between controllable factors, and some experimental choices have been called simplistic.

That matters in trading because interactions are everywhere. A filter may help only with one exit type. A stop may work on daily bars and fail on intraday. A parameter may look stable only because another hidden interaction is doing the real work. Knowing which strategy types need which tests is another edge.

The right takeaway is not “use Taguchi literally and stop there.” The better takeaway is:

Use Taguchi as a Philosophy

Use Taguchi as a philosophy of robustness — nothing is perfect but understand the foundation. Build Alpha provides 12+ tests designed exactly for this. No single test is sufficient. The full pipeline is what matters.

In summary, do not just look for the strategy with the best backtest. Look for the strategy that still behaves reasonably after noise, variation, and stress are deliberately introduced. That is a much better definition of robustness — and it is much closer to how live markets actually behave. Build Alpha automates this process.

David Bergstrom

David Bergstrom is the founder of Build Alpha. His background is in machine learning at a market-making firm. He has spent over a decade building systematic trading tools used by independent traders, proprietary firms, and hedge funds in 70+ countries.

Frequently Asked Questions

What is the Taguchi Method in trading?

The Taguchi Method is a quality engineering framework for designing systems that are less sensitive to noise and variation. Applied to trading, it means designing strategies that perform well not just in backtests, but under realistic disturbances — regime changes, parameter shifts, slippage variation, and noisy data.

How does robust design apply to algorithmic trading?

Robust design separates controllable factors (entry rules, exit logic, stops) from noise factors (market regimes, volatility shifts, execution quality). The goal is to choose controllable settings so performance is less sensitive to the noise — which is exactly what robustness testing identifies.

What is the signal-to-noise ratio for trading strategies?

In trading, the Taguchi signal-to-noise ratio measures how consistent a strategy’s performance is across noise-adjusted tests relative to its average performance. A strategy with high returns but wide dispersion across noise tests has a low signal-to-noise ratio — it may be overfit.

Does Build Alpha use the Taguchi Method?

Build Alpha applies the same philosophy: generate strategy candidates, expose them to deliberate noise and variation, and only present survivors that maintain acceptable performance under stress. The 12+ robustness tests are the trading equivalent of Taguchi’s outer array.

What is the difference between optimization and robust design?

Optimization finds the settings that maximize performance in one specific test. Robust design finds settings that maintain good performance across many conditions. Understanding this difference between generation and optimization is critical for avoiding overfitting.

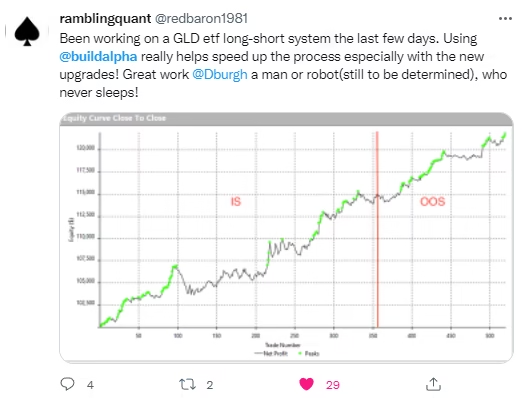

What Traders Say About Build Alpha

Break Your Strategies

Before the Market Does.

12+ robustness tests. Monte Carlo. Noise Test. Walk-Forward. No coding required.