Why Python for Trading?

Python has become the dominant language for quantitative trading research. Its readability, extensive library ecosystem (pandas, NumPy, scikit-learn, ta-lib, statsmodels), and active community make it ideal for data exploration, indicator research, and prototyping trading ideas. Python lets you express complex signal logic in a few lines of readable code, making it the natural first choice for traders moving from discretionary to systematic approaches.

But there’s a critical distinction between using Python for signal research and using Python as a complete trading infrastructure. The former is where Python shines. The latter is where most traders get stuck.

Where Python Alone Becomes a Bottleneck

A full Python trading stack means writing and maintaining your own backtester, handling data alignment and survivorship bias, building robustness tests (Monte Carlo, noise, permutations), creating execution adapters for each broker, managing positions and ticker changes, and handling logs, errors, and edge cases. For many traders, this becomes engineering work instead of trading research — it takes all the enjoyment out of the creative process of signal discovery.

The cost isn’t just time — it’s also reliability. Custom Python backtesters often have subtle look-ahead bias, fill assumption issues, or alignment errors that produce misleading results. And building a single robustness test (let alone a complete validation suite) from scratch is a significant project on its own.

The Hybrid Approach: Python + Build Alpha

Instead of choosing between Python or a no-code platform, you can combine both. Use Python to define your custom signal — a proprietary indicator, regime filter, statistical condition, or ML model — and use Build Alpha to handle strategy generation, robustness testing, and deployment. This gives you full control over signal logic, creative flexibility to express any idea, no need to build or maintain infrastructure, systematic validation instead of one-off backtests, and a powerful C++ simulation engine.

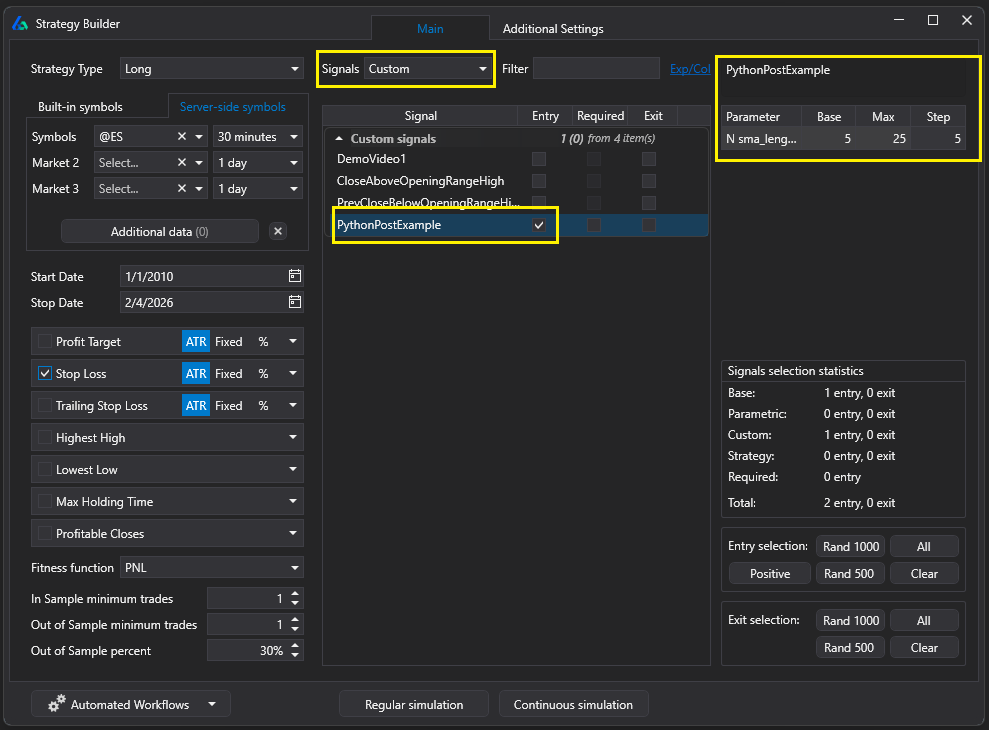

From Build Alpha’s perspective, your Python signal becomes just another signal alongside the 7,000+ built-in signals. It can be combined with other conditions, used as an entry, exit, or filter, tested across different markets and timeframes, and optimized — all through Build Alpha’s point-and-click interface.

How Custom Python Signals Work Inside Build Alpha

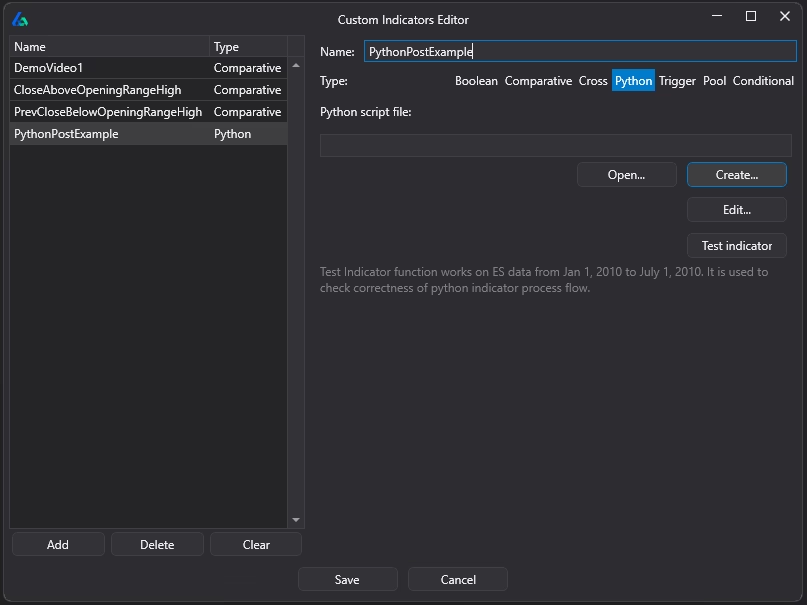

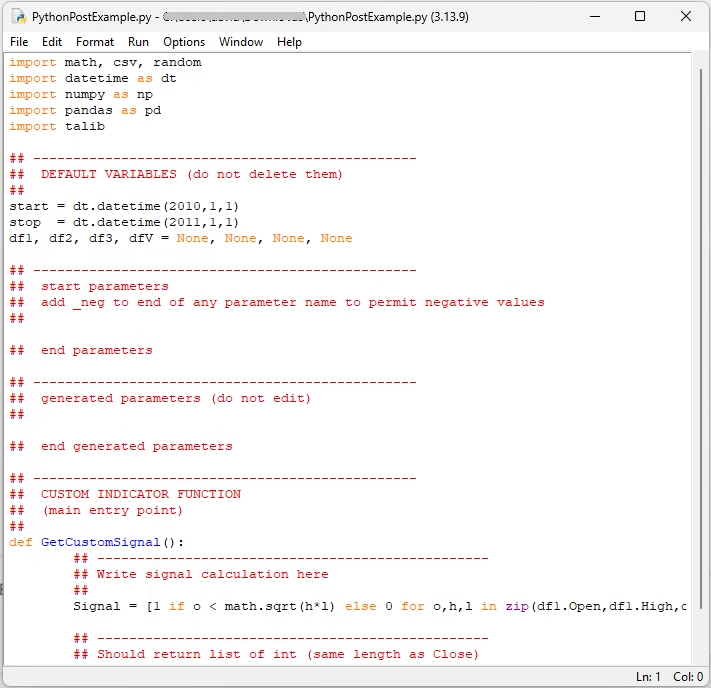

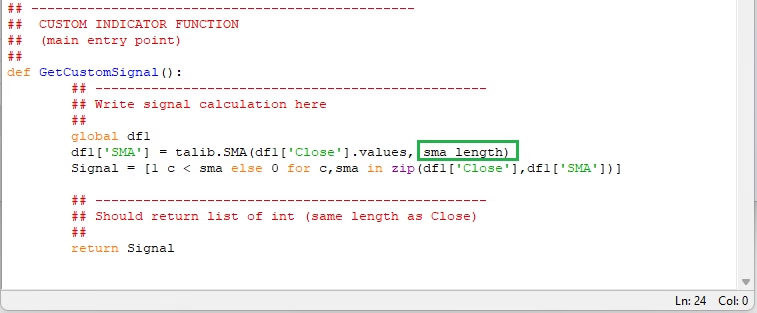

Creating a custom Python signal in Build Alpha follows a straightforward process. Go to File → Custom Signals Editor, create a new Python signal, and Build Alpha opens a template with pandas, ta-lib, scikit-learn, and other popular libraries pre-installed. You can always add additional libraries via pip. Write your signal logic — anything that outputs a time-aligned series (boolean or numeric) — and it integrates seamlessly into the generation engine.

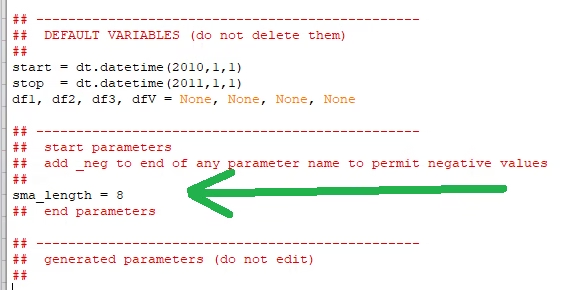

To allow Build Alpha to optimize your custom parameters, add them in the designated template section. The genetic algorithm will explore your parameter ranges alongside all other strategy components. For a complete walkthrough, see Using Python in Build Alpha. For an introduction to creating the same signal in Excel, Python, and Build Alpha, see Same Signal in Excel, Python, Build Alpha.

What Makes the Best Python Trading Strategy Builder?

Many tools can combine trading rules into code. The best Python trading strategy builder goes further — it must also answer the question every systematic trader needs answered: is this backtest real, or is it curve-fit noise?

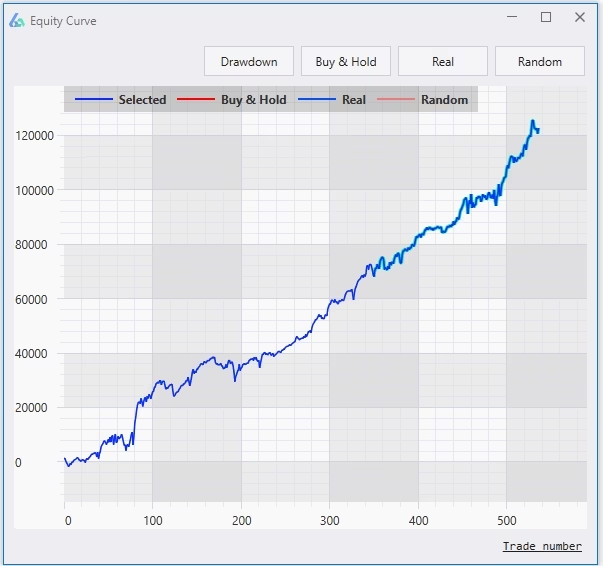

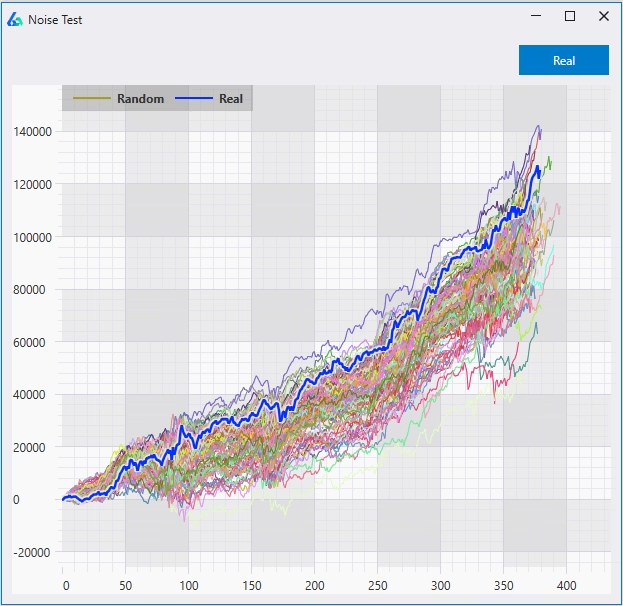

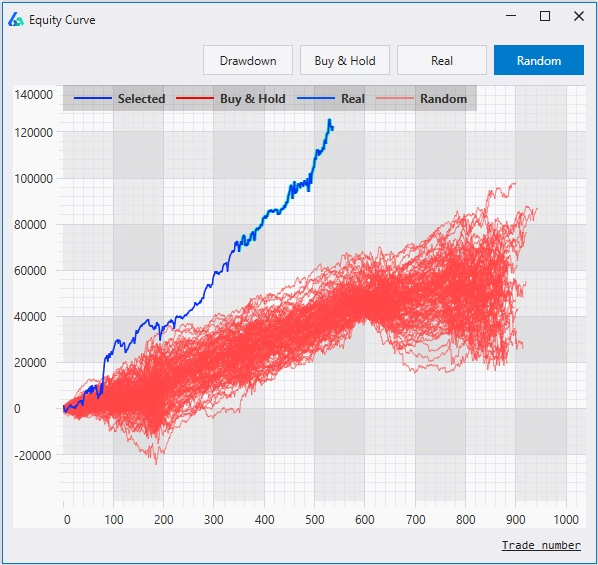

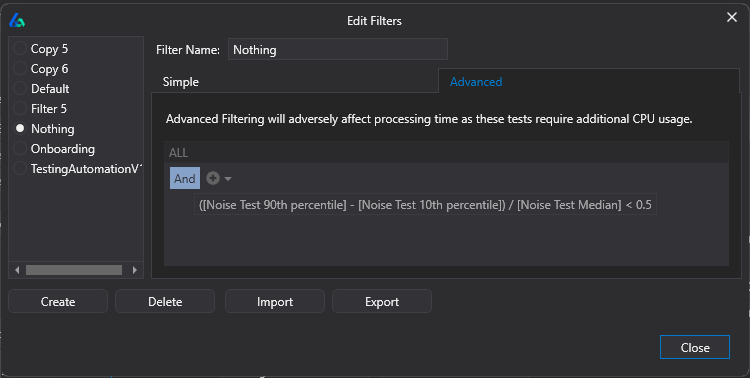

Here’s what separates a credible strategy builder from a backtest factory. First, the signal library matters — Build Alpha’s 7,000+ built-in signals plus your custom Python signals create genuine combinatorial diversity. Second, the search engine matters — Build Alpha’s genetic algorithm with ML overlay is more efficient than brute-force grid search and less prone to overfitting. Third — and most importantly — validation must be built into the workflow, not bolted on afterward. Build Alpha’s automated filter workflows ensure that only strategies passing out-of-sample testing, Monte Carlo analysis, Noise Tests, and Vs Random benchmarking are ever promoted for export.

Genetic Algorithm + Python Signal Optimization

Build Alpha’s backend uses a genetic algorithm with a machine learning overlay to efficiently explore the vast space of possible strategy combinations — including your custom Python signal parameters. You define the search constraints and the engine systematically generates, evaluates, and evolves candidates. Instead of manually looping through variations in slower Python code, you define constraints and let Build Alpha’s C++ engine do the work.

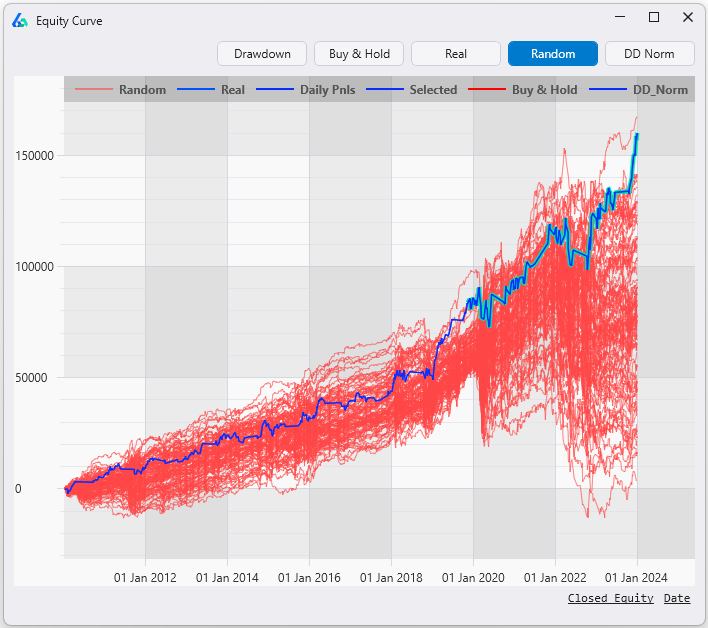

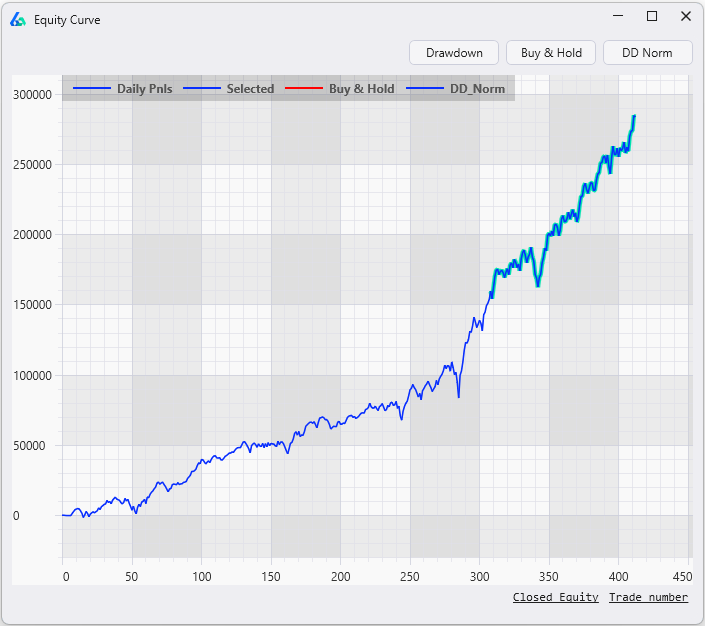

The genetic algorithm produces a large candidate set of diverse strategies — not just a single “best” backtest — giving you the ability to compare, filter, and validate across multiple approaches. Your custom Python parameters are optimized alongside entry conditions, exit rules, filters, and risk management in a single integrated workflow.

Robustness Testing Without Writing More Code

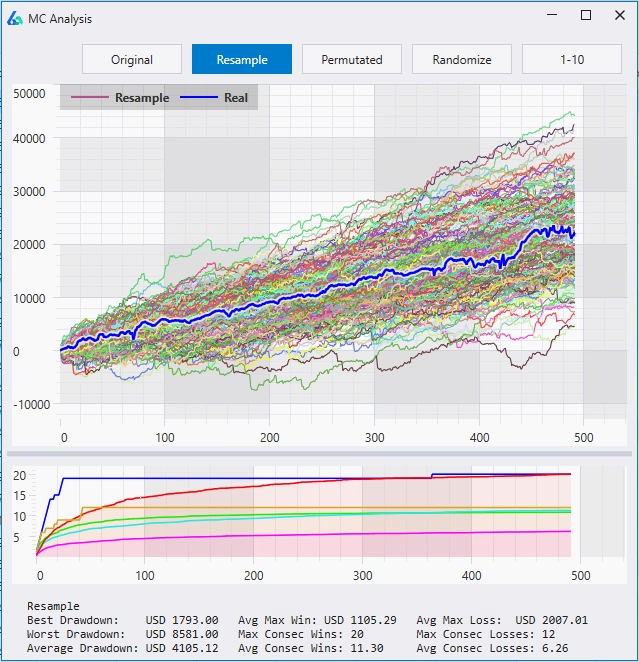

This is where many Python-only workflows break down. Robustness testing is about evaluating whether a strategy is likely to survive across alternate market conditions — not just the historical path it was trained on. Generating multiple alternate “realities” via techniques like noise tests, Monte Carlo resampling, or parameter perturbations and re-trading a strategy across them is computationally expensive and time-consuming to build and maintain in pure Python.

Build Alpha includes all of these tests built-in, plus out-of-sample validation, Walk Forward optimization, Vs Random benchmarking, and testing on synthetic data. All without writing additional Python infrastructure. Read here for more on Robustness Testing.

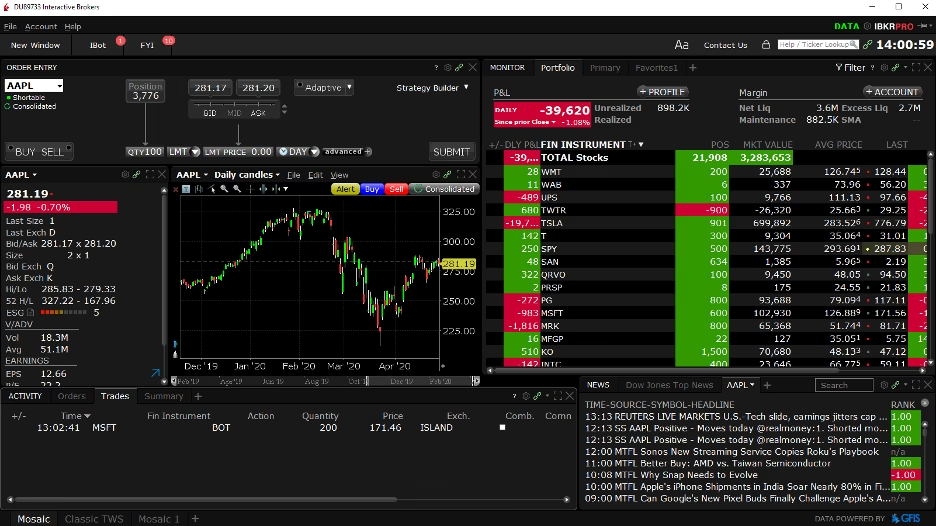

Exporting to Interactive Brokers & Other Platforms

Once a strategy passes your validation rules, Build Alpha generates Python code for Interactive Brokers at the click of a button. The generated code can run on an IB simulated account or live trading account. Once running, you can view orders inside Interactive Brokers’ Trader Workstation (TWS), monitor positions, and manage risk from a centralized interface.

Build Alpha also generates code for TradeStation (EasyLanguage), MetaTrader 4/5 (MQL), MultiCharts (PowerLanguage), TradingView (Pine Script), NinjaTrader 8 (NinjaScript), and ProRealTime (ProBuilder) — so your research is never locked to a single platform.

Alternative Data & Non-Price Signals

Build Alpha expands the research universe beyond what most Python traders typically access with alternative data signals including market breadth and internals, economic data and news events, Treasury yields and spreads, VIX term structure, weather data, Google Trends, COT report positioning, gamma exposure (GEX), dark pool index (DIX), and custom data imports via CSV/TXT.

These non-price signals give context to your custom Python indicators and the 7,000+ built-in signals. Build Alpha can connect directly to multiple broker data feeds for historical and live data, reducing the data wrangling overhead that consumes so much time in a pure Python workflow. All alternative signals can be traded live — not just used for research.

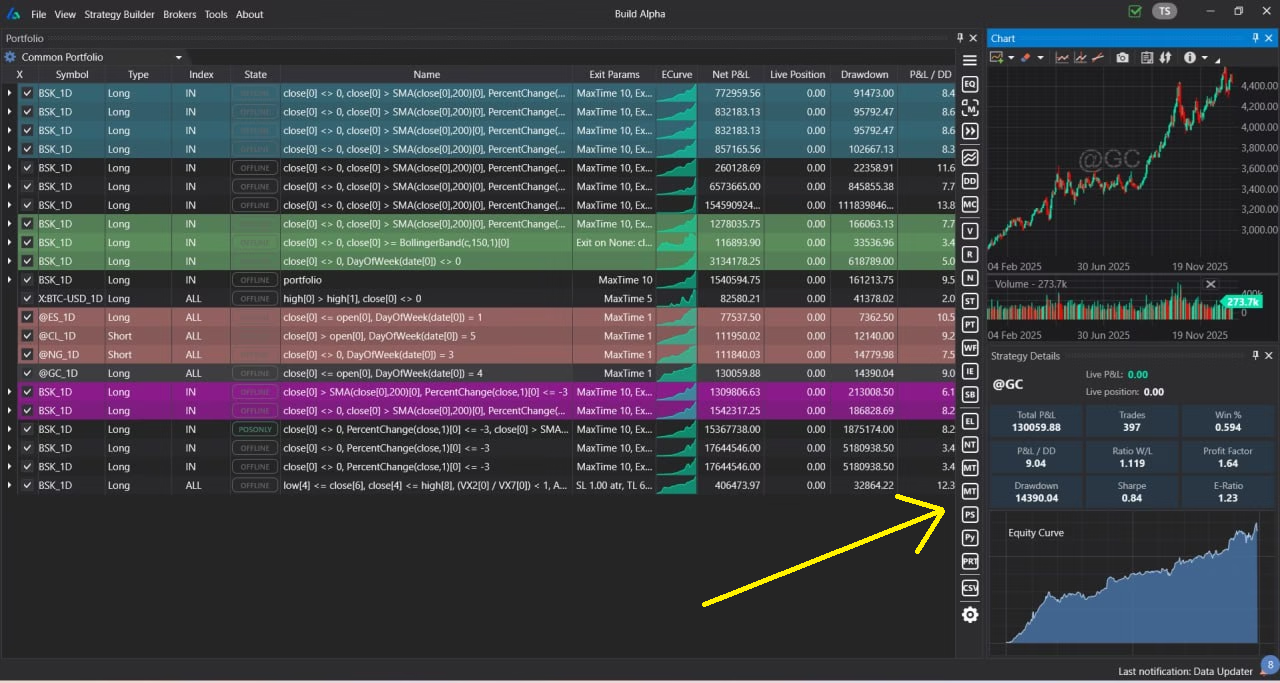

Portfolio Strategy Management

Single strategies are fragile. Portfolios of uncorrelated strategies are antifragile. Build Alpha’s portfolio mode lets you combine multiple validated strategies into a single simulation using pooled (shared) capital, analyze correlation matrices, and optimize allocations across asset classes and timeframes. Each strategy can be exported independently — as Python for IB, EasyLanguage, MQL, or any other supported format — giving you a modular, scalable approach to systematic trading.

Build Alpha also connects to live data feeds for strategy monitoring. Track real-time profit and loss, receive position change alerts, and monitor strategy health against Monte Carlo projection bands — all from a centralized dashboard. Read more: How to automate trading with no coding.