Opening Range Breakout

Strategy: Complete Guide

The Opening Range Breakout (ORB) is one of the most studied intraday strategies in systematic trading. This guide covers the rules, 4 trade setups, common mistakes, validation methods, and how to build ORB systems that survive real markets.

Table of Contents

- What Is an Opening Range Breakout?

- How the ORB Strategy Works

- Why Opening Range Breakouts Work

- 4 ORB Trade Setups

- 5-Minute ORB Walkthrough

- Opening Range Trading Strategies

- Trade Management: Exits, Limits, and Filters

- Key ORB Variations

- Common ORB Mistakes

- How to Validate an ORB Strategy

- Why Most ORB Strategies Fail

- How Build Alpha Improves ORB Development

- Advanced ORB Optimization

- FAQ

What Is an Opening Range Breakout Strategy?

An Opening Range Breakout (ORB) strategy is a trading method that uses the high and low of a defined early session period — typically the first 5 to 60 minutes — to identify breakout opportunities. Traders enter positions when price breaks above or below this range, aiming to capture directional momentum established at the market open.

The Opening Range High (ORH) and Opening Range Low (ORL) become the key levels for the rest of the session. These levels act as support, resistance, entry triggers, stop placement, and profit targets — all defined by a single early-session observation.

Opening Range Breakout: Quick Summary

- → Define the high and low of the first N minutes of the session (the “opening range”)

- → Buy when price breaks above ORH, short when it breaks below ORL

- → One of the most studied intraday strategies — simple rules, many variations

- → Most ORB strategies fail due to overfitting — robustness testing is essential

How the Opening Range Breakout Strategy Works

The opening range defines two critical levels for the session:

- Opening Range High (ORH): The highest price during the first N minutes — breakout trigger for longs

- Opening Range Low (ORL): The lowest price during the first N minutes — breakout trigger for shorts

Why Opening Range Breakouts Work

Opening range breakouts are based on structural market behavior, not just pattern recognition:

Institutional Order Flow

Large institutional orders cluster at the open as funds execute overnight decisions. This creates directional pressure that, once established, tends to persist.

Volatility Expansion

Volatility is highest in the first hour of trading. The opening range captures this compression — and breakouts release the stored energy.

Price Discovery

The open is where overnight positioning meets new information. The opening range represents the market’s first consensus — a break from that consensus signals new directional conviction.

Liquidity Concentration

Volume is highest near the open. Breakouts that occur on high liquidity are more meaningful than those on thin volume later in the session.

4 Opening Range Breakout Trade Setups

The basic ORB is just the beginning. Professional traders use Opening Range in many ways. Here are four distinct setups based on how price interacts with the opening range levels.

Setup 1: Clean Breakout Above ORH

The classic setup. Price breaks above the Opening Range High and continues higher. This is the simplest ORB trade — enter on the break, stop below ORH (or at ORL), and ride the move. Exit EOD or end of session.

Setup 2: Fade the False Breakout

Price breaks above ORH but quickly reverses back below it — a failed breakout. Instead of chasing the break, this setup fades it: short when price falls back inside the range after the false break above. Trapped longs create selling pressure on the reversal.

Setup 3: Retest and Limit Entry

Price breaks above ORH, runs higher, then pulls back to retest ORH as support. This is the highest-probability ORB setup because it confirms the breakout level as new support before entering via limit order at ORH.

Setup 4: Enter at Opposite Range Support

Price is range bound or stuck inside the Opening Range. Price pulls back all the way down to ORL, which now acts as support. This setup buys at ORL and the stop goes below ORL, and the target is back toward ORH or higher.

5-Minute Opening Range Breakout: Video Walkthrough

Watch a 5-minute opening range breakout strategy being built, tested, and validated inside Build Alpha — from signal selection through robustness testing to code export:

Opening Range Trading Strategies

Watch a 30-minute opening range breakout strategy video going over five different applications of trading around the opening range. Then watch Build Alpha improve opening range strategies in minutes — no code strategy discovery:

Trade Management: Exits, Limits, and Filters

ORB strategies require strict trade management rules. The entry is only half the system — exits, trade limits, and filters often determine whether the strategy survives live trading.

Exit at the Opposite Range Level

A popular exit approach is to use the opposite end of the opening range as a stop loss. If you’re buying above ORH, set your exit at ORL — or at the midpoint of the opening range. This works well because the opening range levels act as natural support and resistance throughout the session. The midpoint exit is more conservative but you may stop out prematurely – everything is a trade off and should be tested!

Limit Trades Per Day

Most ORB strategies should limit the number of entries per session — typically one or two. Without this limit, false breakouts can trigger multiple losing entries on choppy days. Build Alpha allows you to set a maximum number of trades per day as part of the strategy rules in the Additional Settings menu.

Force End-of-Day Exit

Intraday strategies should close all positions before the session ends. Holding ORB trades overnight introduces gap risk that the strategy was never designed to handle. Set a forced exit at a specific time (e.g., 15 minutes before close) or at the session end to keep the strategy purely intraday.

Opening Range Size Filters

Not every opening range is worth trading. For example, if the range is too wide then the breakout entry is far from your stop — creating poor risk/reward. If the range is too narrow, the breakout is more likely to be noise. A popular approach is to measure OR / ATR — the opening range width relative to the average true range. This normalizes the range size by recent volatility and helps you restrict trading to sessions where the opening range is large enough to warrant a short-term trade or calm enough for a stable system to operate. Different OR / ATR measures may call for a different opening range trading style.

Key ORB Variations

| Variation | Description | Best For |

|---|---|---|

| 5-Minute ORB | Fast, tight range, more signals, more noise | Scalpers, liquid futures |

| 30-Minute ORB | Balanced range, most studied window | General intraday trading |

| 60-Minute ORB | Wide range, fewer signals, more stable. The first 60 minutes is sometimes referred to as the “Initial Balance” (IB) in market profile terminology. | Swing-oriented intraday |

| Volatility-Filtered | Only trade when ATR exceeds threshold | Avoiding low-vol chop days |

| Gap-Based ORB | Only trade when market gaps up/down | Capturing directional bias |

| Volume-Confirmed | Require breakout volume spike | Filtering false breakouts |

Common Mistakes in ORB Trading

Overfitting the Time Window

Testing dozens of opening windows (5, 7, 10, 12, 15, 20, 25, 30 minutes…) guarantees you’ll find one that looks great on historical data. This is parameter mining, and the “best” window will likely fail going forward.

Ignoring Market Regime

ORB works differently in trending markets vs mean-reverting markets. A strategy optimized on trending data will struggle when the market chops — and vice versa. Regime awareness is critical.

No Robustness Testing

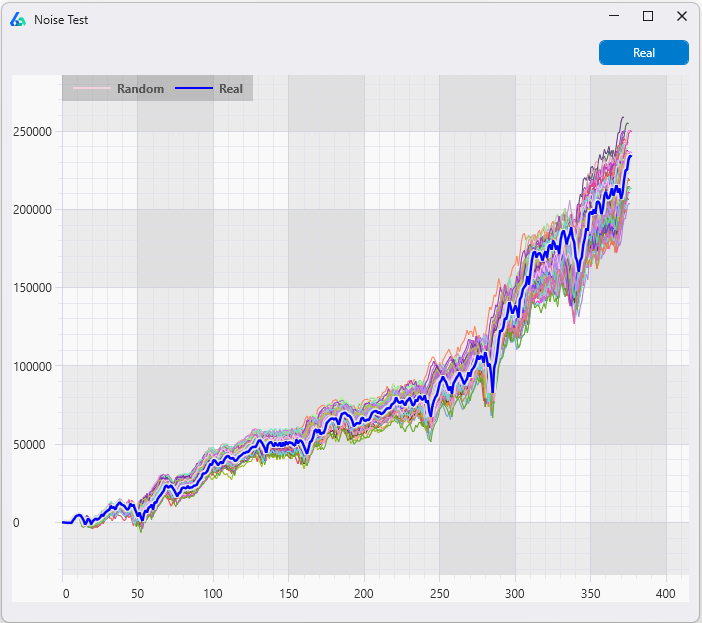

A single backtest is never enough. Without Monte Carlo simulation, noise testing, and out-of-sample validation, you risk trading randomness.

No Trade Limits

Taking every breakout signal without limiting trades per day turns a strategy into a noise-chasing machine on choppy sessions. One or two trades per day maximum.

How to Validate an ORB Strategy

To ensure an ORB strategy is robust and not just a product of curve fitting, it must pass multiple validation tests:

Sample

Forward

Carlo

Test

Benchmark

Out-of-sample testing confirms performance on unseen data. Walk-forward analysis tests stability across rolling windows. Monte Carlo simulation estimates the range of possible outcomes. Noise testing checks if the edge survives small data changes. And vs random benchmarking ensures your ORB strategy beats what random entries could achieve. See the full robustness testing guide.

Why Most ORB Strategies Fail

Testing thousands of ORB variations guarantees some will appear profitable by chance. If you test 20 time windows × 10 stop types × 10 targets, you’ve created 2,000 combinations. Statistically, some will look strong — even with no real edge.

This is the fundamental curve-fitting trap in ORB development. The strategy search space is large enough that luck alone produces impressive backtests. Understanding the difference between strategy generation and optimization is critical: you want to discover robust ORB systems, not overfit parameters to historical noise.

The Lying Backtests case study demonstrates exactly this problem — two strategies with identical backtests, only one survives forward testing.

How Build Alpha Improves ORB Development

Instead of manually testing ORB variations one at a time, Build Alpha automates the entire research workflow:

- Generates thousands of ORB strategy variations automatically using genetic algorithms

- Tests multiple opening range definitions, entry types, and exit logic

- Evaluates candidates with fitness functions

- Can apply 12+ robustness tests automatically on every candidate

- Exports validated strategies to TradeStation, NinjaTrader, TradingView, and more

This transforms ORB development from a manual idea → into a statistically validated system. Every discovered strategy is original and proprietary to you. See examples of generated strategies or learn about the full strategy generation framework.

Advanced ORB Optimization

David Bergstrom

David Bergstrom is the founder of Build Alpha. His background is in machine learning at a market-making firm. He has spent over a decade building systematic trading tools used by independent traders, proprietary firms, and hedge funds in 70+ countries.

Frequently Asked Questions

What is the best time frame for an Opening Range Breakout?

The 30-minute opening range is most common, but optimal settings depend on the market and must be validated with robustness testing. Testing dozens of windows without validation leads to overfitting.

Does the Opening Range Breakout work in all markets?

No. ORB works best in volatile, trending environments — particularly equity index futures and liquid stocks. It may underperform in range-bound or low-volatility markets. Regime filters help.

How do you avoid false breakouts in ORB trading?

Use filters: volume confirmation, volatility thresholds, trend direction. Consider the retest entry (Setup 3) which waits for the breakout level to hold as support. And validate with noise testing and vs random benchmarking.

Is the Opening Range Breakout still profitable today?

It can be — but only when properly validated, not overfit, and used within a diversified portfolio. The edge is not in the ORB idea itself — it’s in how rigorously you test and validate it.

What is the difference between a clean breakout and a retest entry?

A clean breakout enters immediately when price breaks ORH. A retest entry waits for price to break ORH, pull back to ORH, and confirm it as support before entering via limit order. The retest setup has higher probability but fewer signals.

Should I hold ORB trades overnight?

No. ORB is an intraday strategy — force-close all positions before the session ends. Overnight holds introduce gap risk the strategy was never designed for. Set a forced exit at a specific time (e.g., 15 minutes before close).

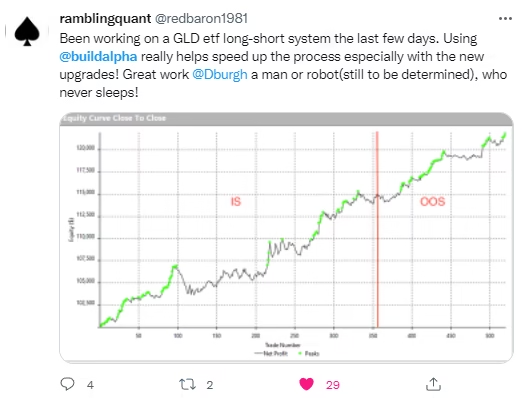

What Traders Say About Build Alpha

Explore More

Ready to Start Algo Trading?

Build Alpha generates, validates, and exports algorithmic trading strategies automatically. 7,000+ signals. 12+ robustness tests. No coding required.