Build Strategies Across the Multiverse of Price Paths

The historical data is one path. The future is another. Train your strategies across hundreds of synthetic price series — noise-adjusted, Monte Carlo permutated, and Vs Shifted — so they survive whatever comes next.

All system traders aim to build more robust strategies and bullet-proof their portfolios. But most traders are stuck training on the historical data that every other participant has. We do not want strategies reliant on one market environment persisting forever — that simply is not the way things are.

A robust strategy can withstand changes to the market and continue to perform. It is not dependent on things remaining the same. Our goal: find strategies that handle varying amounts of noise, volatility, sequences of prices, or even price shocks. One way to better do that is by introducing synthetic data to the building process.

Multi-Path vs. Single Path

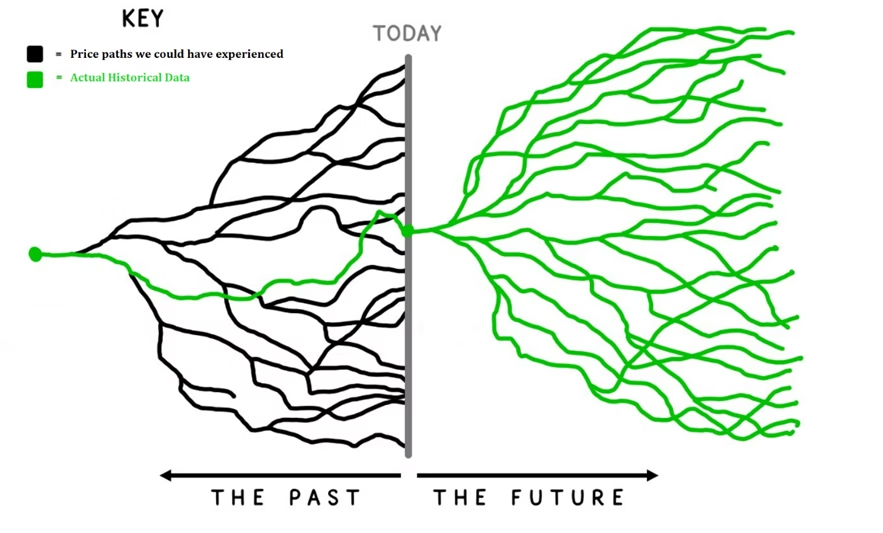

For decades, system traders have developed strategies on only historical price data. But historical data represents a single path of what actually happened (green below), while various paths were possible (black below) and can exist going forward.

The green line is what happened. The black lines are what could have happened — why train on only one?

Instead of building strategies on a single path, why not build strategies on the many paths that could have happened? A favorite trading quote: “do not develop for the knowable past but rather for the probable future.”

🌐 Alternate Realities

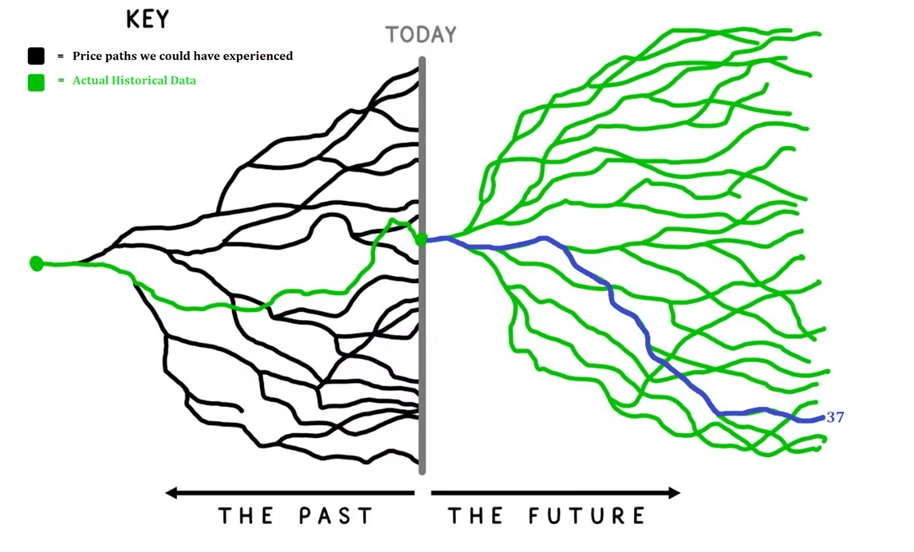

Think of these paths as parallel universes. In our universe, prices behaved how they behaved. But alternate realities could have existed and their prices may have played out differently. Furthermore, we may soon jump to one of these realities. What if the future takes path #37 but you only trained on the single historical green line?

Path #37 highlighted — training on alternate realities prepares your strategy for the unknown future

REAL

🌍

Our Universe

The actual historical path. All-time highs at the known dates.

🪐

Universe #2

Noise-adjusted. Earlier ATH, different volatility clusters.

🌀

Universe #3

MC permutated. Same endpoint, entirely different path.

✨

Universe #4

Vs Shifted. Same market, different bar boundaries.

By creating strategies across multiple data series, we aim to capture the underlying signal rather than the noise (randomness) in any one specific universe.

Pre-Simulation vs. Post-Simulation

Build Alpha has always enabled traders to use synthetic data to test strategies from a robustness testing standpoint (post-simulation). Now you can include this data before the simulation engine or genetic algorithm begins — for the strategy discovery process itself.

Post-Simulation (Traditional)

Test After Building

Build strategy on historical data first, then validate by re-trading on synthetic series.

Add synthetic series to the genetic algorithm. Strategies trained across all paths simultaneously.

Discovery accounts for alternate realities

Rules must work across the multiverse

Fundamentally more robust from the start

Both approaches have value, and using them together is ideal. Build on synthetic data first, then validate survivors with post-simulation Noise Test, Monte Carlo, and out-of-sample testing.

Synthetic Data Methods

How can we create synthetic data? Below are the methods Build Alpha supports, ranging from simple to advanced. Building strategies on a variety of methods diversifies away pitfalls from relying on any single generation approach.

⏱️

Vs Shifted Data

Shifts bar open/close times by 1, 2, 3+ minutes — creating data with the same characteristics but different OHLCV values, patterns, highs/lows, and indicator calculations.

Method: shift bar boundaries ±N min

Control: shift amount, any timeframe

Result: same market, different bars

📊

Noise-Adjusted Data

Randomly adds or subtracts volatility (as a % of ATR) to each bar, creating thousands of new synthetic price series. Helps avoid fitting to the specific noise of one data set.

Method: ±% of ATR → O, H, L, C

Control: bars affected + magnitude

Result: same structure, different noise

🔀

Monte Carlo Permutation

From Timothy Masters’ book — reshuffles the log of inter and intrabar price changes then exponentiates back into raw OHLC. Retains statistical properties but destroys patterns.

Method: shuffle log price increments

Control: permutation parameters

Result: same distribution, new path

Vs Shifted in Detail

Standard 15-minute data creates bars at 0:00, 0:15, 0:30, 0:45. But what if we shifted to 9:03–9:18, 9:18–9:33, etc.? Or 9:06–9:21? Each shift creates a new data series with the same characteristics but different OHLCV values. Patterns are the same but the specifics are not:

Original data vs. Vs Shifted — same patterns, different OHLCV values

Animated: each frame shows a different noise-adjusted version of the same data

Monte Carlo Permutation in Detail

From Timothy Masters’ Permutation and Randomization Tests for Trading System Development — the MCP method reshuffles log inter and intrabar price changes, then exponentiates them back into raw OHLC prices. The result: data with the same statistical fingerprint but completely different price paths.

Three MCP-generated OHLC data sets — same date range, drastically different price paths

You can read more about this test and other Monte Carlo methods in the complete Monte Carlo Simulation Guide which includes a free simulator.

Advanced Machine Learning (GANs & Deep Learning)

Many machine learning methods lend themselves to generating synthetic data. Generative Adversarial Networks (GANs) and deep learning approaches can learn the distribution of historical price data and generate entirely new series that exhibit similar statistical properties — regime clustering, fat tails, volatility persistence — without being a transformation of the original data. These are frontier methods that go beyond simple permutation or noise injection.

🧠 GANs for Synthetic Data

GANs train two neural networks against each other: one generates synthetic data, the other tries to distinguish it from real data. The result is synthetic price data that is statistically indistinguishable from actual market data — a powerful way to expand your training set beyond simple transformations of the historical path.

Custom Data Import

Build Alpha also supports custom data imports — if you have an alternative generative method (your own GAN, deep learning model, or any other approach), you can add your own synthetic data to the build process via CSV or TXT file.

Why Not Just Use Other Markets?

You can! Building strategies on other markets is another great idea, discussed in Testing Across Markets and Trigger Signals. However, other markets often have different players, point values, volatility ranges, and hedging use cases. Despite heavy correlations, the underlying pattern may not exist across markets — resulting in an insufficient test.

The best approach combines all available methods in your portfolio construction:

A single market

A single market plus related markets

A single market plus unrelated markets

A single market plus synthetic data

A single market plus related markets plus synthetic data

There is no single best approach. We constantly aim to equip ourselves with robust strategies built on different methods to best handle changing markets.

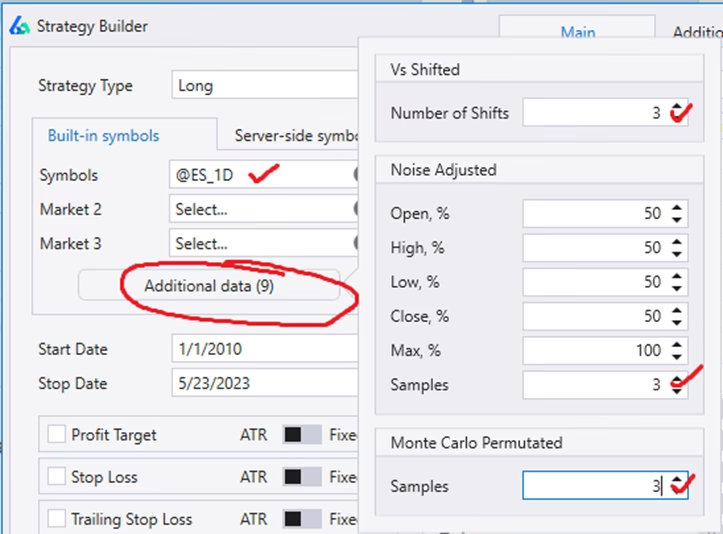

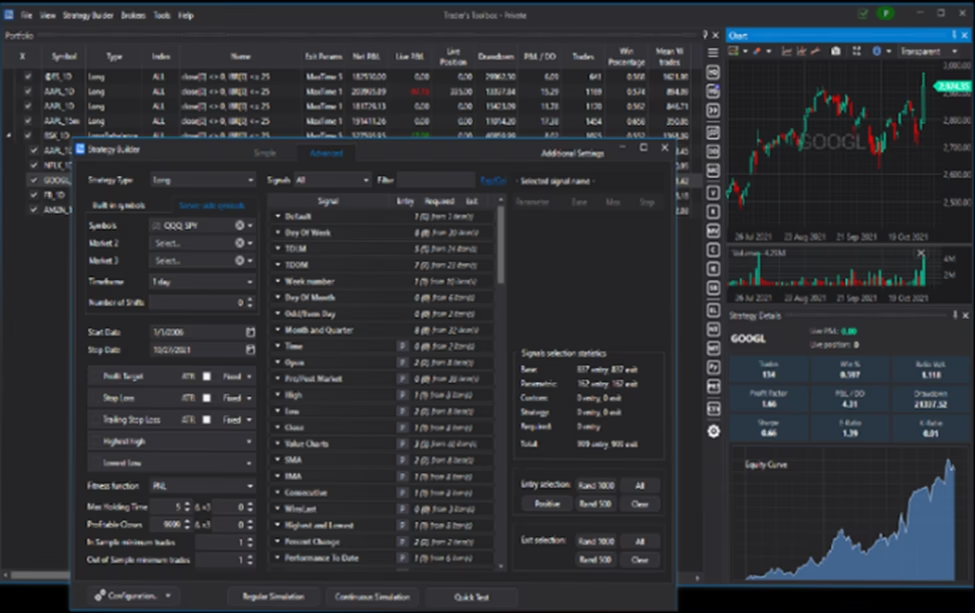

Setting Up Synthetic Data in Build Alpha

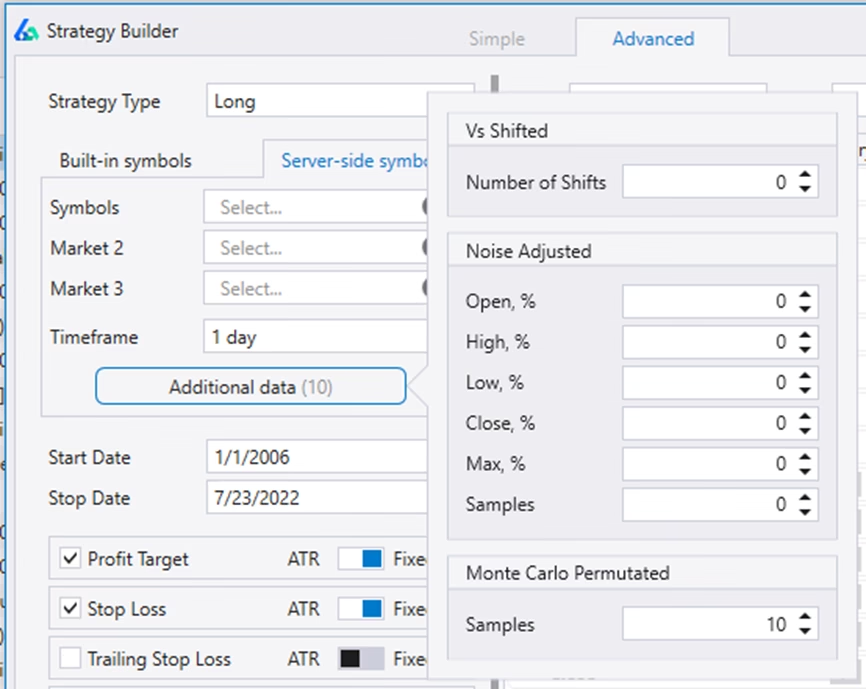

After selecting the market you want to trade (can be multiple markets), hit the Additional Data button to create as many synthetic data series as needed. Below shows SP500 Emini Futures with 9 additional data series — three from each method: Vs Shifted, Noise Adjusted, and Monte Carlo Permutation.

Setup: 9 synthetic series (3 per method) added to @ES Emini futures

📝 Note on Multi-Symbol

If you select multiple symbols (e.g. @ES and @GC), the above configuration creates 18 synthetic data series — 9 for each symbol. The synthetic data scales with your symbol universe automatically.

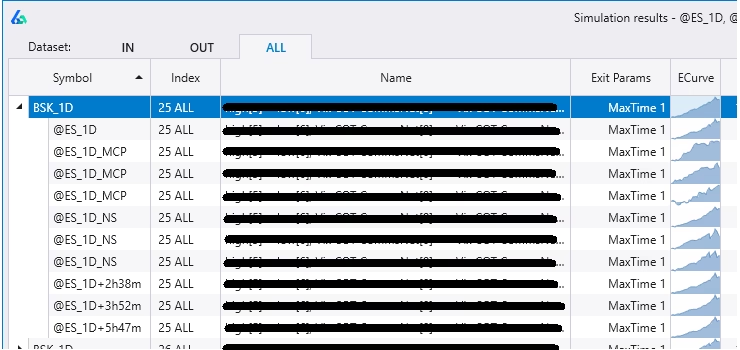

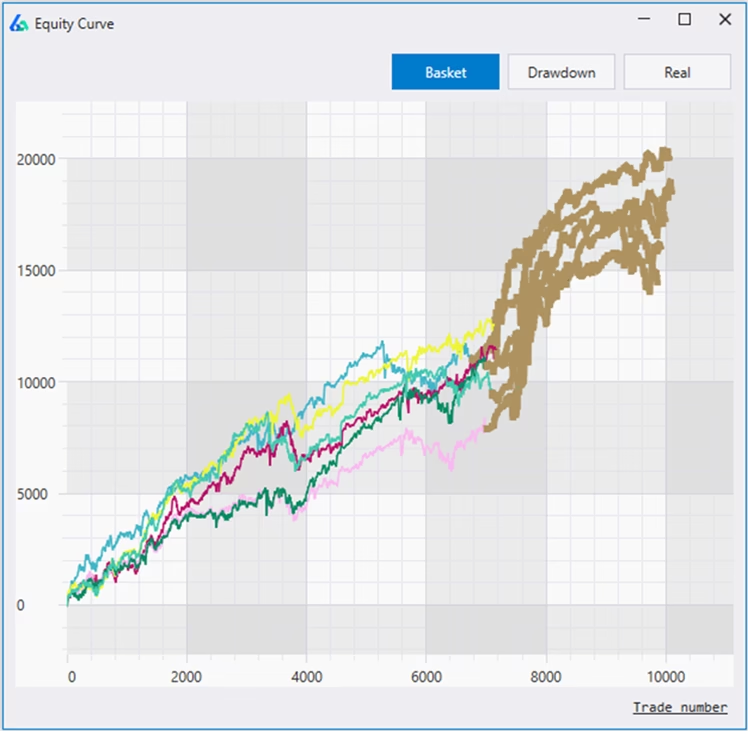

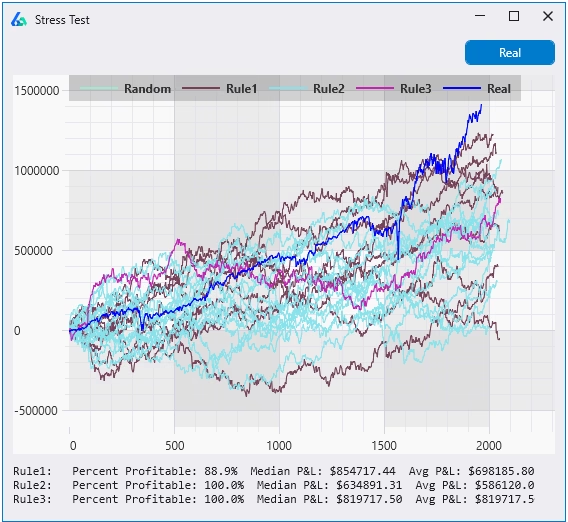

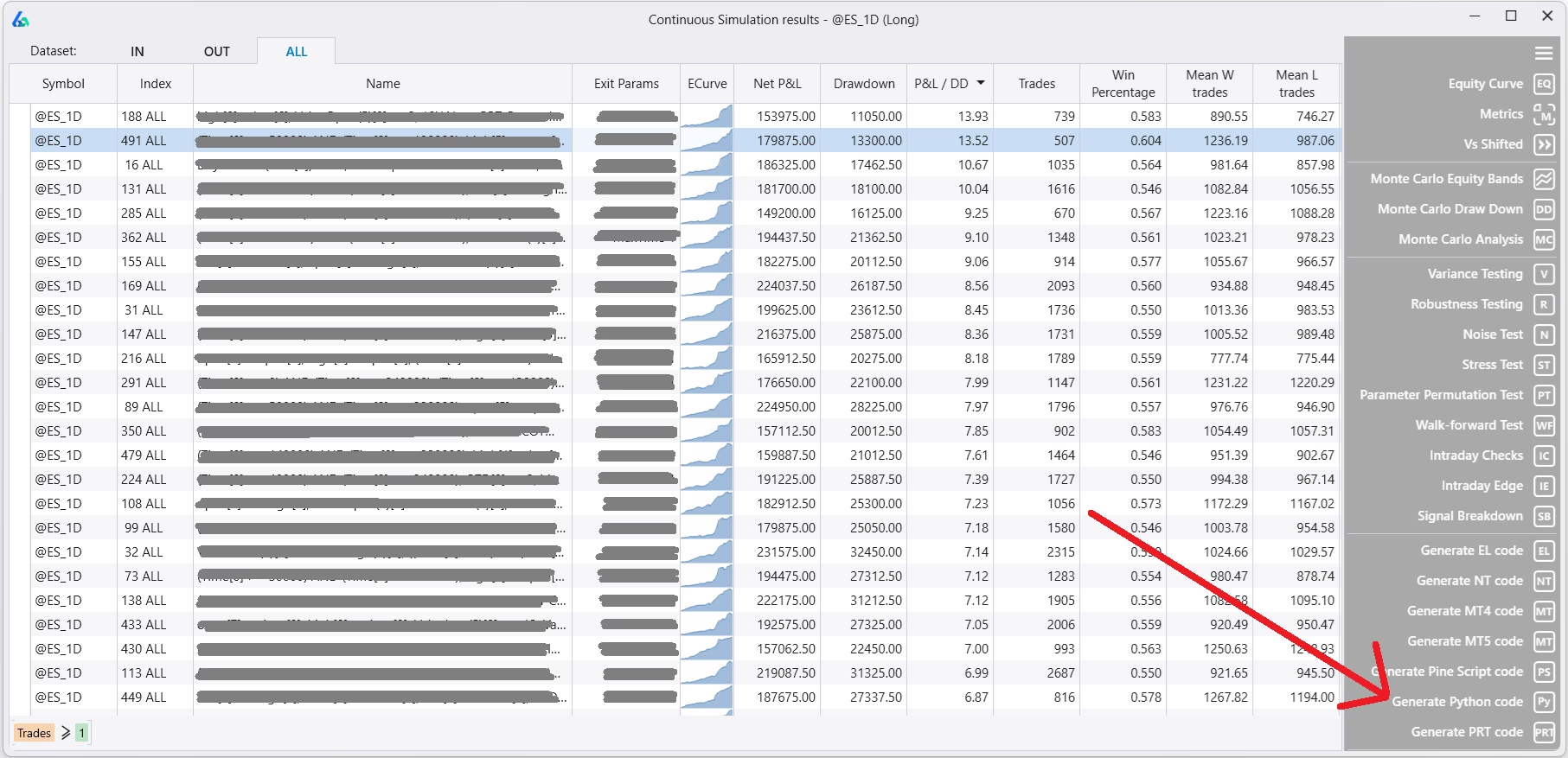

Basket (BSK) Results

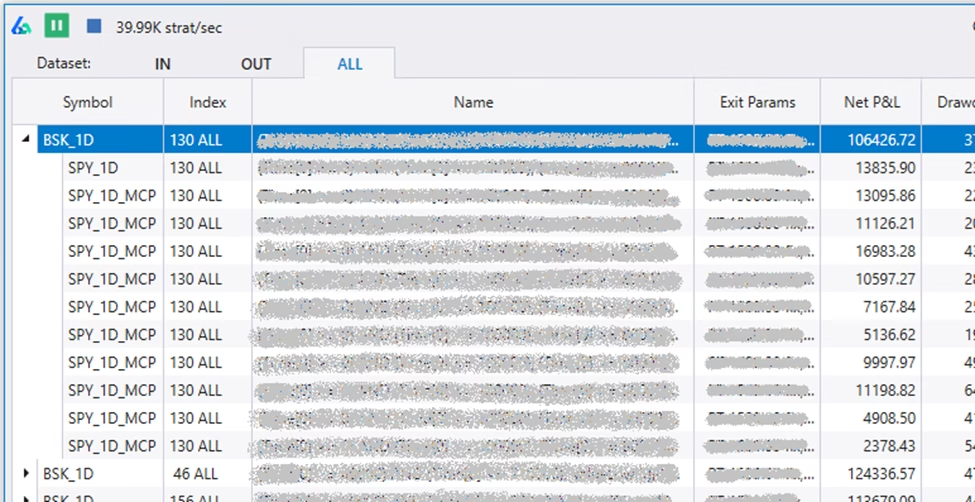

After simulating with added synthetic data, Build Alpha’s results window shows ‘BSK’ results — the strategies that performed best across the entire basket. Expand the BSK row to view how the strategy did on each individual data series:

BSK results: expand to see each synthetic series. Suffixes: _NS = Noise Sample, _MCP = Monte Carlo Permutation, +hhmm = Vs Shifted

Basket Equity Curve Graph

Alternatively, view the equity curve and hit the ‘Basket’ button to overlay the selected strategy’s performance on each synthetic series. Each generation method has its own color:

Orange = Vs Shifted

Blue = Noise Adjusted

Purple = Monte Carlo Permutation

Basket view: each color represents a different generation method — all curves profitable = robust

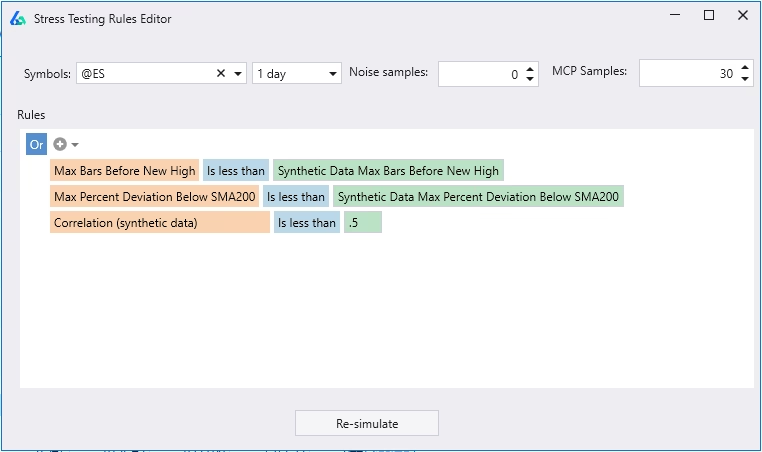

Custom Rules: Filter Your Multiverse

Build Alpha’s no-code rule builder lets you qualify which synthetic series make it into training. Set rules so the data matches the stress scenarios you want to prepare for:

📐

Correlation Filter

Only use series with 0.25–0.75 correlation to original

📉

Larger Drawdown

Synthetic must have deeper drawdowns than history

⏳

Slower Recovery

Must take longer to recover from max drawdown

🌊

Higher Volatility

Require increased volatility regimes in synthetic data

🔗

Combine OR

Chain rules with OR — each gets its own color on the chart

📊

Summary Stats

View how each rule performed independently below the display

Synthetic Data in Walk-Forward Optimization

Build Alpha’s walk-forward optimizer can inject synthetic data into the process. Select Simulate with Synthetic Data, choose the symbol, timeframe, and data-generation methods, then set qualifying rules.

For example, Build Alpha creates 200 synthetic series but only includes those with correlation between 0.25 and 0.75 to the original. The synthetic results are included in pass/fail scoring — parameters must work across both the historical path and synthetic series to pass. See also Noise Test Parameter Optimization which leverages synthetic data for parameter selection.

✓ Why This Matters

Market shocks are what gets system traders in trouble. By generating synthetic data with your desired “shocks,” you can stress-test your strategy against the market you fear before it happens. This is preparing for the probable future, not optimizing for the certain past.

Build Alpha v3’s automated workflows run this entire pipeline. Set filters, hit simulate, and only see strategies that survive everything — including training across the multiverse.

Takeaways

✓ Key Takeaways

Training on synthetic data is pre-simulation — fundamentally different from post-simulation robustness tests

Three built-in methods: Vs Shifted, Noise Adjusted, Monte Carlo Permutation — plus GANs, deep learning, and custom imports

BSK results show performance across all paths; color-coded equity curves reveal method-specific behavior

💡 Need to Know

Building on a variety of synthetic methods diversifies away pitfalls from any single generation approach

Synthetic data integrates with walk-forward optimization — results count in pass/fail scoring

Synthetic data refers to artificially generated price series that differ from actual historical data. Methods include noise adjustment, Monte Carlo permutation, Vs Shifted, GANs, and custom imports. They represent alternate realities — plausible price paths the market could have taken.

The standard Noise Test is post-simulation — build first, then re-trade on noise-adjusted data. Building on synthetic data is pre-simulation — the genetic algorithm trains across the historical path AND synthetic series simultaneously from the start.

Three built-in methods: Vs Shifted (shifts bar boundaries), Noise Adjusted (adds/subtracts volatility), and Monte Carlo Permutation (shuffles log price increments). Custom data can be imported for advanced methods like GANs or deep learning.

Yes. Build Alpha’s no-code rule builder lets you qualify synthetic data by correlation, drawdown depth, recovery time, volatility, and more. Rules can be combined or evaluated independently with color-coded results.

Yes. Build Alpha injects synthetic data into the walk-forward process. Synthetic results are included in pass/fail scoring — parameters must work across both the historical path and synthetic series to pass.

A decade-plus in professional trading as a market maker and quantitative strategy developer at a high-frequency trading firm with a CME seat. Self-taught C++, C#, and Python programmer specializing in data science, machine learning, and trading strategy development.

What Traders Say About Build Alpha

Train for the Unknown Future

Build strategies across hundreds of alternate price paths. Three generation methods. Custom stress rules. No coding required.

Portfolio trading is combining many independent, uncorrelated trading strategies into one shared account to gain some net benefit from their combination. One should design automated trading systems to handle and capture different market effects and environments to maximize this benefit.

Next, one needs to figure out how to combine these trading strategies to best improve the overall risk-adjusted return (or whatever your portfolio’s objective may be). This is [successful] system trading 101.

A Portfolio backtest splits the starting capital among the various individual trading strategies to see how the interplay of strategies affects the shared capital pool (aka our account).

In this post, I will discuss how we rebalance capital, why we rebalance capital, when to rebalance capital, and why we need many uncorrelated trading strategies vs. a single “holy grail” strategy.

Why Portfolio Trading?

There is no “holy grail” strategy. Sorry. I have been using machine learning and artificial intelligence for a decade-plus and have yet to find it. What’s worse is that over-optimizing, constant tweaking, and adding complex rules produce great-looking backtests which fail in live markets. Trust me.

The real “holy grail” is combining multiple strategies into one capital-aware portfolio.

The goal isn’t one perfect strategy — it’s a team of [robust] strategies that work well together. Some perform in bull markets, others in bear markets; some thrive in calm conditions, others in crises. Since no one knows what tomorrow brings, your portfolio should be prepared for all environments.

To do this, strategies must be different from each other. If they’re too similar, you’re just taking the same risk twice while adding operational complexity (yuck). We measure difference with correlation: ideally, when one strategy zigs, another zags — like pistons in a car engine (some up, some down but car moves forward).

Mixing strategies across assets, timeframes, frequencies, and styles (effect capture) builds a far more robust portfolio.

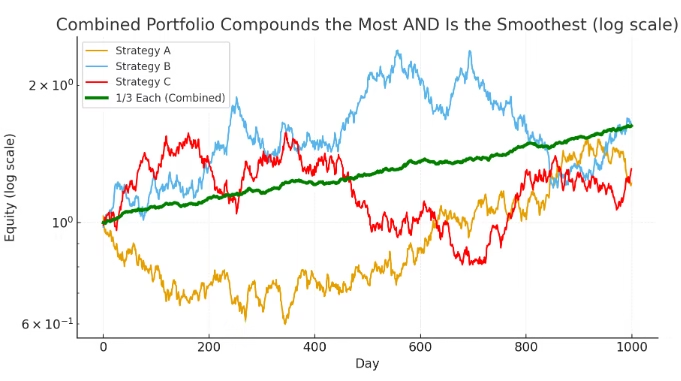

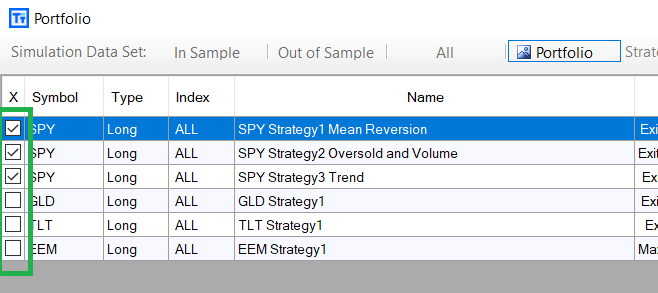

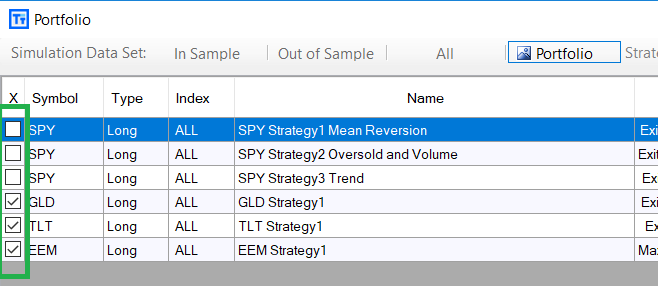

Combining Strategies to Improve a Portfolio

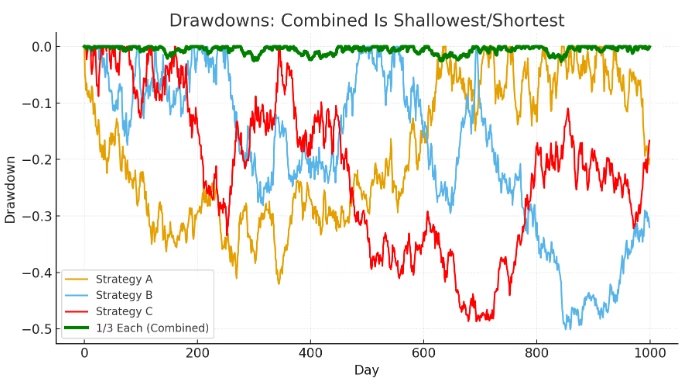

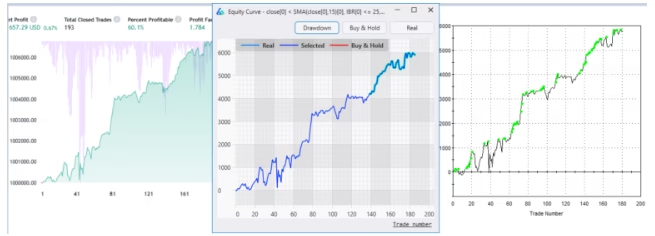

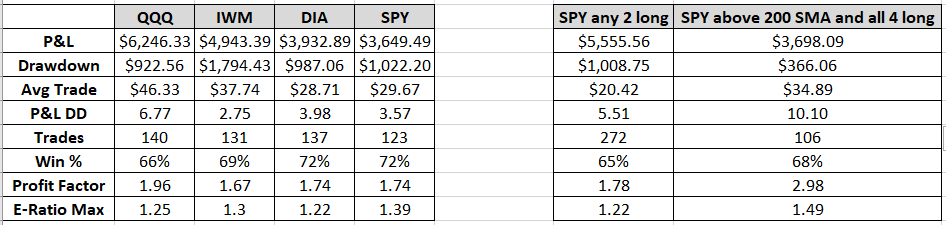

Below are three simple strategies that no one would trade by themselves. However, the historical drawdowns of these three strategies do not happen at the same time so when the strategies are combined, we notice improved performance (green equity curve).

And notice the drawdowns! On its own, each strategy experienced a 40%+ reduction from its peak equity at one point, but the combined hypothetical example never experienced even a 5% haircut.

This, generally speaking, is what we aim to achieve with portfolio trading. The coveted “holy grail”.

Parrondo’s Paradox in Trading

Wikipedia defines the Parrondo’s Paradox in Game Theory as “a combination of losing strategies that becomes a winning strategy”. Below is a brief video explaining Parrondo’s Paradox and loosely explains what system traders aim to achieve by combining uncorrelated strategies together.

This video begs the question: can we combine two bad strategies into a winning strategy?

The answer is (mostly) yes, but it is not done through simply combining two bad strategies together. We cannot just mash any two strategies together and voila.

An example portfolio

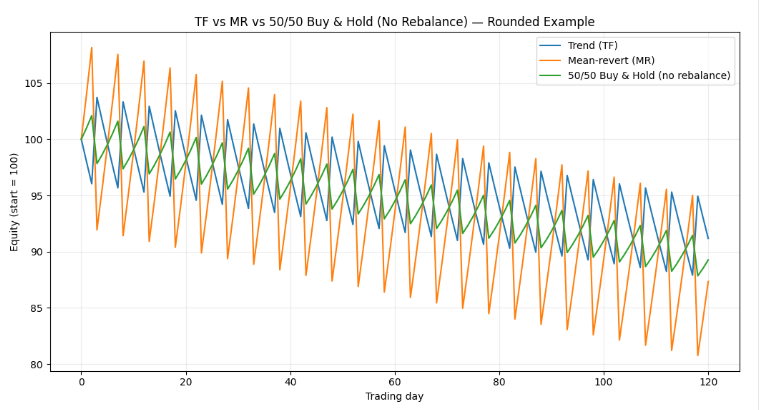

Trading is never that simple. Take this simple proxy portfolio

Trend Following (TF) proxy: 20% win rate, 8% average win, -2% average loss

Mean Reversion (MR) proxy: 80% win rate, 4% average win, -15% average loss (occasional crash)

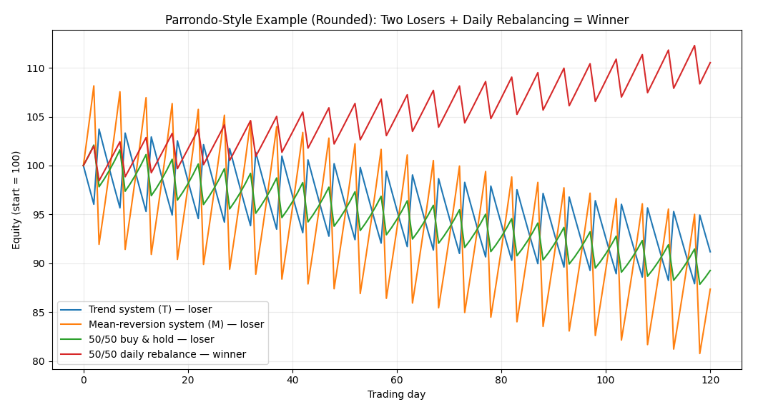

Both of these systems are losers on their own (negative geometric return). And if we give each 50% of our capital and mash together as a portfolio we still lose (green line).

But wait…

Portfolio Rebalancing is key

Rebalancing our capital every day turns the combined equity curve into a winner (red line). The “daily” 50/50 rebalancing mechanically sells what just went up and buys what just went down.

When strategies are sufficiently uncorrelated or negatively correlated, and volatile enough, this creates a rebalancing premium (sometimes called Shannon’s Demon).

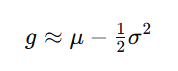

The effect or positive return comes from harvesting the volatility when we rebalance the capital. In quant speak, the geometric return is roughly the arithmetic return – 1/2 of the variance.

As we combine strategies (and rebalance the capital) the portfolio variance drops a lot more than the arithmetic mean does. This can flip the geometric mean positive!

In English please…

That is, we must pool the capital together and reallocate periodically in order to experience Parrondo’s Paradox in our trading accounts.

Not so fast

So just rebalance every day? No, there’s trading costs. And why 50/50 rebalancing? And what about correlation? And what if mid-trade our 50/50 weighting becomes 70/30? And what if, and what if, and what if, and.. hold on.

Rebalancing isn’t magic. It only helps when the strategies take turns leading (low/negative correlation) and have enough volatility/dispersion to harvest — and even then, trading costs can erase it.

Rebalancing can also hurt when one strategy is the clear long-run winner: you’re constantly selling the winner to buy the laggard, which reduces terminal wealth. We rarely know if we’ll have one long-run winner or which it will be, though.

In other words, if the strategies don’t “take turns” (correlated or very different long-run growth rates), frequent rebalancing can act like a “sell your best idea” tax.

In short, it is vital to combine uncorrelated, unrelated strategies to capture this effect! Not similar strategies.

So where does that leave usnow?

New Questions

We know we want to combine unrelated strategies but now have new variables and a bunch of new questions. For instance, we now ask:

what strategies to combine

what weights to give them

what correlation is acceptable

how to size strategies

show we rebalance capital

how often to rebalance

what about in-trade adjustments (e.g., 50/50 becomes 70/30)

Yep, an explosion of new things to test. “Hey, I’m barely working my way through my strategy ideas and now I have to answer portfolio questions? Come on, man. Can BA help?”

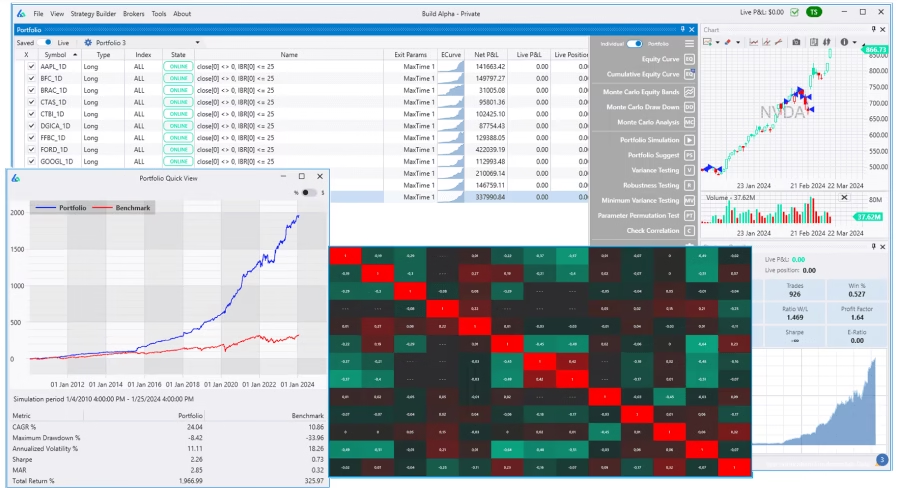

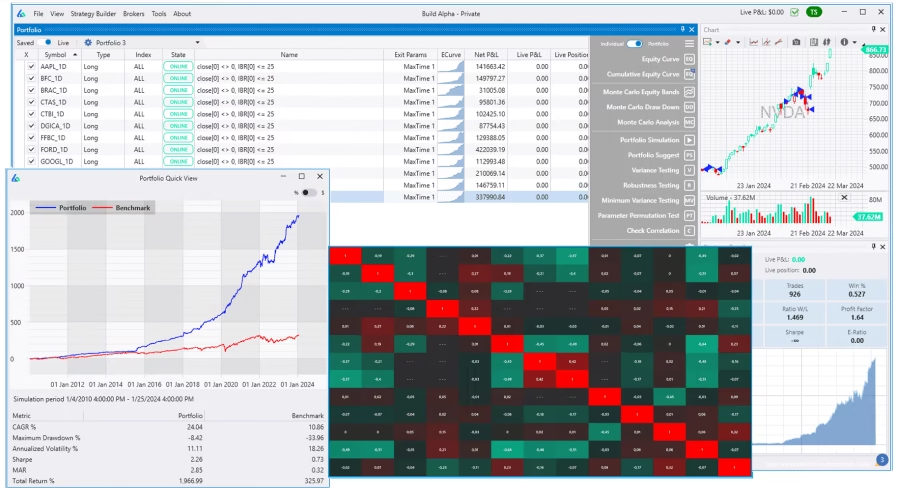

Build Alpha Portfolio Mode

Build Alpha’s portfolio mode enables traders to save strategies, combine them, analyze asset allocation methods, optimize rebalancing frequencies, and more. Let’s go through some of the core features below.

Fundamental Data and Factor Analysis

Build Alpha signed a data deal with the Nasdaq to offer fundamental data for building trading and investment strategies. This allows equity traders to filter symbol universes to only trade when Free Cash Flow or Revenues or Price to Book or PEG ratio or any other fundamental data point is to your liking.

This also enables Build Alpha to build and test various factor models such as market, size, value, profitability, investment, momentum, etc. The price data provided by Nasdaq is split and dividend adjusted.

Combining investment strategies built on different factors is one of the most time-tested methods for portfolio construction.

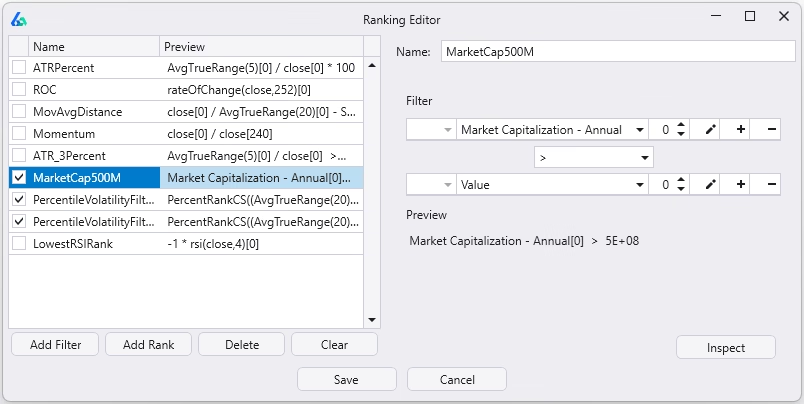

Custom Filters and Ranks

Filters are rules of what is trade-able and what is not. For example, only trade stocks or ETFs with an average daily volume greater than $10,000,000 or only trade futures with an average true range (ATR) at or above the 70th percentile or growth mutual funds above $5 or whatever.

Ranks are how you determine what symbol gets an allocation when you have more entries than available slots.

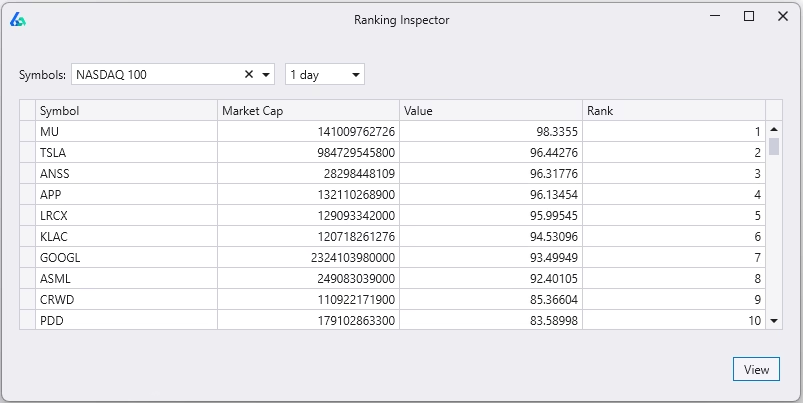

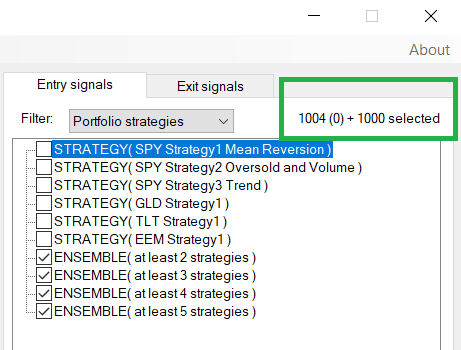

We can rank on anything: relative strength, volatility, market cap, momentum or any custom ranking you can imagine. Use the no-code editor to build rankings and review current rankings using the Rank Inspection tool (pictured below).

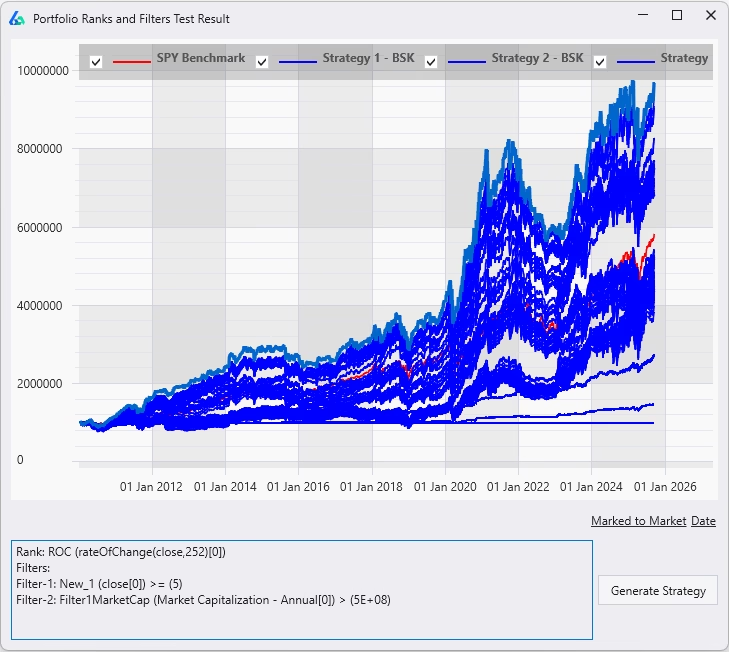

Create a library of filters and ranks, and let Build Alpha show which ones work best for your strategy.

The results above show different combinations of filters and ranking methods applied to the core strategy. The selected row shows how the strategy performs when stocks under $5 or below $500M in market cap are excluded, and the remaining stocks are ranked by 252-day rate of change.

Portfolio Analysis and Visuals

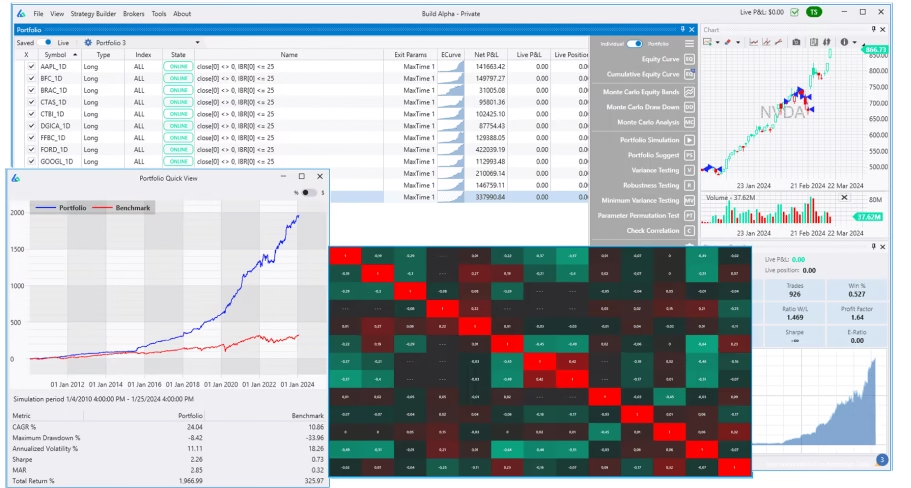

Build Alpha portfolio mode comes with all standard visuals and metrics such as equity curve comparison to buy and hold, performance metrics, correlation matrix, minimum variance test, and the institutional-grade robustness tests you all know from Build Alpha. Below shows an equity curve and correlation matrix.

A Quick Note About Other Portfolio Backtesters

Most portfolio tools just merge trade lists (txt or csv files) from multiple strategies. This cannot model real portfolio behavior because it does not know how trades would change when strategies share capital.

Example: a strategy that sizes positions based on stop-loss distance might only take 3 trades in its own backtest because capital was fully used. In a real portfolio, profits from other strategies could free up enough capital to take a 4th trade—but a trade-list simulator will never add this 4th trade, so the results are unrealistic.

Build Alpha solves this by re-simulating the strategies together, tracking capital in real time and letting strategies interact the way they would in live trading—something static trade lists can’t do.

Build Alpha – An Adanced Portfolio Backtesting Tool

Build Alpha is built for both independent traders and professional managers (CTAs and RIAs) running multiple strategies across multiple client accounts. It’s flexible enough to support a wide range of workflows and requirements—while also avoiding the common portfolio-simulator pitfalls mentioned above.

Backtesting Portfolio Strategies with Various Exit Strategies

Many equity investors and Registered Investment Advisors utilize strategies that rank a symbol universe periodically and only trade the top N signals. However, what happens when a position grows to be too large a percentage of your portfolio? Should we immediately reduce size? Or what happens if the stock falls out of the top N ranked stocks? Should we immediately close the position and add a position in the newly ranked stock?

New questions mean new tools.

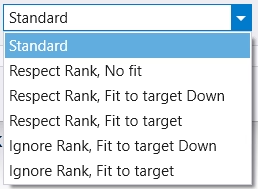

Build Alpha has various exit modes for portfolio strategies to give traders flexibility:

(Terms: Standard exit = stop-loss, trailing stop, or signal exit. Rank = position’s standing vs your universe. Fit to target = enforce position-size target E (e.g., 10%). “Down only” trims but never tops up.)

Standard — Close the position only on a standard exit. Ignore rank and size while held. Lets winners run (no trimming if it appreciates or drops in rank).

Respect Rank, No Fit — Close on any standard exit or when the stock falls out of the top N (your max positions). Example: Max positions = 10; if a holding becomes rank 12, it’s closed.

Respect Rank, Fit to Target Down — Same as above plus enforce max exposure E: trim if the position grows above E; do not add if it falls below E.

Respect Rank, Fit to Target — Same as above, but rebalance both ways: trim if >E and top up if <E.

Ignore Rank, Fit to Target Down — Close only on standard exit; ignore rank changes. Trim positions that exceed E; never add when below E.

Ignore Rank, Fit to Target — Close only on standard exit; ignore rank. Rebalance to E whether the position is above or below target.

These provide the trader or investor the ability to create constant volatility targeted portfolios or ones that hold for the long-term aiming to capture large trends. This flexibility is paramount with many use cases.

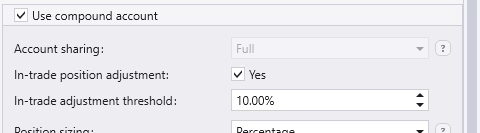

In-Trade Adjustments and Rebalance Periods

We have all been in a trade when volatility drastically changes. That is, we may size based on current volatility but a few bars later the volatility has collapsed, and we do not have enough exposure or a few bars later volatility explodes, and we have too much exposure!

Build Alpha allows traders to enable In-trade adjustments where Build Alpha will re-size positions if they deviate from the desired or current size by a certain percentage threshold. Below would re-size a position whenever the current exposure deviates 10% or more from your desired position size.

This constant or continuous adjustment helps smooth returns and helps traders and investors target certain volatility levels.

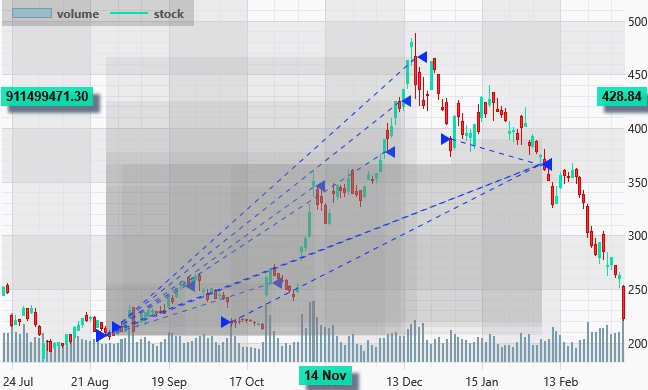

This is akin to a Hold ’em Poker player changing his bet as new cards (data) are unveiled. A poker player doesn’t determine his bet size at the beginning of the hand and wait until the end of the hand (trade’s exit). He adjusts his exposure mid-hand, multiple times often. However, in trading, we can adjust our exposure both up and down – how cool!

Here is an example TSLA trade with many in-trade adjustments (buys and sells to resize the position as needed).

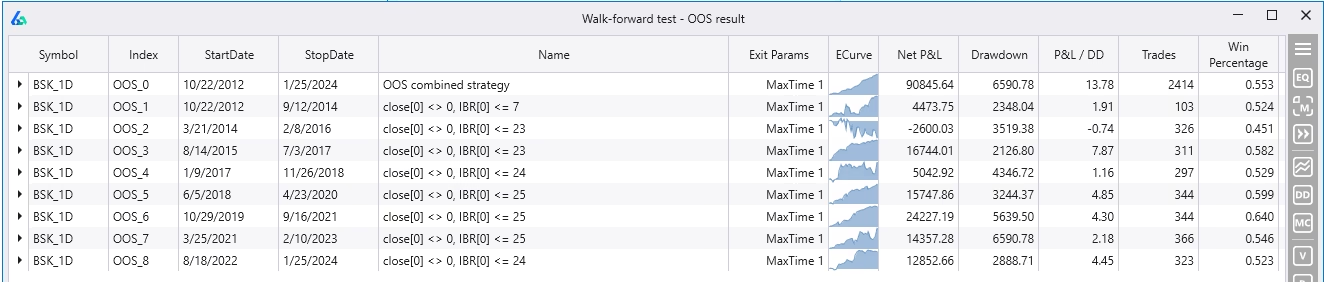

Walk Forward Test to Backtest Portfolio Strategies

Walk Forward Testing splits the historical data into multiple training and testing partitions where we optimize strategy parameters during the training data (in-sample data, blue below) and test the best parameter settings on the unseen (out-of-sample, green below) data.

This process is repeated until we “walk forward” through the entire historical data set which ultimately allows the trader to combine all out-of-sample data (green boxes) into one truly out-of-sample equity curve.

Build Alpha enables you to do this with a single strategy or a portfolio of strategies and you get this results window which shows performance and risk metrics for every out-of-sample period for the portfolio. Expand any row and view the individual strategies’ performance during any OOS period.

One can gain insights into how often one should re-optimize a strategy or how much ideal parameters have/do change over time. I wrote more about Walk Forward Optimization here.

Portfolio Suggest – AI Asset Allocation

Build Alpha’s Portfolio Suggest feature is a single button that enables Build Alpha’s AI, that was trained on thousands of strategies and market environments, to sift through your saved strategies and suggest the best sizing method, exit modes, combination of strategies, weightings, and more so you do not have to test every combination yourself.

Below are results of the Portfolio Suggest feature. The blue lines are various combinations, weightings, sizing methods that Build Alpha simulated based on the saved strategies in the portfolio. The red line is Buy and Hold (S&P 500).

See what settings were applied to create each equity curve. The Generate button opens a new results window for the selected settings for further analysis.

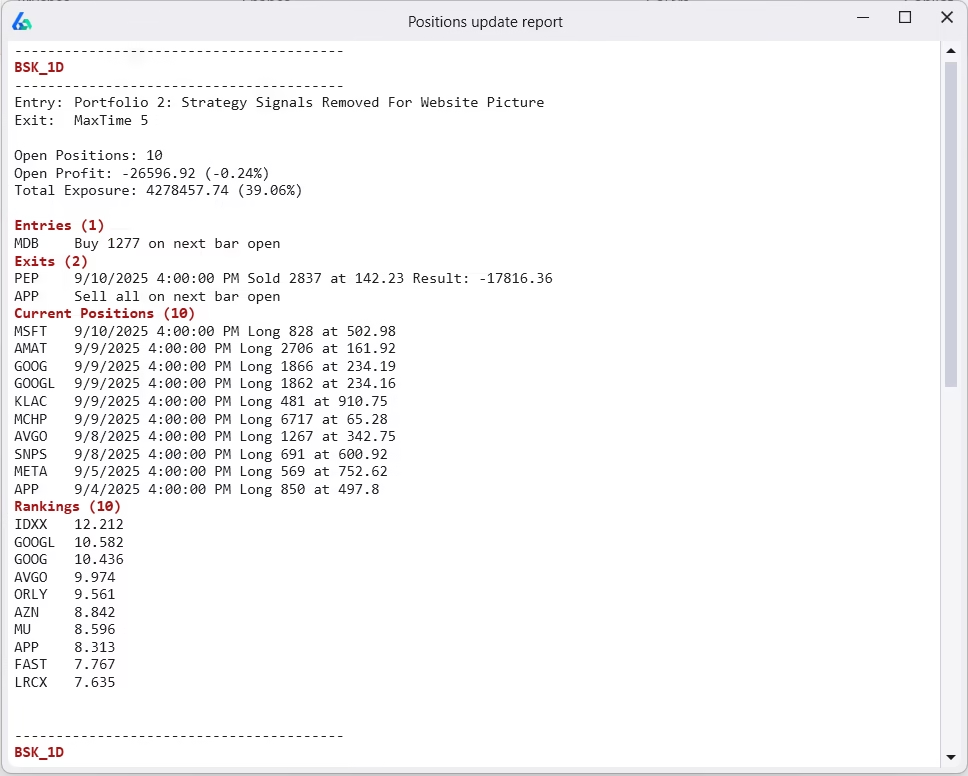

Position Update Report

Build Alpha runs a daily report to update all your saved strategies. This overview gives an update on every saved strategy. The report includes:

What to enter

What to exit

Current Positions

Current Rankings

Open P&L

Funds Available

Total Exposure

This is the simplest way to track portfolio strategies and get daily updates. This is also for all of the new Build Alpha members that are not ready for full automation! The data updates overnight so this feature is best run before the US market opens.

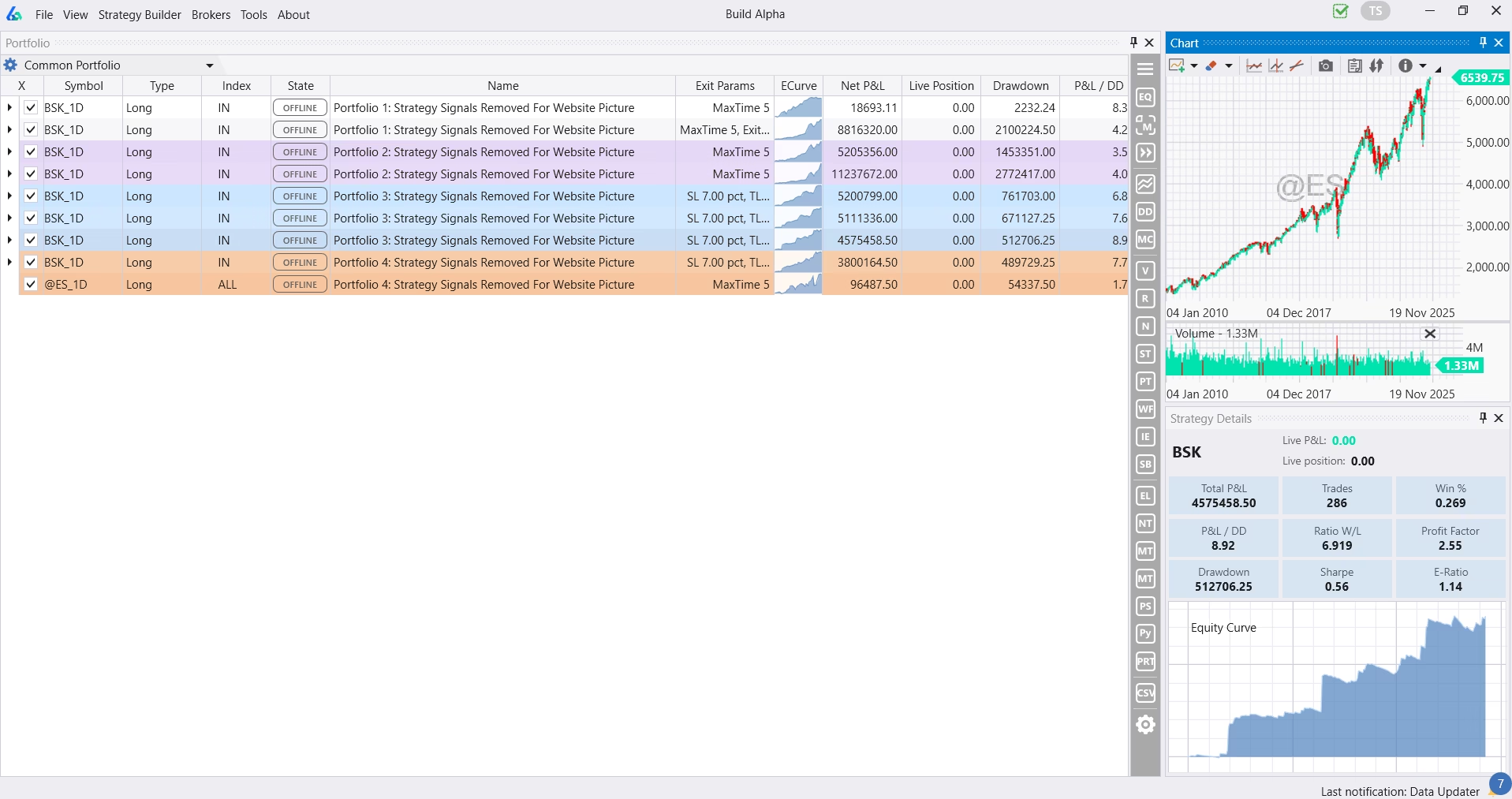

Multiple Portfolios in one place

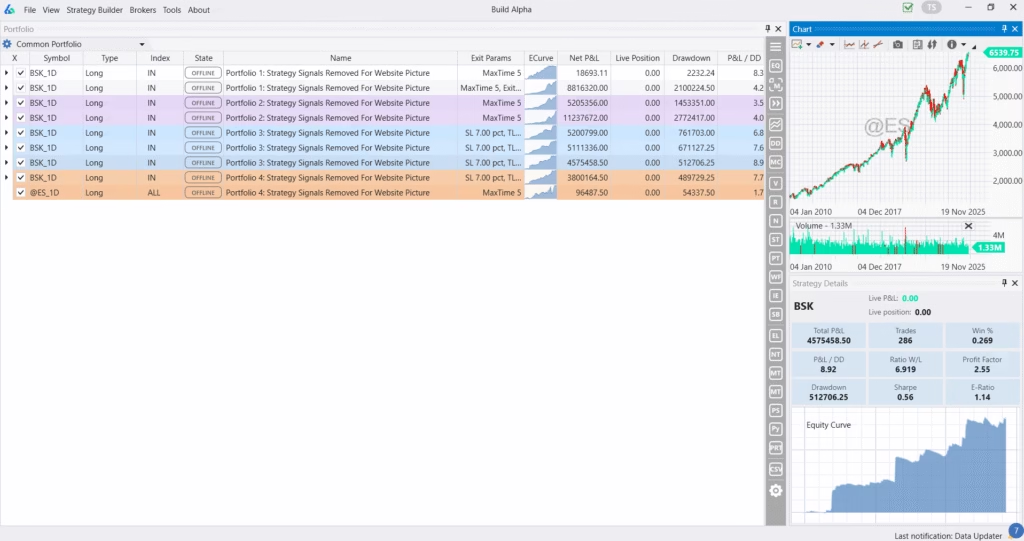

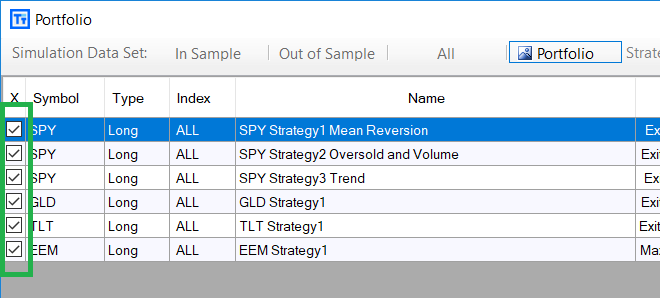

Color code, name, and organize all your saved strategies into different portfolios. This gives a one screen summary to view risk metrics, compare strategies, and keep tabs on all your hard work. There is a dropdown in the upper left that will allow you to move between each portfolio or view the combined Common Portfolio (pictured below).

Build Alpha Portfolio Mode

What’s Included

Multi-strategy portfolio simulation

Portfolio Suggest AI

Multi-strategy walk-forward testing

Portfolio filters and ranks

In-trade volatility adjustments

Fundamental data access (Nasdaq)

Ranking inspector

Save multiple portfolios

Daily position update report

Please email me with any questions and check out the Build Alpha V3 Update to see what else is new in the latest release.

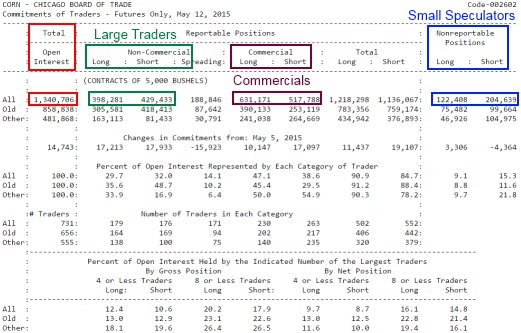

The Commitment of Traders Report is a weekly report released by the Commodity Futures Trading Commission (CFTC) that shows the open interest for futures and options on futures in markets with 20 or more traders holding positions above or equal to the reporting levels established by the CFTC. The report shows open interest data as of Tuesday but is not released until Friday afternoon.

The reports are based on open interest position data supplied by reporting firms such as FCMs, clearing members, foreign brokers and exchanges. The data is categorized by the trader’s dominant business purpose self-reported by traders on the CFTC Form 40 and is subject to review by the CFTC.

The report is broken down into three different types of traders:

Commercial traders (hedgers): Traders in this category are typically considered to be market professionals, such as producers, processors, users, merchants, and swap dealers. These traders use futures markets to hedge against price changes in the underlying commodities. They are considered to have a direct commercial interest in the underlying commodities.

Non-commercial traders (large speculators): This category of traders is considered to consist of speculators who trade futures contracts for financial purposes, rather than to hedge against price changes in the underlying commodities. These traders include hedge funds, Commodity Trading Advisors (CTAs), individual traders, and other investment firms.

Nonreportable (small traders): These traders are defined as those holding positions below the reporting levels established by the CFTC. Traders in this category are considered to have less impact on the market and provide valuable insight into market sentiment and behavior. Their positions are classified as non-reportable positions in the COT report.

Smart Money vs Dumb Money

The COT report is broken down into three categories of traders and often the commercial traders and to a lesser extent the non-commercial traders (large speculators) are considered “smart money”. The nonreportable category is often called small speculators or retail traders which unfortunately gets the moniker “dumb money”.

Watching the divergence between smart and dumb money can often leave clues to direction or market sentiment which can help influence trading approaches. The most popular COT trading style is watching when these two categories diverge to extremes as large divergences between smart and dumb money is typically when or how the market moves. Someone has to be someone’s liquidity!

Is there Free COT Data?

Yes, COT data is freely available on the CFTC’s website at cftc.gov and then navigating to the Commitment of Traders report link here: Commitments of Traders | CFTC

However, the historical data from COT reports are not formatted for easy use and often needs modification to make useful futures markets signals. More on how Build Alpha does this later.

How can traders use COT data?

Simply using the commitments of traders reported data as a trade signal is not a great idea! The data is shared as long and short positions and is not normalized for Tuesday’s open interest. Instead, the values are just raw values and rather meaningless on their own. For instance, is a number of 10,374 contracts long a lot or a little? Well, it depends on what open interest is! And how many contracts are short!

There are two simple ways of deriving signals from COT data. First, the normalized net position which is expressed as a percent. Positive 20% would mean the net position is long and 20% of open interest. The second way is the COT Index.

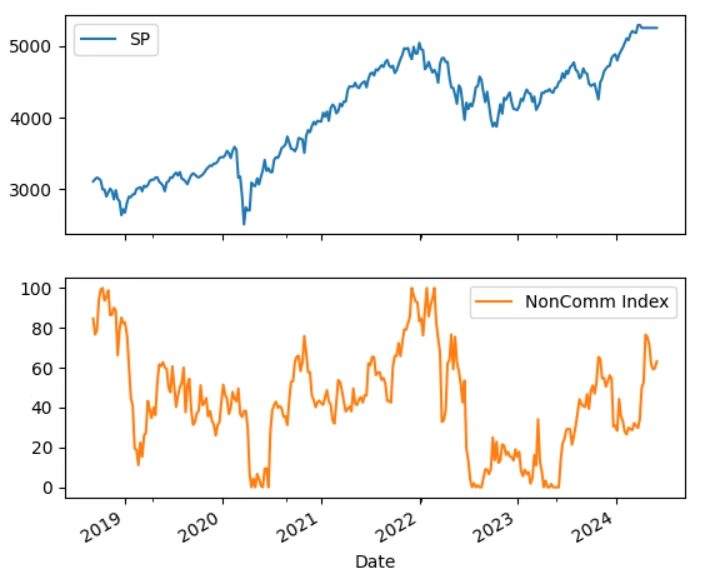

What is the COT Index?

The COT Index or Commitment of Traders (COT) Index is a popular trading indicator showing where current net positioning is in relation to historical positioning of the same trader group over the past three years (36 months).

A COT Index reading of 100 means the group is the most bullish compared to any point in the past 36 months and a reading of 0 means the group is the most bearish compared to any point in the past 36 months. The COT Index can be calculated on Commercials, Non-Commercials, or Non-Reporting traders.

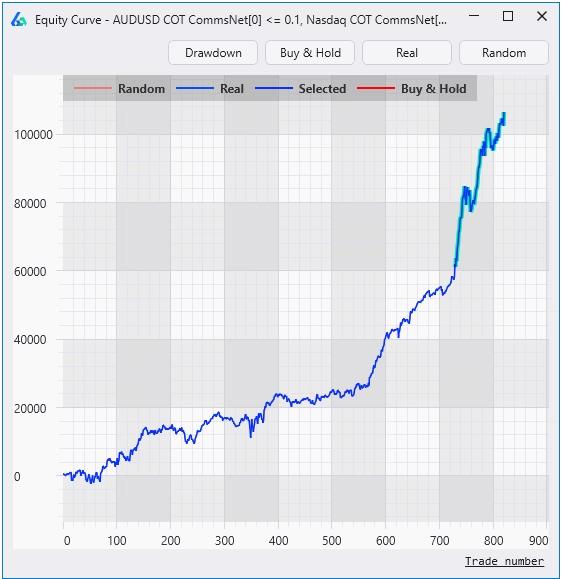

Above is an image showing the SP500 price fluctuations with the non-commercial trader (large speculators) positioning via COT Index over the past 36 months. Traders can isolate periods of extreme positioning to identify the start or end of a trending environment.

In Build Alpha, traders can test any COT Index value or range of values from the point-and-click interface. Here’s a sample strategy that goes long $10,000 per trade in QQQ (Nasdaq ETF) when Nasdaq futures non-commercials COT Index is less than or equal to 50. Simply being long QQQ when large speculators are less bullish (blue line) has drastically outperformed QQQ buy and hold (red line) over the past 20 years.

This signal can of course be improved by requiring this signal and having Build Alpha search thousands of other signals to find complimentary filters.

Simpler COT Trading Signals

The simplest COT trading signal is to look at the net position – subtract the shorts from the longs – so that a positive number means that particular category of trader is net long and a negative number means that category of trader is net short. If the net position is zero, long and short traders’ positions reported equal each other. It is common when there is no underlying bias or directional sentiment that traders hold positions equal to each other or close to it.

Further, we can then divide the net number by the total open interest to express a normalized value that can provide apples to apples comparisons over time or across markets. A value of -0.20 would be a 20% net position or 20% of open interest is positioned short.

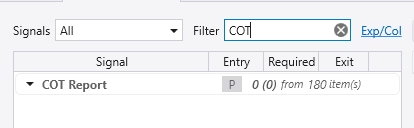

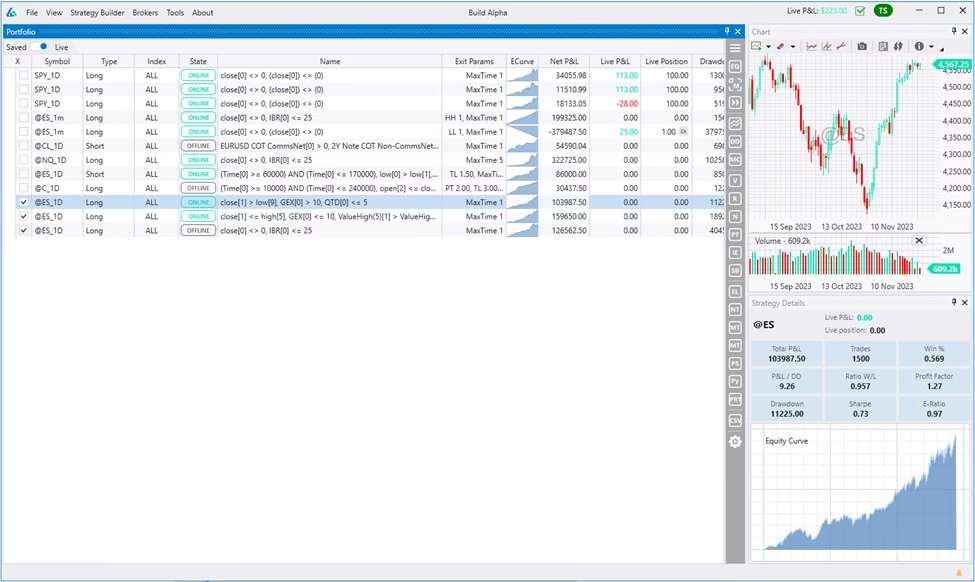

COT Report Trading Signals in Build Alpha

Build Alpha has COT data back to 2000 included in the 5,000+ built-in signal library. You can search for them in the top filter using “COT” as pictured below.

These signals can be used for entries, exits or general strategy filters. Build Alpha has COT data for the following markets:

S&P500

Nasdaq

Dow Jones

Vix Futures

AUDUSD

Dollar Index

EURUSD

2-Year Note Interest Rates

5-Year Note Interest Rates

10-Year Note Interest Rates

30-Year Bond Interest Rates

Natural Gas

WTI Oil

Silver

COT Report Trading Strategy Example

Index traders take a look at this one! This simple SP500 futures market strategy demonstration was built using Build Alpha’s COT signals. I only used the COT signals and did not use any other price, volume or non-price based entry or exit signals. This strategy enters whenever the following is true:

Nasdaq Commercials Net positioning 15% or less of open interest

Five-Year Note Commercials Net positioning 15% or less of open interest

AUDUSD Commercials Net positioning 10% or less of open interest

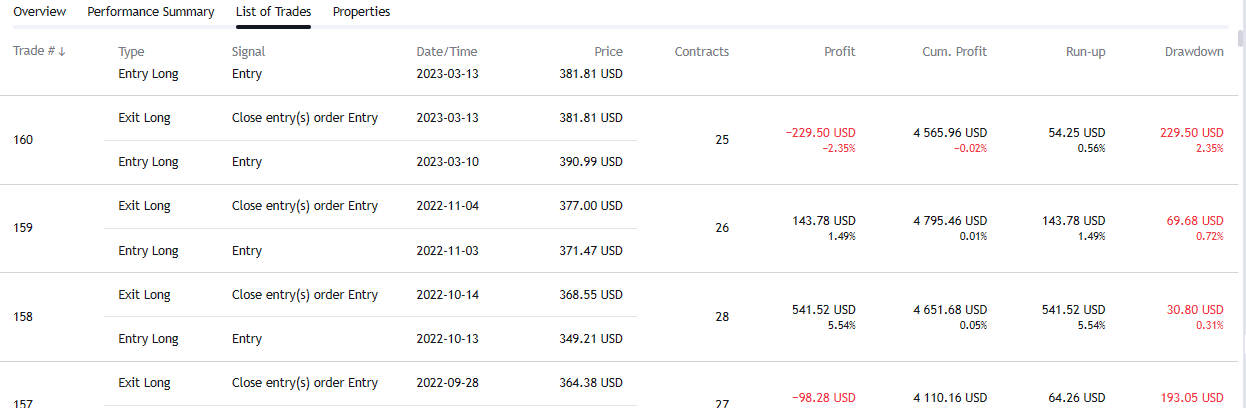

The strategy simply exits after one bar. Its performance below is from 2007 through 2023 using only one contract per trade.

COT Indicator or Filter

A better use of non-price data like COT report or other sentiment data is often to use the data as a filter to a price action or price and volume-based strategy. Price strategies often lack context about the market environment and as we all know patterns and signals act differently in different market conditions.

COT data and other non-price based data acts as a way to relay information about the environment to our trading systems.

Below is a simple example of how to find or improve a simple price action strategy with COT report data as a filter using the required signal functionality in Build Alpha.

Cool Ideas for using COT Data with BA

You can pair COT data with economic news events. For instance, perhaps it is only worth trading a news event when smart money is in the same direction. Perhaps intraday trading systems could benefit from a filter from larger players.

Summary

The Commitment of Traders COT Report is a weekly report released by the Commodity Futures Trading Commission which discloses open interest and market positioning in futures markets and options on futures markets for three different types of traders: Commercials (hedgers), non-commercials (large speculators), and nonreportable speculative traders (small trader).

The data gives insights into how market participants are positioning for future trends and give an asset manager or commercial traders an idea on market timing or pending market pressure. The report is released Friday but only contains data up until Tuesday.

Traders reports and other non-price-based data can be valuable contextual information to relay market environment or regime details to automated trading strategies. Build Alpha now contains COT report data for 15+ futures markets that can be used to create automated trading strategies without any coding.

Author

David Bergstrom – the guy behind Build Alpha. I have spent a decade-plus in the professional trading world working as a market maker and quantitative strategy developer at a high frequency trading firm with a Chicago Mercantile Exchange (CME) seat, consulting for Hedge Funds, Commodity Trading Advisors (CTAs), Family Offices and Registered Investment Advisors (RIAs). I am a self-taught programmer utilizing C++, C# and python with a statistics background specializing in data science, machine learning and trading strategy development. I have been featured on Chatwithtraders.com, Bettersystemtrader.com, Desiretotrade.com, Quantocracy, Traderlife.com, Seeitmarket.com, Benzinga, TradeStation, NinjaTrader and more. Most of my experience has led me to a series of repeatable processes to find, create, test and implement algorithmic trading ideas in a robust manner. Build Alpha is the culmination of this process from start to finish. Please reach out to me directly at any time.

What’s New in the Build Alpha Update

First, thank you all for the patience on this update. A lot has happened since the last update. Covid lockdowns, I built and sold another software company (now part of a public company), had two kids (being a dad is the coolest), consulted for a handful of funds, partnerships with TradeStation, Interactive Brokers, etc.

Long story short, I’m focused on Build Alpha and have a lot to share!

Here is a brief table of context of what is new in this update:

Live Data monitoring

Historical intraday database

Data Converter No Code

Automated Workflows

New Code Generators (Pine, IB, MT5)

Cryptocurrency Data

*Beta* Intelligence Report

Quantified Chart Patterns

Vs Shifted Test

Monte Carlo Permutation Test

Ability to train systems on synthetic data

Tonight Mode

Quick Test

Updated Custom Signal Builder

Machine Generated Rules

Signal Pools

OR Logic Exits

Conditional Signals

Dark Mode Option

Drawdown Normalization

Fixed Fractional Position Sizing

Position Sizing Scalers / Continuous Signals

Commitment of Traders Data

Weather Data

Market Breadth Data

Google Trends Data

Parameter Permutation Testing

Stress Testing or Scenario Testing

Walk Forward with Synthetic Data

Opening Range and Custom Entries

Custom Fitness and Correlation

Multi-strategy Portfolio Simulation

Portfolio Suggest

Daily Position Report

Live Data Monitoring

Build Alpha now connects to live data feeds for strategy monitoring and alerting real-time positions. This gives a much more reliable way to track hundreds of strategies than exporting code to your respective broker platform. Note: You can still export code for any strategy!

Historical Intraday Database

Build Alpha now has a historical database going back to 2006. The API connections are great for live data updating; however, the APIs do not always quickly provide historical data for testing and often fail with many consecutive API calls (or randomly).

Build Alpha can still use built-in data files, imported data files, API connections, and now the built-in historical intraday database. You can easily access built-in intraday data via the Server-side symbols dropdowns.

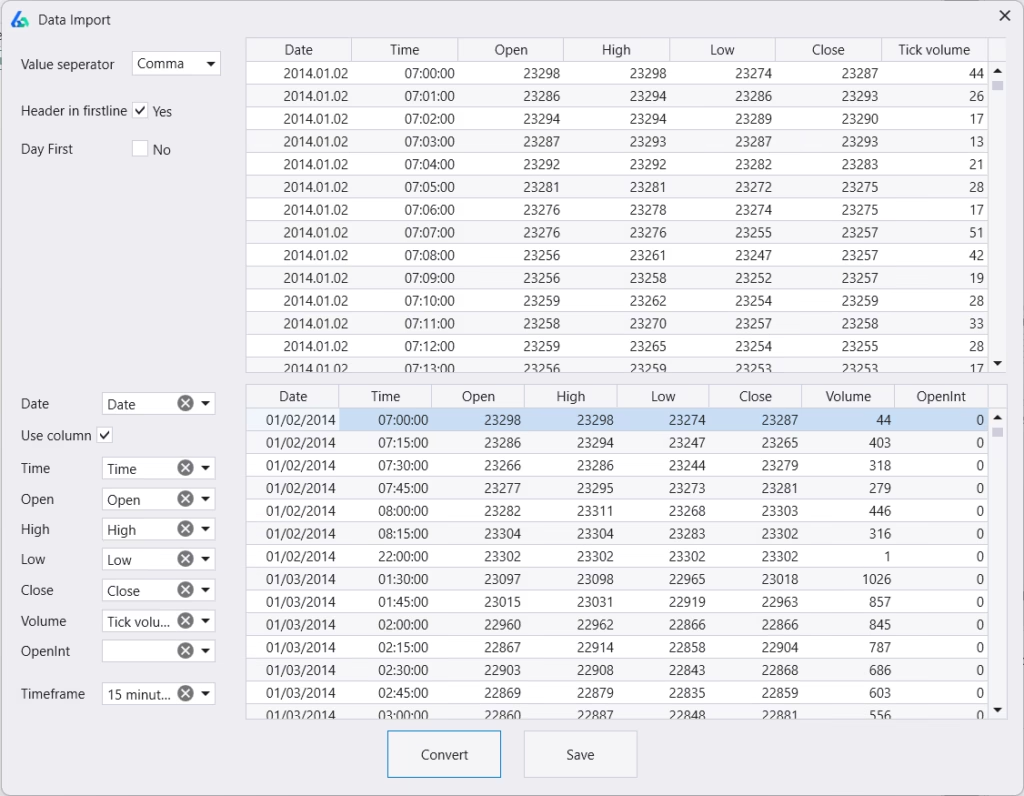

No Code Data Converter

Import any data file from any source with any format and Build Alpha will format it. No more converting or formatting with excel, python or ChatGPT. Includes the ability to resample (create) any higher timeframe as well.

Automated Workflows

Traders can now set in-sample, out-of-sample and combined results filters to automatically discard any strategies not meeting certain criteria. Traders can set performance metric thresholds to ensure strategies have a high enough winning percentage, high enough profit factor, trade frequently enough, etc.

Additionally, set advanced filters and automate robustness testing! For example, traders can specify the lower band of the Noise Test to be positive or the 90th percentile of the Variance Test to be x% of the backtest or various other ideas.

This makes finding strategies that fit your portfolio or risk criteria even simpler. Run a simulation and only see what passes your filters and tests.

This really makes it possible for lazy or busy people to develop exactly the algorithmic trading strategies they’re after in financial markets.

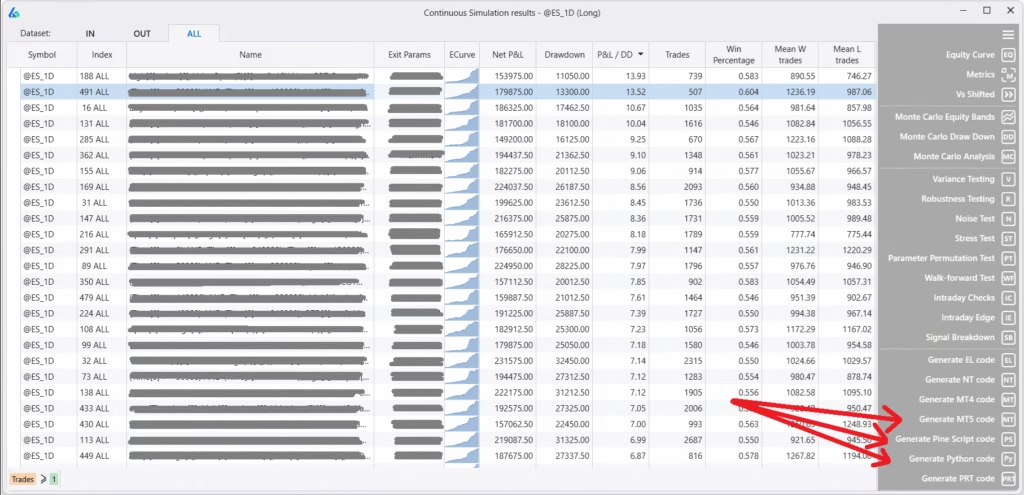

New Code Generators Added (TradingView, Interactive Brokers and Metatrader5) and Improved

Build Alpha now generates fully automate-able, trade-able code for any strategy it builds for TradingView (Pine Script), Interactive Brokers (Python) and MetaTrader5.

This adds to the existing list which now looks like

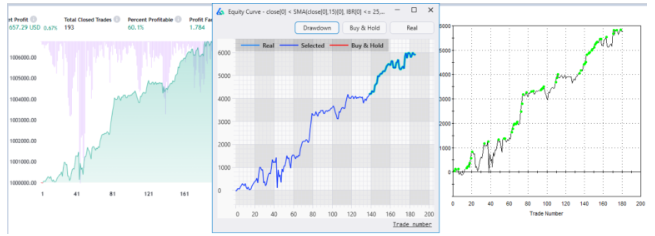

Read more on how and what TradingView Pine Script is and how it works with Build Alpha. You have full control over any generated code or trading algorithms. Image below shows TradingView (left), Build Alpha (center), TradeStation (right) displaying the same equity curve.

Additionally, I’ve revamped the Ninjatrader8 generated code. NT8 has grown in popularity as it appears to be the backend or broker of choice for many prop firms and prop challenges. Build Alpha (left) fully supports NT8 (right).

Cryptocurrency Data and Connectivity

You can now connect to Binance or use the historical database to build cryptocurrency strategies with no code. Binance connection will permit live position updating of any saved crypto strategies.

Build Alpha also supports fractional sizing so you can buy pieces of coins for accurate backtesting results and flexible position sizing options. Please suggest what other crypto connections I should add. Note: You do NOT need any of these connections to use Build Alpha.

Intelligence Report

Build Alpha can now review all your saved strategies and make suggestions to automatically help improve them. This is new [beta] AI feature has been trained on thousands of strategies and market environments. Anyways, you can run the Intelligence Report from the Brokers menu and any strategies with an IR icon have a suggested improvement. Click on the IR icon to view the suggested modification.

This has made strategy modification and improvement much simpler!

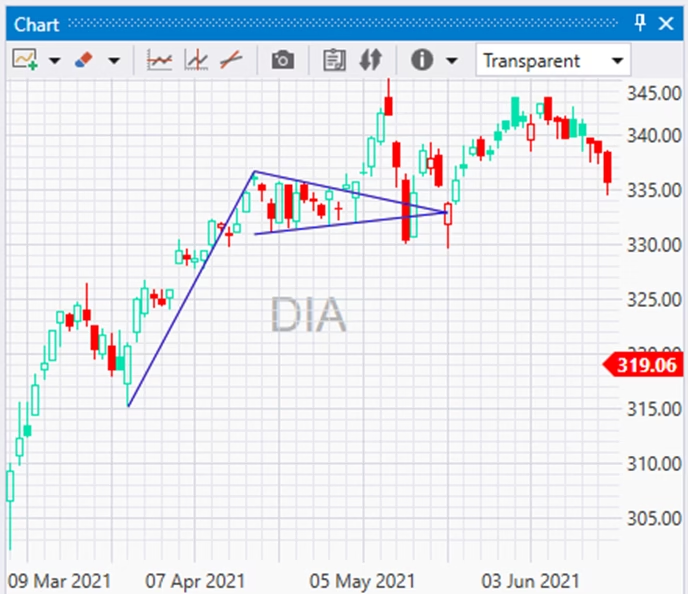

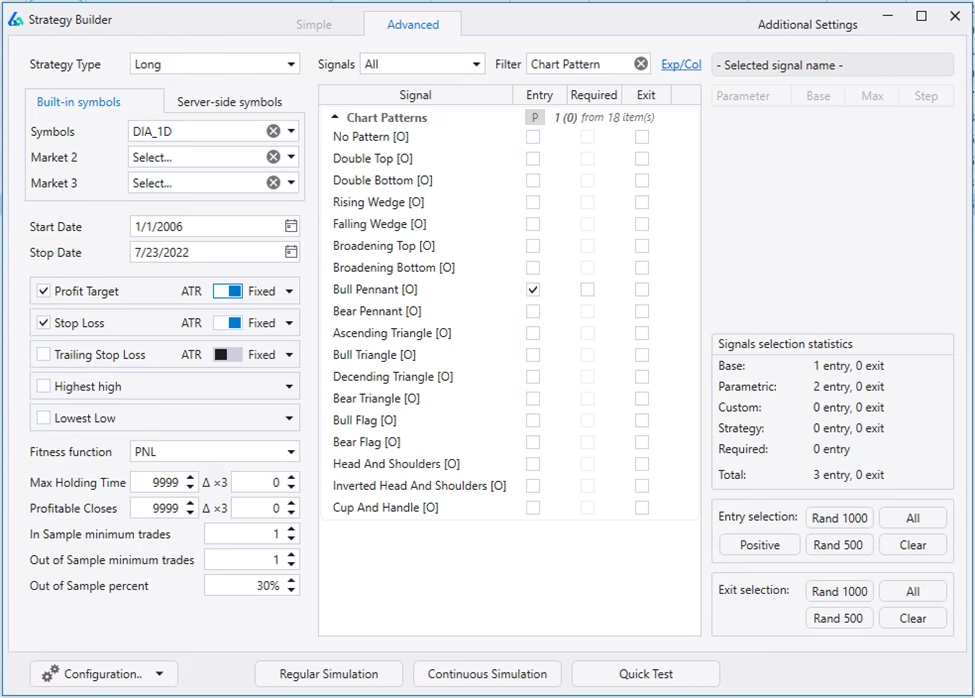

Quantified Chart Patterns

One of the largest requests from new traders (and some professional traders) is to test [infamous] chart patterns. To do so properly, the patterns must be quantified. That is finally possible in Build Alpha. The chart patterns Build Alpha now supports are:

Double Top and Double Bottom

Rising Wedge and Falling Wedge

Broadening Top and Broadening Bottom

Bull Pennant and Bear Pennant

Ascending and Descending Triangle

Bull Flag and Bear Flag

Head and Shoulders and Inverse H&S

Here is a quick example on $DIA ETF and how to select them as entry or exit signals in Build Alpha for testing

Vs Shifted Test

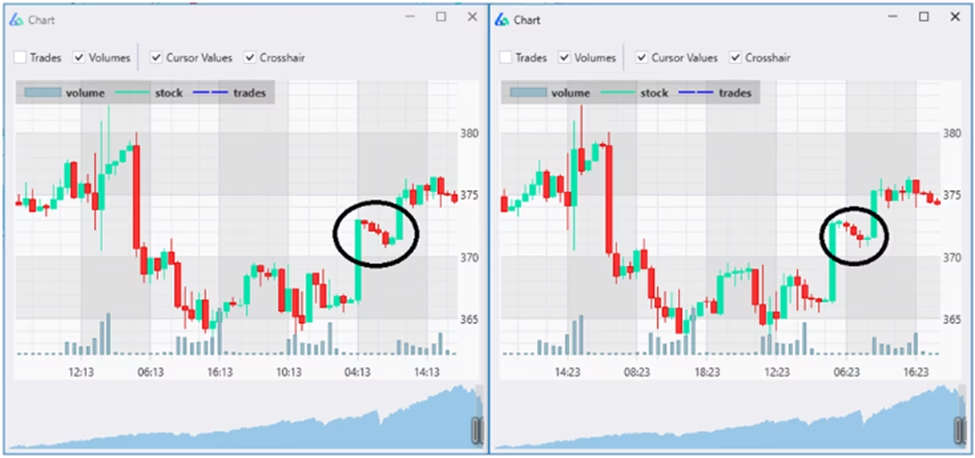

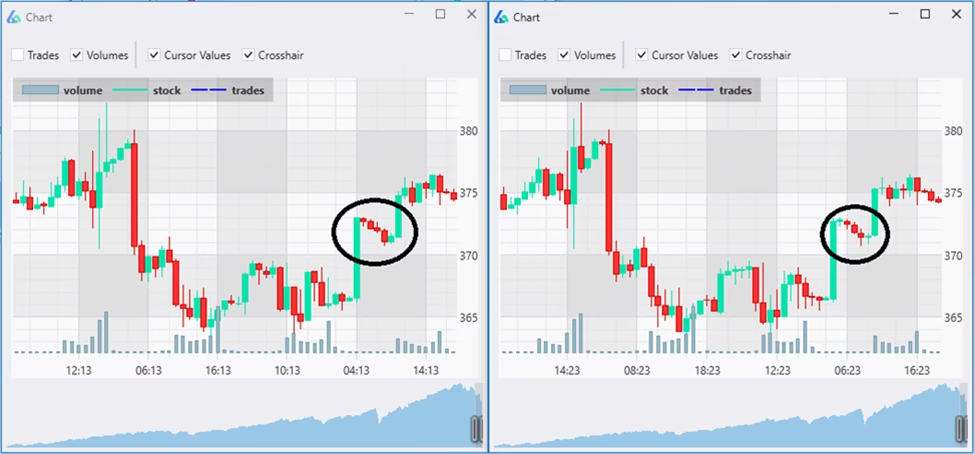

Every data provider uses hourly bars from the top of the hour to the end of the hour. That is, 11:00 to 12:00, 12:00 to 13:00, etc. However, shifting the opening and closing time can create additional data sets with near identical properties.

“Shifted Data” is a great way to evaluate if our strategies require the exact historical data patterns for success or will be robust to slight variations (spoiler there will be variations in live trading).

Shifting the data works on any timeframe. This test may change bar patterns, high and lows, consecutive up and down streaks, indicator calculations, and more.

Here is an example from my Complete Robustness Testing Guide, assume a long strategy needs four consecutive red bars to trigger a trade. In the original data (on the left), the strategy nailed a winner. On the shifted data (on the right), the trade never happened.

Re-trading your strategy on shifted data can give insights on how overfit your strategy was to the EXACT patterns available in the historical price data. Past performance should maintain across shifted data sets. If performance degrades, it may be a warning sign that the strategy is overoptimized (overfit). Here is one example of the Vs Shifted output

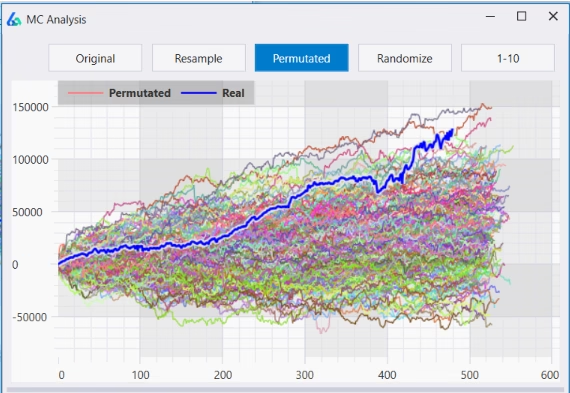

The Monte Carlo Permutation test takes the logs of interbar gaps and the intrabar OHLC relationships, randomizes their order, then exponentiates them back into raw OHLC prices. This process creates unique OHLC data while destroying any underlying patterns.

This newly created data, like other adjusted data sets Build Alpha creates, can provide another test set of data to make sure our data was not overfit to the actual historical data. I love multi-path tests like this! Another stress test for the arsenal.

Testing trading strategies on synthetic or altered data such as Noise-adjusted data, Vs shifted data, Monte Carlo Permuted data, etc. post simulation is a great way to identify curve fit or overfit strategies before trading them live.

However, can we use this altered data pre-simulation to build more robust trading strategies? This new feature in Build Alpha allows you to add altered data series to the genetic algorithm (simulator engine).

You can think of these altered data sets as alternate universes from a multiverse. The actual historical data we lived through is our universe, but these other universes were a possibility that we could have lived through. Since we don’t know what will happen next, we need a strategy that is robust across the multiverse!

Below is our universe in the upper left and three alternate universes. You can see each universe made all-time-highs at a different time and each took different paths (despite all ending at the same point).

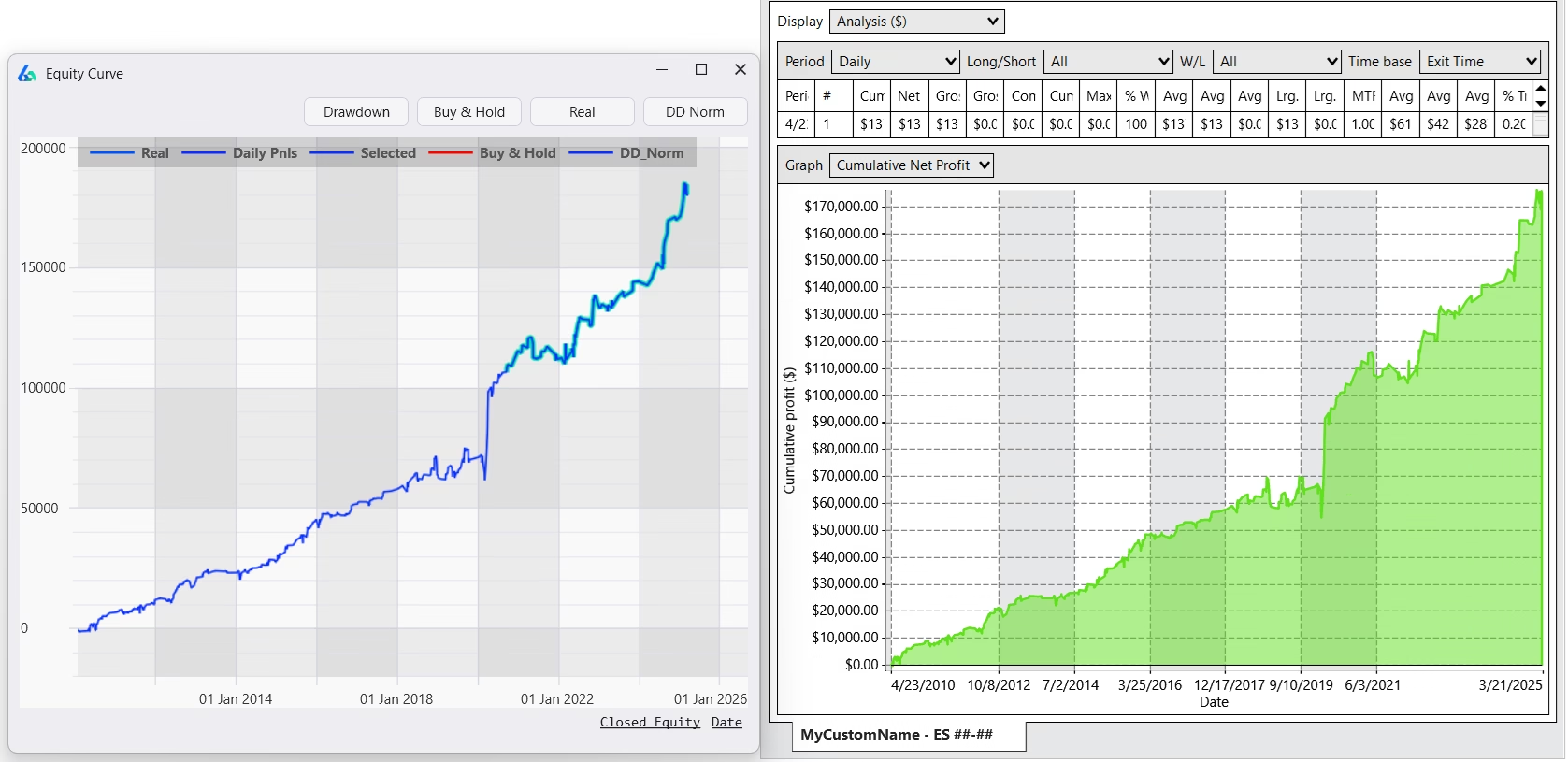

Build Alpha will return the results of the strategies that perform best across the basket (or multiverse) and you can breakdown and view each universe’s specific performance. The ‘MCP’ suffix denotes the underlying data for this strategy was generated via Monte Carlo Permutation.

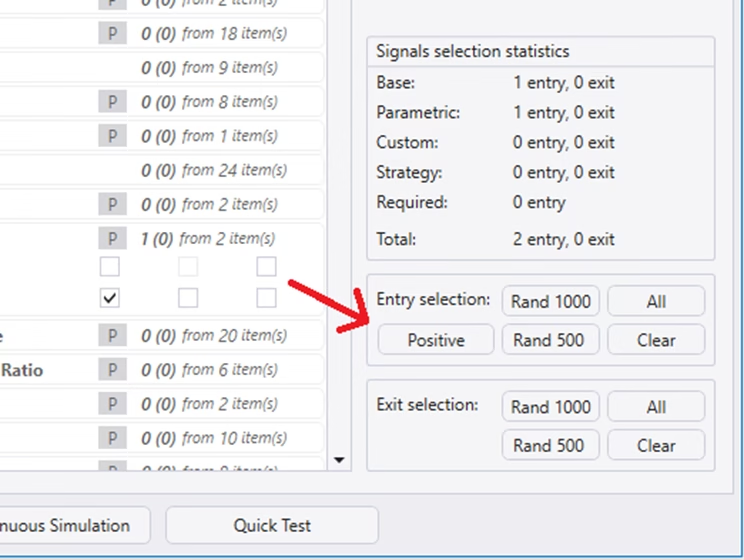

This feature automatically selects all entry signals that are true for the given day. Select the symbol and date, then hit the ‘Positive’ button and Build Alpha will auto-select every true signal. Very cool feature to find things for the coming day, week, etc. It also helps those who have trouble coming up with trading ideas.

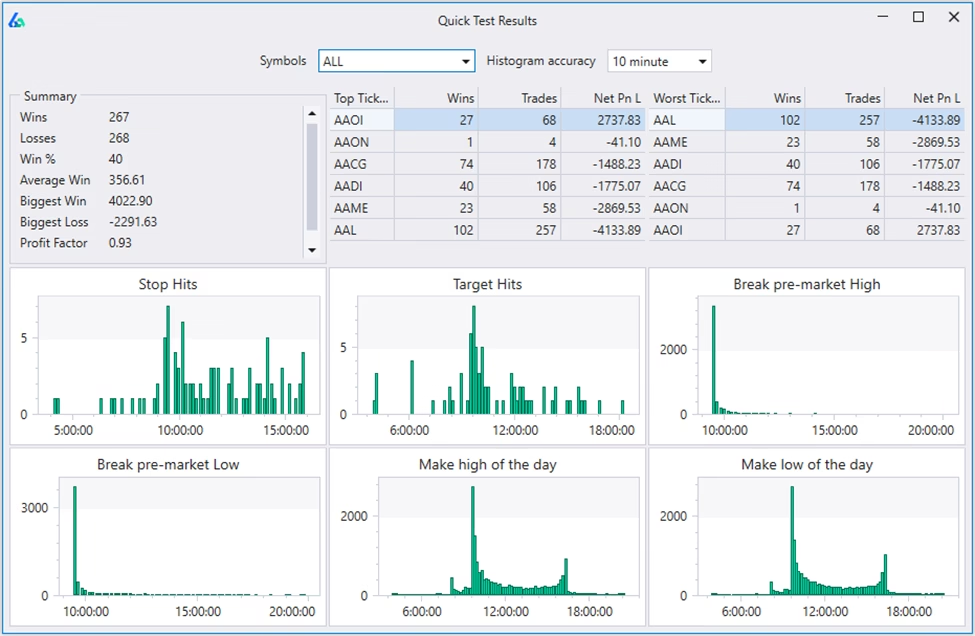

Quick Test

A quick and dirty way to get high level insights into a trading strategy. This enables traders to configure their entry, exits, stops, targets, symbol universe and hit ‘Quick Test’.

The Quick Test will provide a breakdown including:

Summary of results

Top Tickers

Worst Tickers

When stops are hit

When profits are hit

When breaks pre-market high

When breaks pre-market low

When makes high of day

When makes low of day

One beta user described this as “an incredible weapon” to investigate and extract more edge from a trading system. For forex, futures and crypto it will check 24 hours.

Updated Custom Signal Builder

My goal, as stated on the BA homepage, is to bridge the quantitative trading world with those who cannot (or do not want to) code. This means adding more flexibility and functionality to Build Alpha.

The latest version has an improved Custom Indicator Builder so you can build your own signals and add them to the existing 5,000+ BA signal library.

All custom signals are also parametric so you can optimize them through the Build Alpha interface. This goes for signals created using the no code editor (above) or custom signals added via python.

Machine Generated Rules

You can enable or disable this feature in the Additional Settings menu. If enabled, Build Alpha will use your selected signals to create new signals. Typically, Build Alpha will look at things like counting, sequence, correlation, weights, decay and various other transformations to create new signals from your existing selected signals. Disable this feature and Build Alpha will only use signals you have selected.

A Signal Pool or Trading Signal Pool is an aggregation of other signals to determine how many signals occur on the same bar. Looking at the combination of trading signals or pooling signals together can often present more insights and breadth of the current market.

Consider three signals like

Close is above SMA200

2-Peroid RSI is below 10

Bearish Engulfing candle

On any given bar we could have 0% true, 33% true, 67% true or 100% true. Below is a plot for 10 different RSI signals on the SP500 Emini Futures.

You can create Signal Pools with the Custom Indicator Editor. Read more about creating custom Trading Signal Pools and how they can improve simple or weak trading signals and technical indicators.

This is also how to create OR entry rules. That is, the Signal Pool is > 0 means at least one of the pooled entries is true.

OR Exit Logic

Combine exit signals with OR logic. Nothing major just an additional Exit Signal Mode for more flexibility.

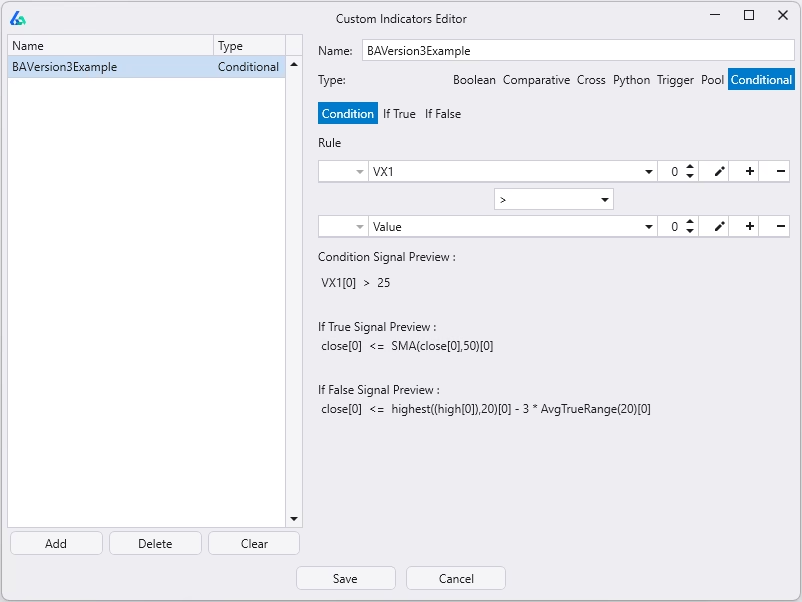

Conditional Signals

Trading rules don’t have to be rigid. For example, a volatility-based exit could tighten when markets get choppy or loosen as a trend strengthens. With Build Alpha, you can create conditional signals: if condition is true, use exit1; if false, use exit2. These conditions can also be combined and nested for more nuance than a simple on/off rule.

Example:

If VIX > 25, exit if price falls below a moving average.

If VIX < 25, exit if price drops 3 ATR below the highest close of the past N bars.

In low volatility (VIX < 25), dipping below a moving average might not matter, but when volatility spikes (VIX > 25) and price breaks below, it could signal trend reversal — so exiting makes sense.

This flexibility lets you adapt exits to different market regimes, test assumptions, and even redefine concepts like “overbought” based on context — all within Build Alpha.

Parametric Python Signals

First, I must reiterate, Build Alpha does not require you to write any python code. Build Alpha is completely no code! However, if you want to extend Build Alpha with your own custom signals you can use the no code editor or you can add custom python signals.

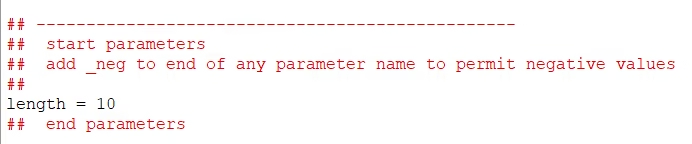

Now you can add python signals that can be parameterized and optimized by Build Alpha! Simply place your variables inside one comment section of the python template and then control the parameter ranges from Build Alpha’s user interface.

You guys asked and I could no longer deny it. For those of you burning the midnight oil, there is finally dark mode available for Build Alpha. You can control color option from the main menu View >> Themes >> Light or Dark. Here’s a quick snapshot of Build Alpha in dark mode.

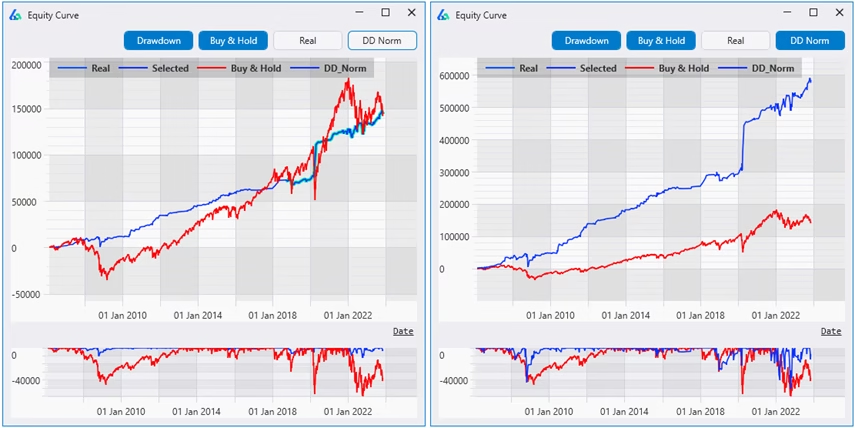

Drawdown Normalization

The latest version has a new feature in the Individual Equity Curve graph called “DD Norm” short for Drawdown Normalization. This feature aims to show how a strategy would perform (hypothetically) if one were to scale the sizing of the strategy so that the strategy’s drawdown would match the drawdown of Buy and Hold. In other words, how the strategy would do assuming the same “risk” as Buy and Hold.

Fixed Fractional Position Sizing

Size your trades based on distance to stop loss or risk level. This was popularized by (the late) Dr. Van Tharp. This is a new position sizing method added to the existing list of fixed dollar sizing, volatility based sizing, etc.

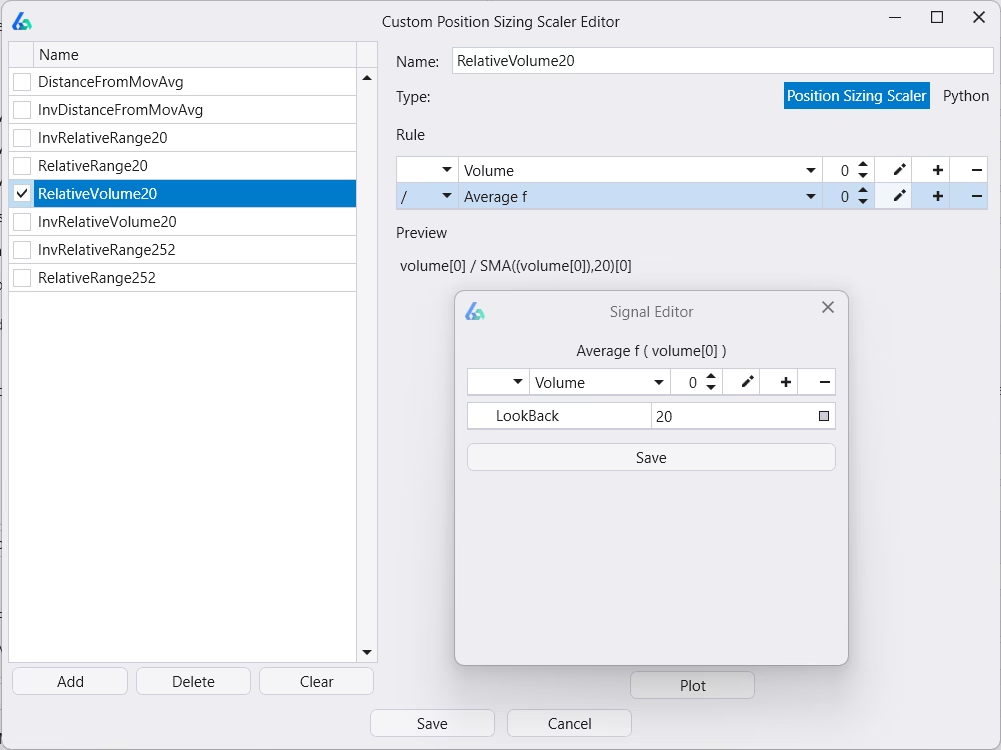

Position Sizing Scaler / Continuous Signals

Create continuous signals to multiply your position size. Some refer to this as “signal strength” but I feel that is too limiting in its application. Anyways, this feature enables total flexibility to create position sizes that scale with any market condition or calculation.

For instance, perhaps trading more [size] when volatility or volume spikes is helpful (and perhaps it is the other way); however, not testing how to size during different market conditions is the only real mistake. Build Alpha now has a no-code editor (and python ability) to create these custom or continuous sizing rules pictured below.

Plot any position sizing scaler to review it before adding to a simulation.

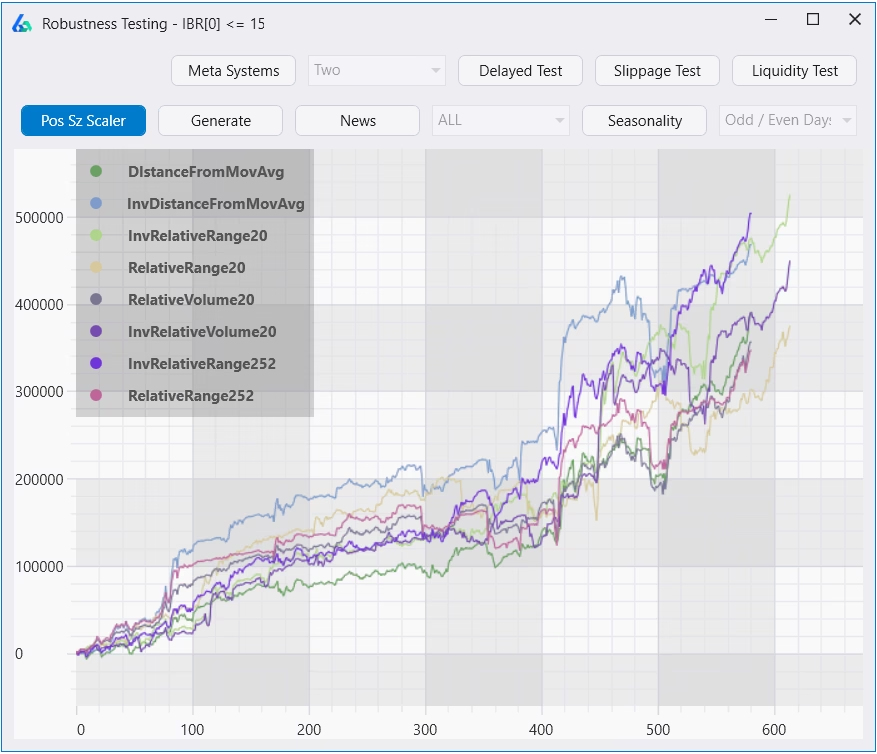

Notice the subplot shows position size grows as price declines from normal. You can also create the inverse, normalize, standardize, use percentiles, etc. to create flexible position sizing rules.

Additionally, you can create rules and allow Build Alpha to show you how any strategy would perform with any position sizing scaler. If position sizing scaler is enabled, the scaler logic will be added to the generated code for any and all platforms automatically. Below shows how different position sizing scalers can affect total P&L by 50%+ in some cases. Always worth exploring.

Commitment of Traders Report Data Added

Crowded trades and understanding positioning are playing a larger and larger role in today’s market. The Commitment of Traders Report is published by the CFTC and contains information how hedge funds, commercial hedgers and retail traders are positioning. This can help you understand if you are positioning with smart money or the dumb money.

This data can provide context about market environment for price and volume-based strategies. Build Alpha now has COT Report data included. You can read more about it here and see an example strategy using a COT filter: Improving Strategies with the Commitment of Traders Report

Weather Data Added

Build Alpha now has weather data going back 30 years to test and build trading strategies. Weather data has been successful in helping large tier 1 trading firms generate alpha over the past few years and is now available.

For instance, Citadel – the world’s most successful hedge fund – generates more from commodities than any other strategy – $30b+ since 2002. However, half of that gain has come in the last four years under Sebastian Barrack. Barrack grew a tiny strategy to one that generates 50%+ of their profit some years by using weather models (and physical tracking).

I have expanded the data in the existing Market Breadth Signal category. There is now AAII, NAAIM sentiment data. You can read about all the market breadth, sentiment and other alternative data Build Alpha has included here: Improving Strategies with Market Breadth

Google Trends Data Added

Build Alpha now has Google Trends data so traders can add sentiment and search history volume to simulations. Build Alpha has Google Trends data for the following keywords for the last 20 years (note Google already normalizes this data)

Recession

Bear Market

Market Crash

Market Bottom

Buy Gold

Financial Crisis

Bank Failures

Open a trading account

Best stocks to buy

Day trading

Options trading

Unemployment benefits

Mortgage rates

Inflation

Interest Rates

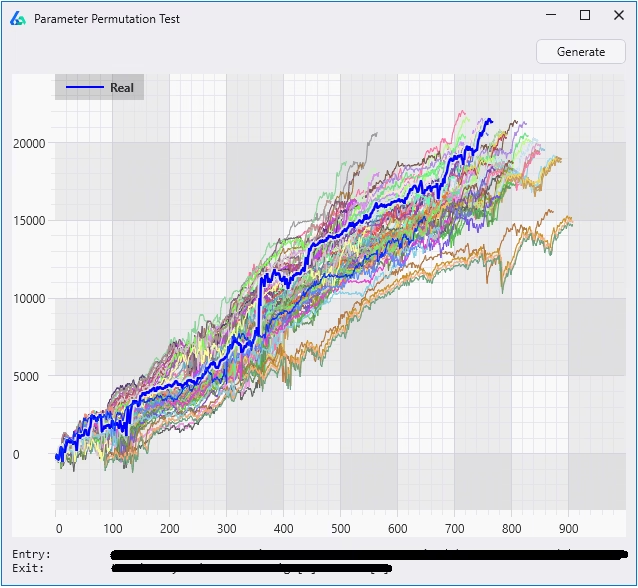

Parameter Permutation Test

Build Alpha always let you test and optimize parameters; however, I have recently added a simple Parameter Permutation Test to the right-hand panel for a quick view. Hit this button and quickly view how a strategy performs with +/- X% variation to all parameters used in the strategy with default being 10% fluctuation.

Varying the parameters also helps better set expectations. Your strategy may return 5x but after optimizing the strategy it is better to expect 2-3x (arbitrary example).

Also, a wider dispersion of results is often a sign of overfitting and of course seeing large performance degradation is a more overt sign of overfitting. Here’s an example of desirable results that are closely knit:

Stress Testing or Scenario Testing on Synthetic Data

Stress-test your strategy against the market you fear—before it happens. Build Alpha generates synthetic price series that match the statistical “fingerprint” of any asset or regime you select, then automatically tests your strategy across them. Build Alpha supports two data generation engines and a no-code rule builder to make setup fast. Chain rules with OR and BA evaluates each rule independently—color-coding results—so you can see, at a glance, how your system holds up to multiple hypothetical stressors on a single chart.

Build Alpha will also generate summary statistics – displayed under the chart – showing how each rule performed. These insights can reveal which scenarios cause trouble or spark new ideas for hedging strategies.

Walk Forward Testing (with and without Synthetic Data)

Walk Forward Testing splits the historical data into multiple training and testing partitions where we optimize strategy parameters during the training data (in-sample data, blue below) and test the best parameter settings on the unseen (out-of-sample, green below) data.

The Walk Forward test button has been added to the right-hand panel of the Strategy Generation results window. You can run various out of sample splits, runs, and create your own pass/fail metrics. Additionally, you can add alternative (synthetic) data to optimize across not only the historical price data but also on synthetic, noise adjusted data. This allows us to test our strategy on alternate realities other than the single one we lived in!

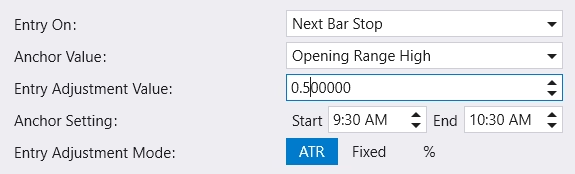

Change entry type to stop or limit orders and specify logic. Full flexibility to create custom entry logic including opening range breakouts (e.g., buy the first n-minute high of the day). Below shows how to enter at 0.50 ATR above the high of the (traditional) opening range (9:30 AM EST to 10:30 AM EST). To enter at the exact high of the opening range please make the Entry Adjustment Value 0.

You can pair this with a time signal to only trade between 10:30 AM and 4:00 PM. Additionally, you can set a maximum number of trades per day and even force an exit at the end of the day to have no overnight risk. It is extremely simple to have Build Alpha generate traditional intraday breakout strategies now.

The strategy example above uses the first two 30-minute candles of the regular trading session (9:30 – 10:30 AM, volume spikes) as the opening range and buys the breakout at the opening range high. The trade then closes at the end of the day (last big volume spike of the day, 4:00 PM) for no overnight risk.

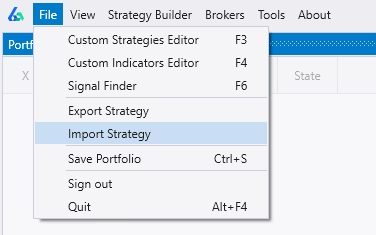

Import and Export Strategies

Build Alpha also allows you to highlight (ctrl + click) and then go to File >> Export to export strategies. These can be sent to any other Build Alpha user for easier collaboration. The receiving end can go to File >> Import and the strategies will be appended (added) to their portfolio. You can right-click to re-run or modify on your own.

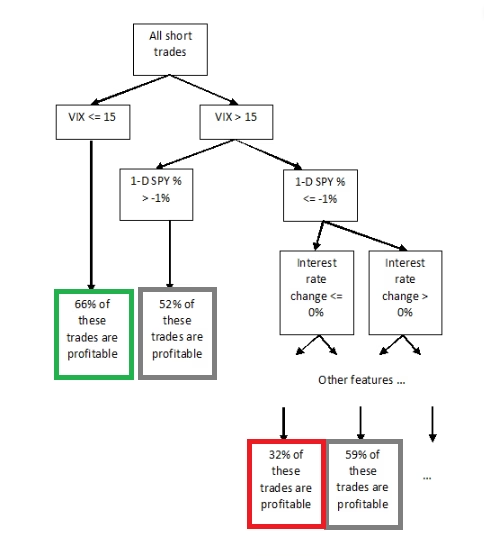

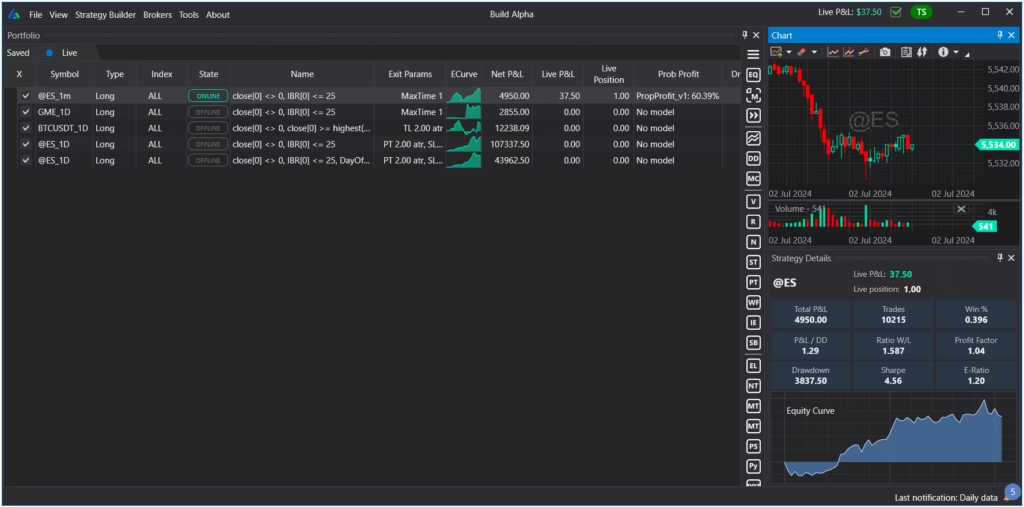

Probability of Profit Models (beta)

You can now create Probability of Profit models to overlay on your automated trading strategies. These models will predict the probability that your next trade is profitable. You can create these machine learning models with a new, no code editor and view the individual decision trees. Here is an example decision tree below.

The trader can now view a Probability of Profit model as soon as a new trade is initiated in Build Alpha’s live data view. You can see below the demonstration model shows a 60.39% chance of this current trade resulting in a profit in “Prob Profit” column.

To read more about Probability of Profit models please check this full blog post.

Social Posting (beta)

Right-click on any saved strategy to enable automatic social posting when a new trade is entered. You can publish to x.com or discord. Instructions to set it up are in the written User Guide.

You can publish any trading system

with or without entry and exit logic visible

after x number of wins or losses

add your own text or logo

You can configure all of this through this easy to use interface seen below.

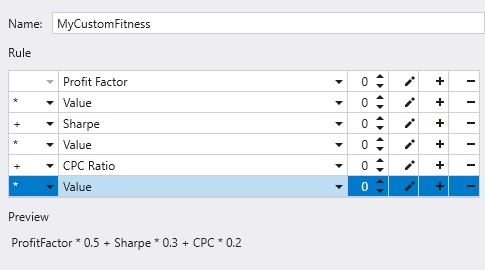

Custom Fitness and Correlation Fitness

Build Alpha now has the ability to search for strategies that meet any custom fitness function. This is the metric that the software will optimize for. Instead of optimizing for Sharpe ratio or total return now you can create a weighted fitness function that combines many metrics.

Additionally, you can now set Correlation as the fitness function and Build Alpha will search for strategies that are the least correlated to your existing portfolio. This is a huge time saver to find complimentary strategies that can improve risk-adjusted returns.

Portfolio Mode

Build Alpha now lets you combine many independent, uncorrelated strategies into one shared account, simulating realistic capital interactions (not just merged trade lists), and optimize rebalancing, sizing, and exits for the whole portfolio. Full multi-strategy portfolio simulations!

Test filters and ranks at scale, inspect correlations, run multi-strategy Walk Forward, stress test across synthetic regimes, and even tap Portfolio Suggest (AI) to discover allocations and rules that improve risk-adjusted returns finding the best combinations and weightings of all your saved strategies.

Includes fundamental data (Nasdaq) for factor models and symbol filtering, in-trade re-sizing to target volatility, and a Daily Position Update Report for pre-open workflow. A full multi-strategy testing and monitoring environment. Read more here: Build Alpha Portfolio Backtesting

Summary

If you are starting to look at algorithmic trading, beginning as an automated trader or a serious trading system developer then this new update has something for you. I always want to remind everyone that the BA license does come with instructional videos, a written user guide and support. I am literally always in front of a computer because I love this stuff; contact me through the website or email anytime. I will keep building this algorithmic trading software and appreciate all of those that continue to make suggestions, test features, be sound boards, etc. because without the BA community this just wouldn’t be possible (or fun). What should I add next?

TradingView Pine Script is a proprietary programming language developed by TradingView to allow traders to easily create custom indicators, signals, and strategies to be used with TradingView’s charts and website.

In this blog, I will cover the basics of Pine Script, a few simple examples, and how traders can leverage Build Alpha (no code software) to create their own Pine Script indicators and strategies.

Why should I use Pine Script?

Pine script is a simple to use scripting language geared towards traders with little to no programming experience. Traders must have an edge to compete in the markets and I am a staunch believer that edge must be quantified! If you cannot quantify your edge, then you simply do not have one.

Pine Script programming gives traders a simple way to code their ideas and see if an edge exists. Whether analyzing your own indicators or creating strategies for backtesting or something more advanced like Edge Ratio, traders must calculate their edge before live trading.

Pine Script is a good middle ground for a trader or analyst who wants to do some coding but does not want to learn a real programming language such as C++ or Python (or has not heard of Build Alpha), for example.

Please note these guys update Pine often so there are ever evolving changes, but it has seemed to stabilize over the past few releases.

Can Build Alpha generate Pine Scrit?

Yes. Build Alpha can generate TradingView Pine Script strategy code from its no-code strategy builder. You can paste the code directly into TradingView’s Pine Editor to visualize and trade the strategy. More below.

Pine Script Vs. Easy Language

Much like Pine Script, Easy Language is TradeStation’s proprietary programming language geared toward helping traders with no coding background put their indicators and strategies into code for proper testing.

Both programming languages come with many built-in keywords and functions for trading such as technical indicators, order management, and more making testing strategies and coding multiple indicators easier.

As of now, TradeStation’s Easy Language is more robust than Pine Script and the consensus favorite platform among Build Alpha traders. However, Pinescript programming is slowly catching up in terms of backtesting functionality and flexibility but not quite as full functioned yet (more examples later).

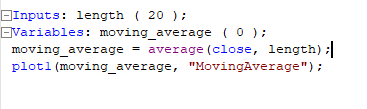

Code Comparison

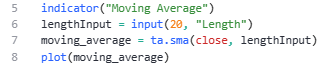

On the left-hand side we have a custom indicator for the moving average function in Easy Language and on the right-hand side there is custom pine script to plot the moving average in TradingView. This is simply to show the full code syntax of each language side-by-side.

Both written scripts are very similar with input options or “inputs” (variable values) which can be controlled through the script settings GUI and optimized while strategy backtesting. Both ignore any default value and require saving before loading onto a chart to view the moving average line.

Please spare writing comments about removing unneeded variables and placing the function call directly in the plot statement, etc. I wanted to show the cleanest possible code for demonstration purposes.

SPY TradingView Example

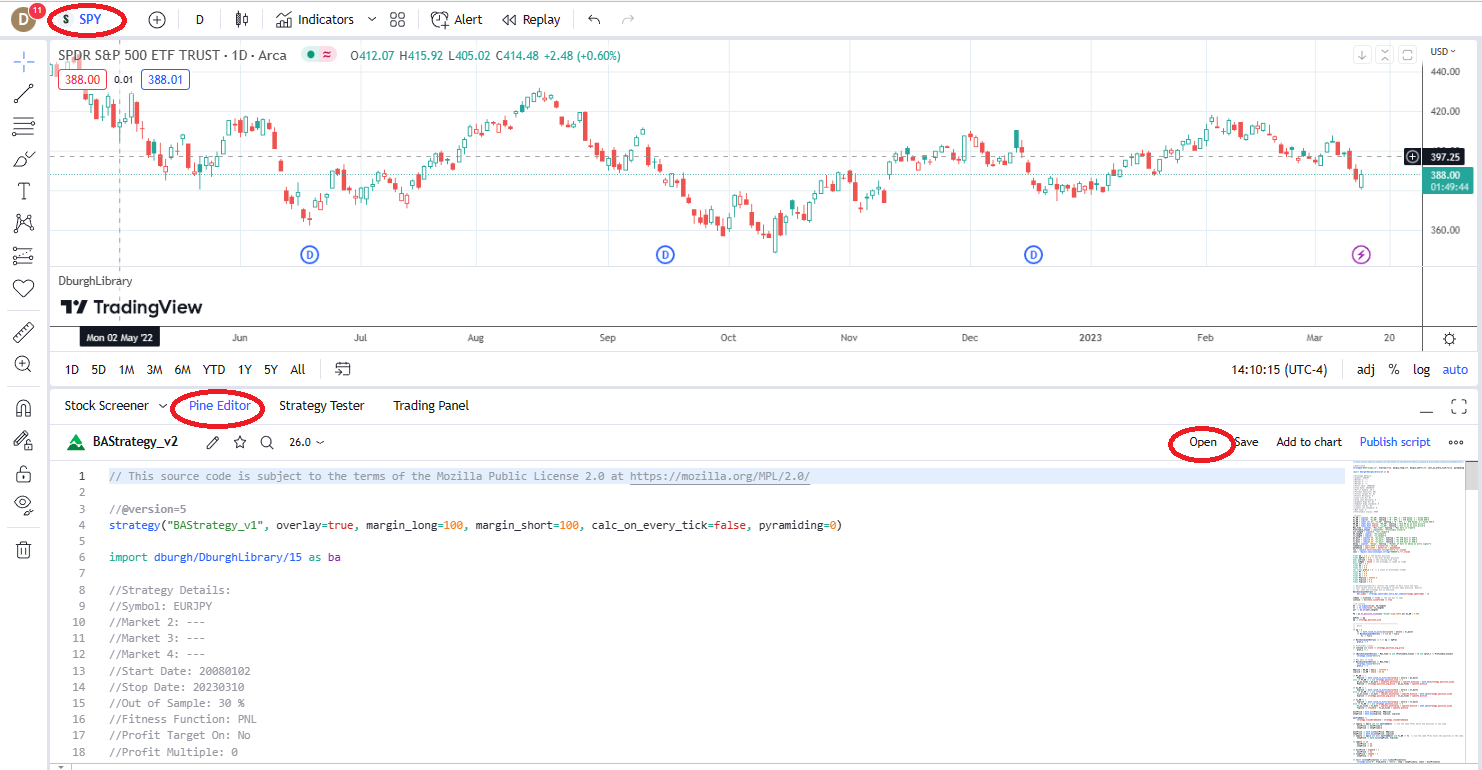

A quick primer on TradingView will serve all traders at this point. First, let’s open a page or chart of SPY – the most popular ETF in all markets – and take a look at what we see. Change the symbol in the upper left corner.

Next, open the Pine Script editor to create a new indicator or strategy. Select the Pine Editor and then hit Open. This is where creating custom indicators and all the code lives.

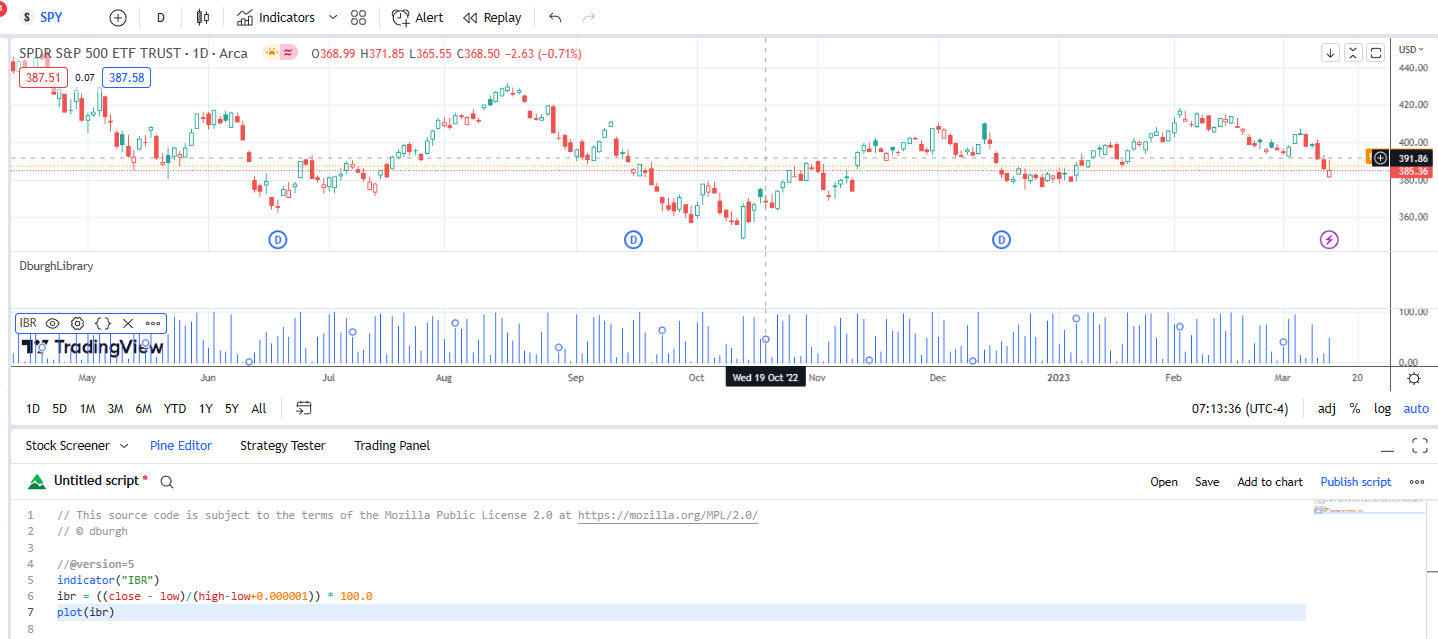

Above (and below) is simple Pine Script code for a custom indicator that plots the Internal Bar Rank or the Internal Bar Strength. This is the IBR signal in Build Alpha’s built-in library. It simply plots the close in relation to the bar’s high-low range.

An IBR reading of 25% means the close was in the bottom 25 percent of the bar’s range (weak close). A reading of 90% would mean the close was near the high of the day (strong close).

TradingView Backtesting (quick note)

TradingView is much more than a charting platform as a free tradingview account gets you access to new features like technical analysis, price data, open-source scripts, the pine script language, built-in tradingview indicators, and the ability to backtest trading strategies.

It is important to note that TradingView’s backtesting is in its infancy and does not support all functionality that other platforms dedicated to backtesting (like Build Alpha, TradeStation, etc.) do.

This blog’s intentions are not to highlight the pitfalls or shortcomings of TradingView but to present it as an alternative for quantitative traders (often with a smaller budget or looking to trade across borders).

Build Alpha – Strategy Building with No Code

Build Alpha is no code algorithmic trading software designed to empower quant traders with fast prototyping and strategy testing for any market, timeframe or bar type. Build Alpha can backtest strategies and has its own signal generators (genetic algorithm) that builds the best strategies for you given your inputs. It was designed to be a huge time saver for those with big research to do lists (myself primarily).

After Build Alpha generates the best performing strategies based on your inputs, the trader can click to highlight any strategy and then press one button to generate fully automate-able code for a ton of platforms.

I am happy to announce that Trading View’s Pine Script is newly added to the latest Build Alpha release. Below I will cover a full example from setting up Build Alpha, generating the Pine Script code, and ultimately putting the generated code into Trading View to view the performance/compared to Build Alpha.

Create Custom Indicators with no programming language

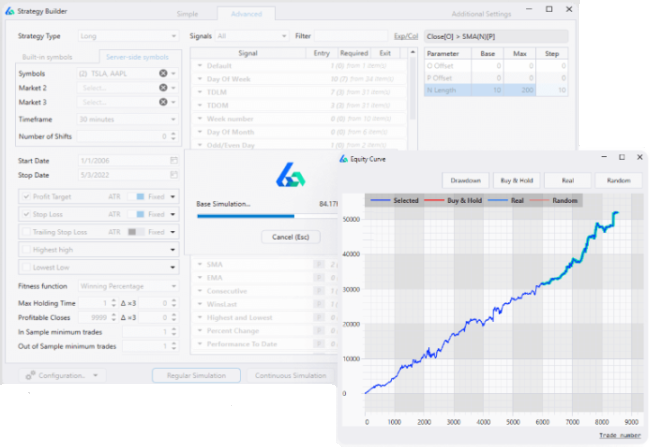

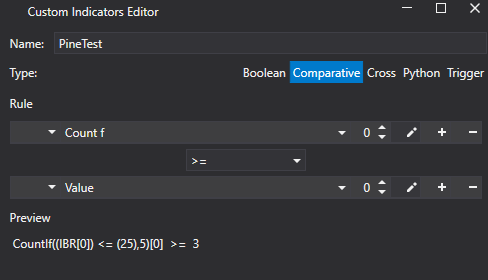

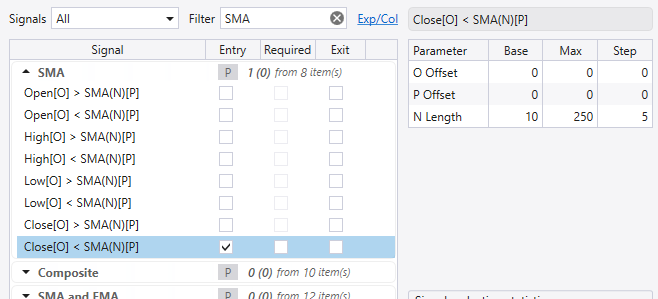

To highlight another new feature in the latest Build Alpha release, we will create a custom indicator using the new no-code editor in BA (dark mode). Let’s create a signal that only trades if 3 or more of the last 5 bars have closed in the bottom 25% of their respective range (yes, the IBR indicator)!

Below is how it looks in the Custom Indicator Editor in Build Alpha. Click the pencil to edit the condition inside the ‘Count F’ function.

Generate Algo Trading Strategy with no code

Next, let’s use the custom signal above to generate a trading strategy in BA. I wrote more about automating trading strategies with no code in this link for those interested: Automate with No Code

First, type in PineTest to the signal search bar and select it for Entry. I am going to require it as well (this forces the software to use it in every strategy it generates).

Next, let’s add the IBR signal by typing that into the signal bar and selecting it for Entry. I will not edit the ‘V’ value and will use the default signal that IBR is less than or equal to 25% (settings not pictured).

Finally, let’s add a filter that the current price must be above its Simple Moving Average. Type SMA into the search filter and select Close less than SMA as an Entry signal. Additionally, let’s let Build Alpha find the best moving average length to use and give it a range from 10 to 250 stepping by 5.

Please note there are other SMA signal categories for crossovers, moving average slopes, etc.

I have set max entry rules to three, so we always have our two required rules plus one of the SMA variations in every strategy the software builds. The only exit is a one day hold (no stop loss for this test) and will run on SPY for demonstration purposes.

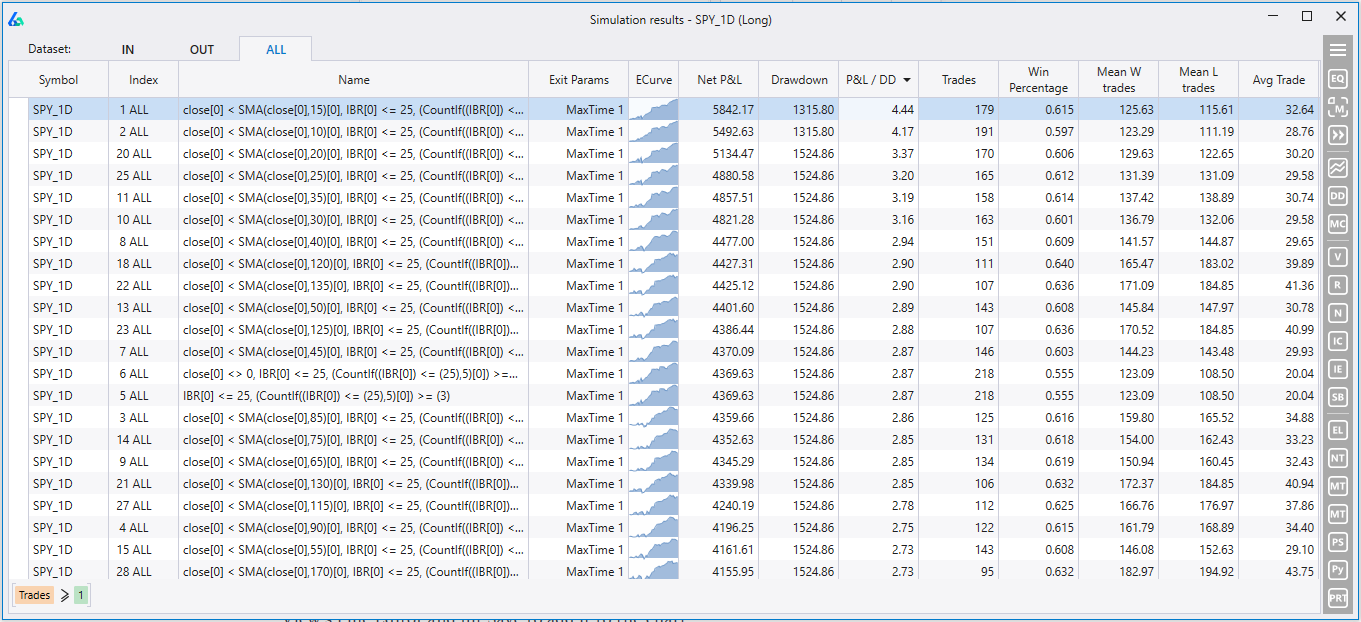

Generate TradingView Pine Script

After we hit Simulate, we can view all the variations to find the best performing SMA filter plus our two rules (IBR and IBR count).

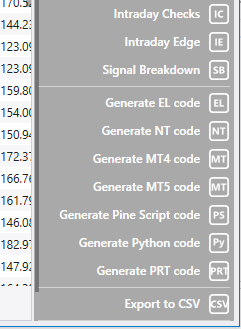

Click a strategy to highlight then click the Generate Pine Script Code button in the lower right. I’ve expanded them for the below picture, but they are collapsed (but still clickable) in the above photo.

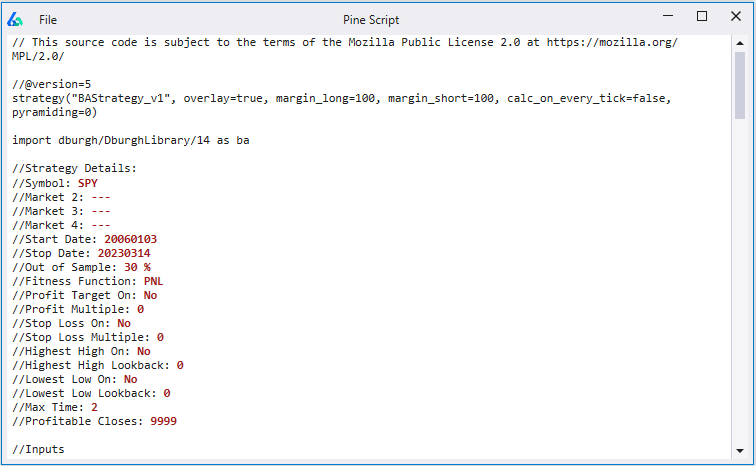

Build Alpha will pop open a new window with full code that can be copy and pasted into Trading View’s Pine Editor including code for the custom indicator. Save and then place on a SPY chart to view.

Below you can see the strategy’s equity curve on TradingView, Build Alpha, and TradeStation. TradingView is still in its infancy in regards to data quality, backtesting ability, and accuracy but I felt it was a close enough match that it was time to support TradingView.

The more recent underlying data seems more accurate in TradingView. Here is a small sample of the last four trades to show an exact match in trade size, entry, exit, P&L!

TradingView Paper Trading

TradingView does support paper trading for users looking to build and incubate tons of strategies before going live. Once the generated pine script code is loaded on a Trading View chart you can watch the trading strategy on live price data on screen similar to a paper trading account without doing anything.

Build Alpha’s latest upgrade also has the ability to monitor strategies live and output real-time alerts, issue position updates and update P&Ls. Simply right-click on a strategy to save it to your BA portfolio and then enable it for Live Simulation.

Takeaways

Pine Script is TradingView’s proprietary programming language

Pine Script has many built-in trading related keywords and functions

Pine Script and Easy Language are very similar for those familiar with TradeStation

Build Alpha generates both TradeStation Easy Language and TradingView Pine Script code at the click of a button

Pine Script and TradingView’s backtesting accuracy is still in its infancy but coming along quickly

Summary

Trading View has taken over the trading world in the past few years with its easy to use web based charting platform. The introduction of their proprietary programming language, Pine Script, is proving to be a great resource for those traders understanding the need to quantify their ideas and looking for automation. Build Alpha now generates complete code for Pine Script for those that do not want to learn to program but still want to quantify their ideas, build robust strategies, and take advantage of TradingView.

Video example below of Pine Script code generation and matching results with Build Alpha:

Pine Script + Build Alpha FAQ

Can TradingView auto-trade my Pine strategy?

Yes, you can autotrade with TradingView using its alert sysetm to send webhooks to a third-party automation platform or directly to a supported broker.

Will TradingView and Build Alpha results match exactly?

They can differ due to data sources, backtest assumptions, and execution modeling. However, if you use the same data and align settings results will match (as shown above).

Can Build Alpha generate indicators too?

Yes, the generated code can be modified to work as an indicator, if desired.

What You’ll Learn

How to generate NinjaTrader strategy code with Build Alpha

How to import/compile in the NinjaScript Editor

How to verify backtest matching and avoid common mismatches

How to Download NinjaTrader

First, create a free NinjaTrader account at NinjaTrader.com and download the NT8 NinjaTrader8 platform. Often Ninjatrader.com needs to review the security of your connection and may request you verify you are human by completing a simple captcha.

NinjaTrader 8

Currently NinjaTrader is on version 8. Build Alpha has supported NinjaTrader since NinjaTrader7 but now proudly supports Ninjatrader8. Make sure you download the latest version for the best experience.

NinjaTrader Brokerage Account

Ninjatrader is also their own broker, meaning you can open a real money account and trade directly through the Ninjatrader platform.

NinjaTrader is arguably the best futures broker available at the moment for retail traders and serious independent traders. NinjaTrader has a wide variety of futures data connections and has competitive margin requirements. You can trade all assets through NinjaTrader but it is particularly good for futures traders.

NinjaTrader also permits full automation of trading strategies using their proprietary NinjaScript programming language. The programming language is C# based and extremely flexible.

There are tons of existing functions, tools, indicators and strategy logic blocks for those that want to dive into the C# code. For those that do not want to write their own code, there is of course Build Alpha!

NinjaTrader Automated Trading Systems with No Code

Build Alpha generates fully operational NinjaTrader code at the click of a button with perfectly matching results across the two platforms. Build Alpha enables traders to build and execute their own trading ideas with no code and then easily transfer the generated code over to NT8 for live (or simulated) trading.

Build Alpha vs NinjaTrader Strategy Builder vs Coding

NinjaTrader has their own basic Strategy Builder which may be good for basic rules but can be quite limiting. It also only tests a single idea at a time and has no artificial intelligence to help arrive at better strategies for you.

NinjaScript – NinjaTrader’s proprietary coding language – gives maximum flexibility but requires coding time. It is C# based so it is not trivial for a non-coder to pick up.

On the other hand, Build Alpha generates thousands of strategies per second improving them using a genetic algorithm and artificial intelligence (my background in machine learning). BA also has the most advanced suite of robustness tests and completely exportable NinjaScript code.

How to Automate Build Alpha strategies in NinjaTrader with no coding

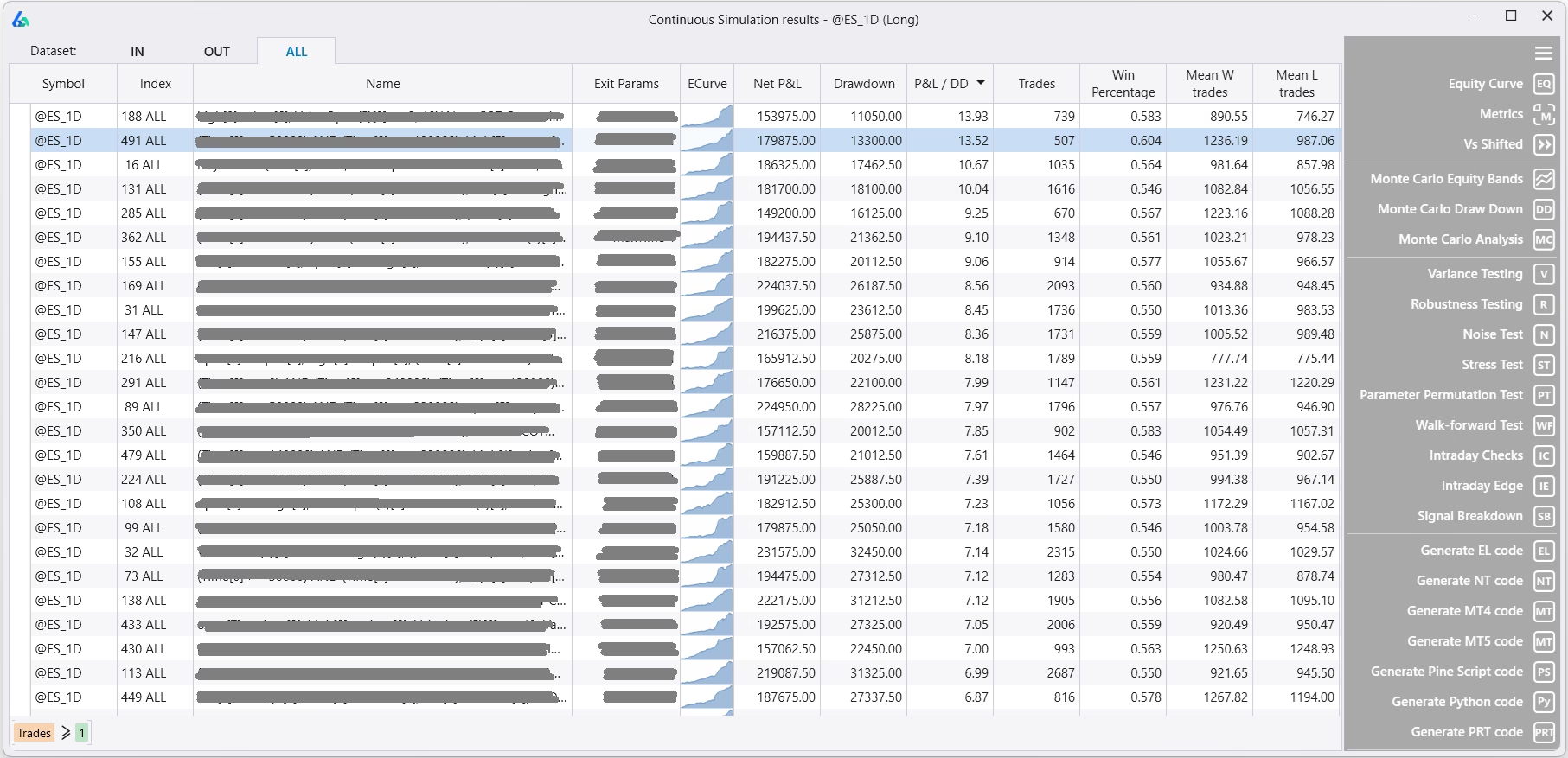

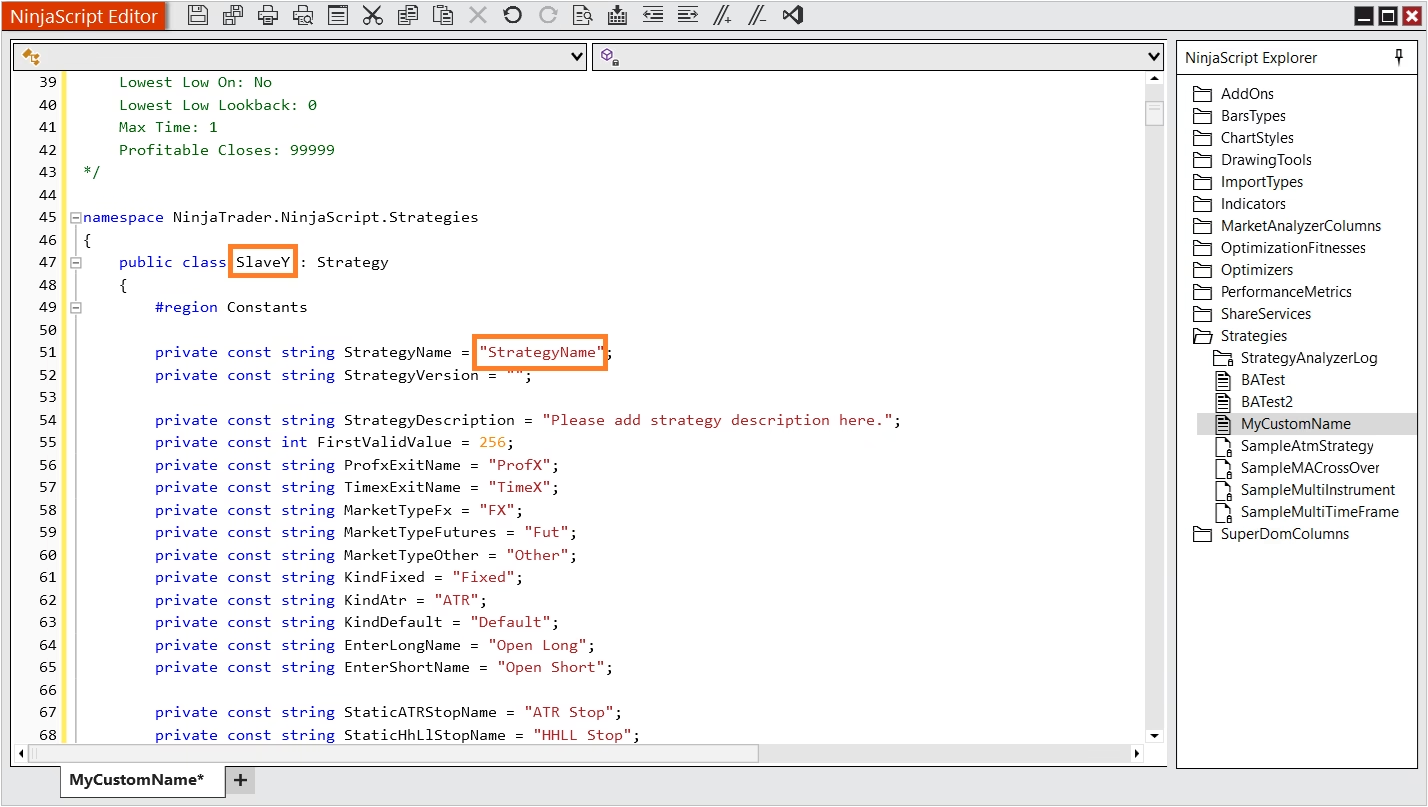

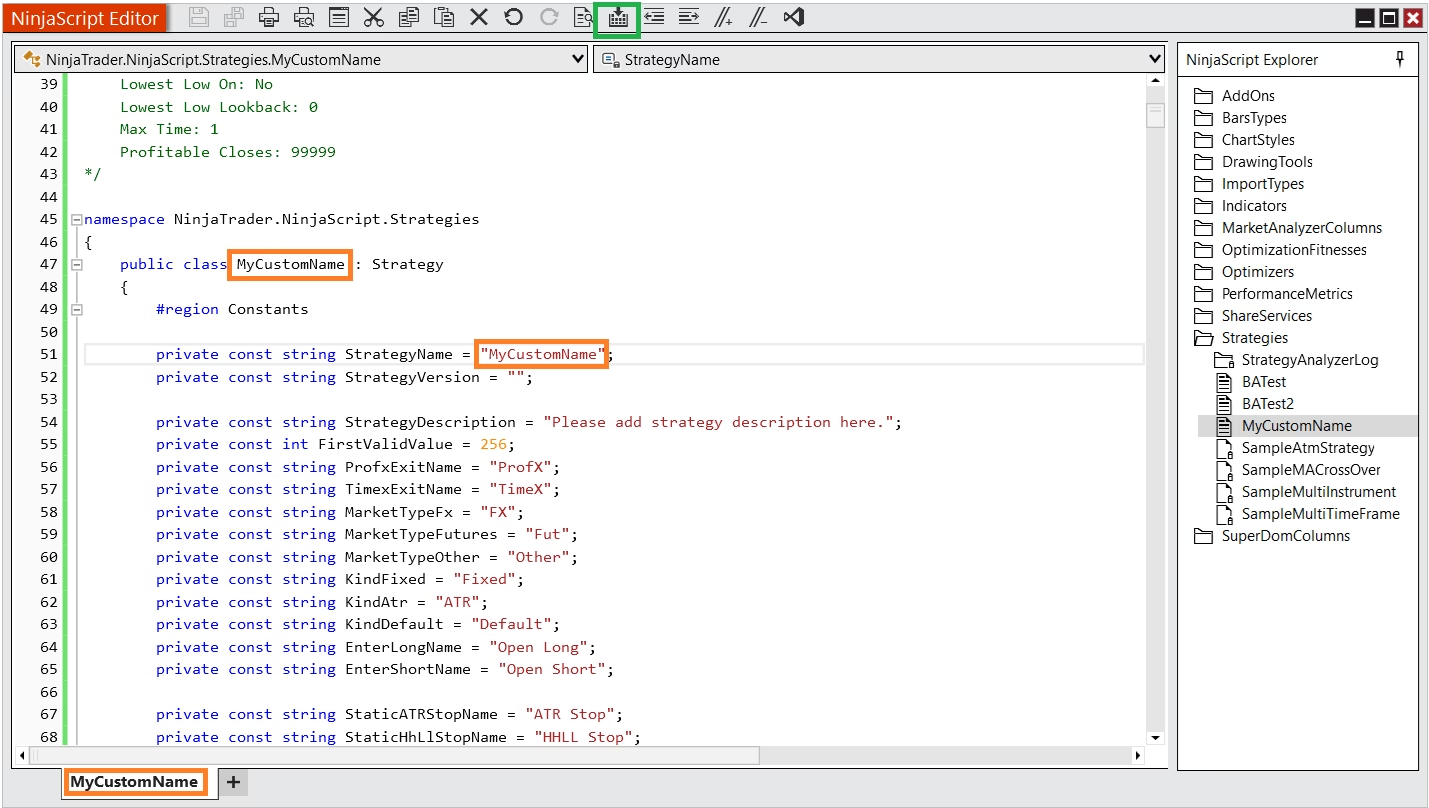

First, let’s generate a simple strategy so we can talk about the same example. I selected a few thousand signals in Build Alpha, hit simulate, and selected a random strategy to review.

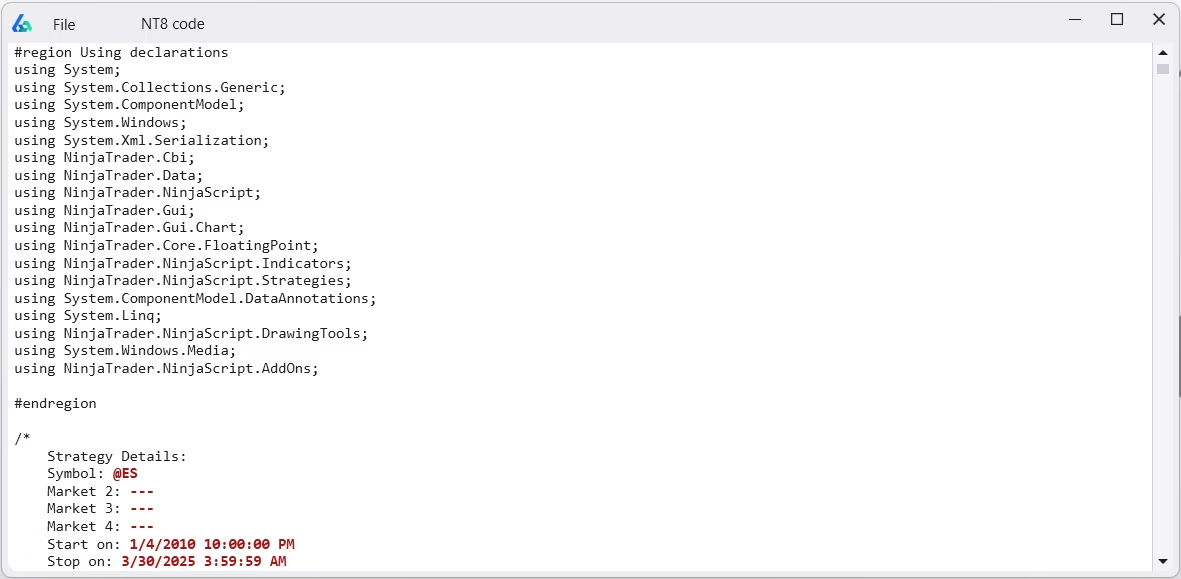

Next, hit the ‘Generate NT Code’ button in the lower right of the Strategy Simulation results window pictured above. NT stands for Ninjatrader8. Please note there are also Build Alpha code generators for

Below is a picture of the Build Alpha generated code for NinjaTrader8. Copy all the code by hitting CTRL + A (to highlight all) and CTRL + C (to copy all).

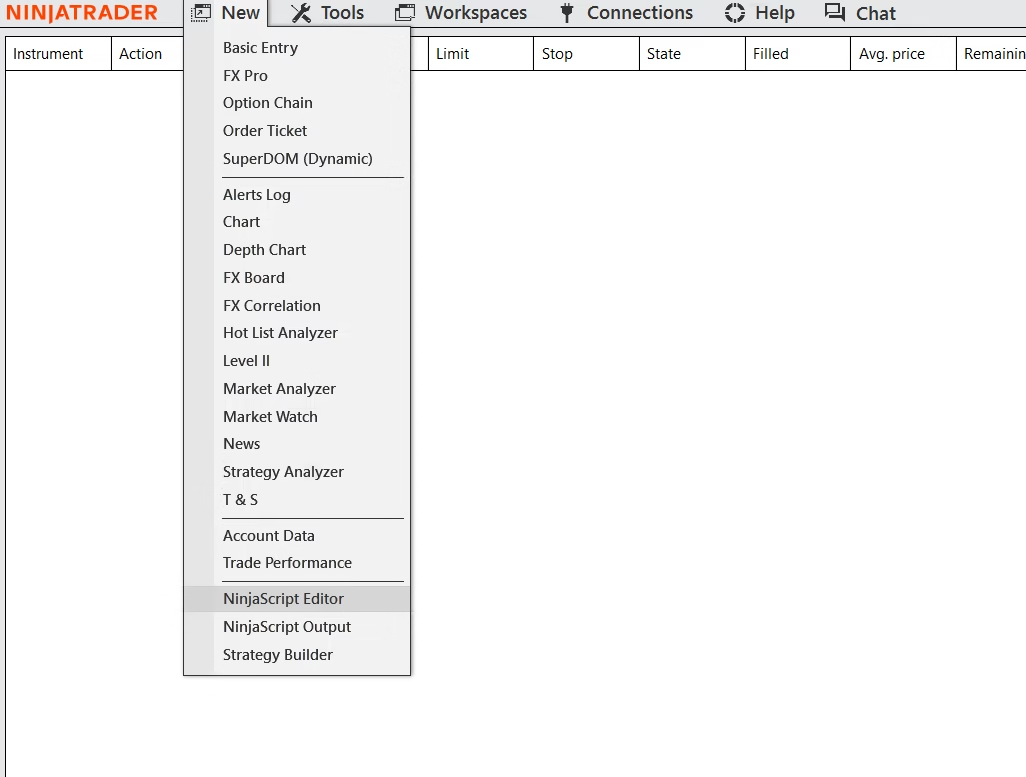

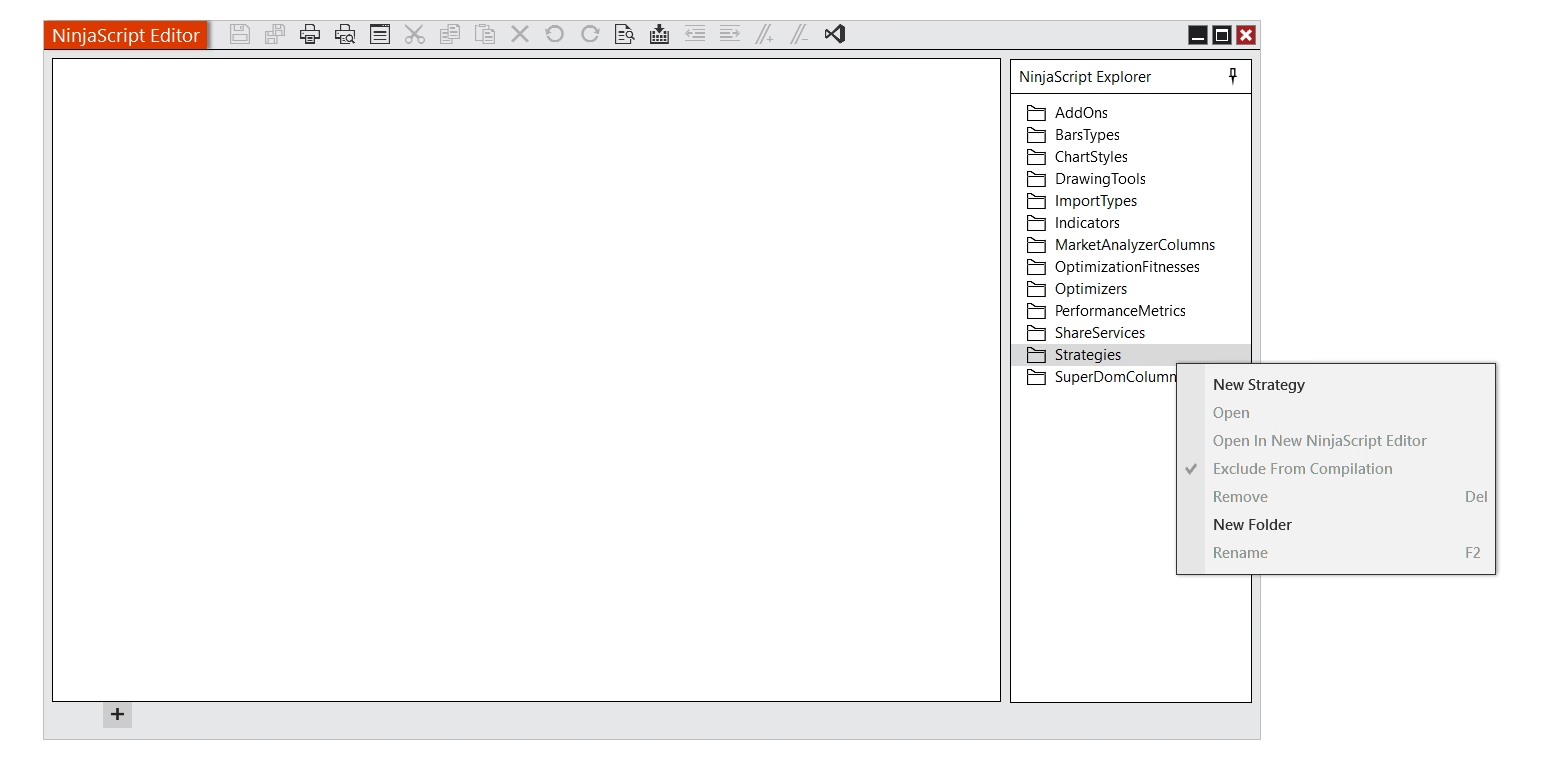

In NinjaTrader, go to New >> NinjaScript Editor