Luck in Trading and Favorable Distributions

The role of luck in (algorithmic) trading is ever present. Trading is undoubtedly a field that experiences vast amounts of randomness compared to mathematical proofs or chess, for example.

That being said, a smart trader must be conscious of the possibility of outcomes and not just a single outcome. I spoke about this in my Chatwithtraders.com/103 interview, but I want to reiterate the point as I am often asked about it to this day.

The point I want to make is that it is very important to understand the distribution your trading strategy comes from and not just make decisions off the single backtest’s results. Doing so can increase a trader’s “luck”.

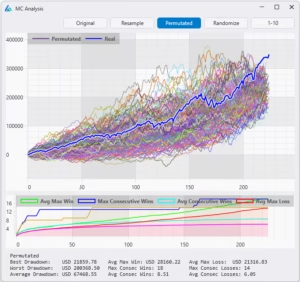

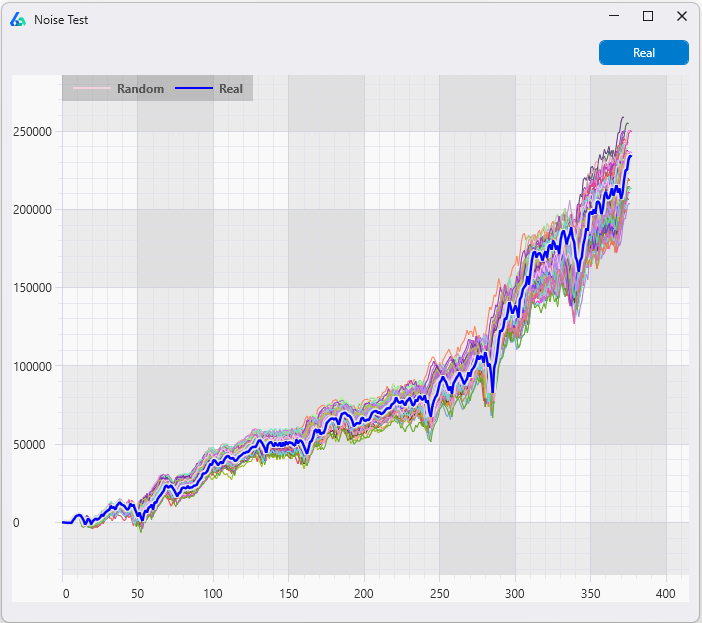

In the interview I spoke about this graph below that shows two different trading systems that have very similar backtests. The black line on the left represents system A’s backtest and the black line on the right represents system B’s backtest. For our intents and purposes let’s assume the two individual backtest results are “similar” enough producing the same P&L over the same number of trades.

The colorful lines on the left is system A simulated out (can use a variety of methods such as Monte Carlo, Bootstrapping, etc.) and the colorful lines on the right is system B simulated out using the same method. These are the possible outcomes or paths that system A and system B can take when applied to new data (Theoretically – read disclaimers about trading).

These graphs are the “distributions of outcomes” so many successful traders speak about. This picture makes it quite obvious which system you would want to trade even though system A and system B have very comparable backtests (black lines).

*There are many ways to create these “test” distributions but I will not get into specifics as BuildAlpha does quite a few of them*

Another View

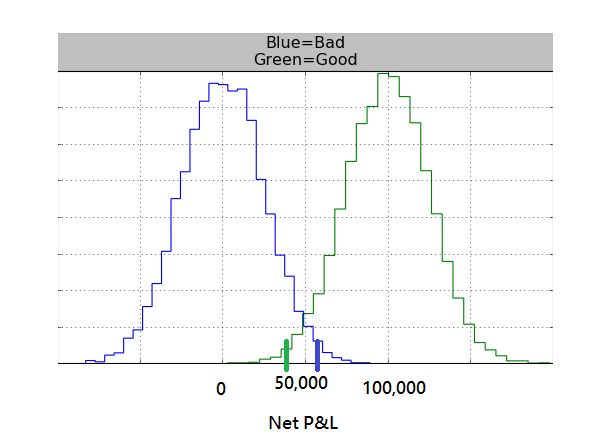

This second example below demonstrates this point in another way but incorporates the role luck can have on your trading. Let’s say the blue line is the single backtest from System A (blue distribution is all possibilities). The single green line is the single backtest from System B (green possibilities).

In this graph, you can see that System A (part of the blue possibilities) was lucky and performed way better than most of the possibilities and of course better than the single backtest for System B.

You can also see that System B (part of the green possibilities) was extremely unlucky and performed way worse than most of the green possibilities.

Moving forward… do you want to count on Mother Market to give system A the same extremely favorable luck? or do you want to bet on system B’s luck evening out?

I always assume I will be close to the average/median of the distribution moving forward which would put us at the peaks of both of these possibilities or distributions… if that is the assumption then the choice is clear.

Update Announcement

Build Alpha licenses now come with an instructional video series or course that goes over all the features and how to use the statistical tests the software offers. It makes spotting systems and their related distributions much easier than Build Alpha already makes it.

Thanks for reading,

Dave